In a significant strategic move within the maritime industry, KOREA LINE CORPORATION (KLC) has officially secured a major long-term charter contract with its partner, H-Line Shipping Co., Ltd. This agreement, valued at a substantial 66.5 billion won, is far more than a simple revenue entry; it represents a foundational pillar for KLC’s future stability and growth. For investors and market analysts, understanding the nuances of this KOREA LINE CORPORATION contract is crucial for assessing the company’s trajectory in a notoriously cyclical industry. This analysis will dissect the deal’s structure, strategic implications, financial impact, and potential risks.

This long-term commitment provides a predictable revenue stream, insulating a portion of KLC’s business from the extreme volatility of the spot market and strengthening its competitive position for the years to come.

Breaking Down the ₩66.5 Billion KLC H-Line Shipping Deal

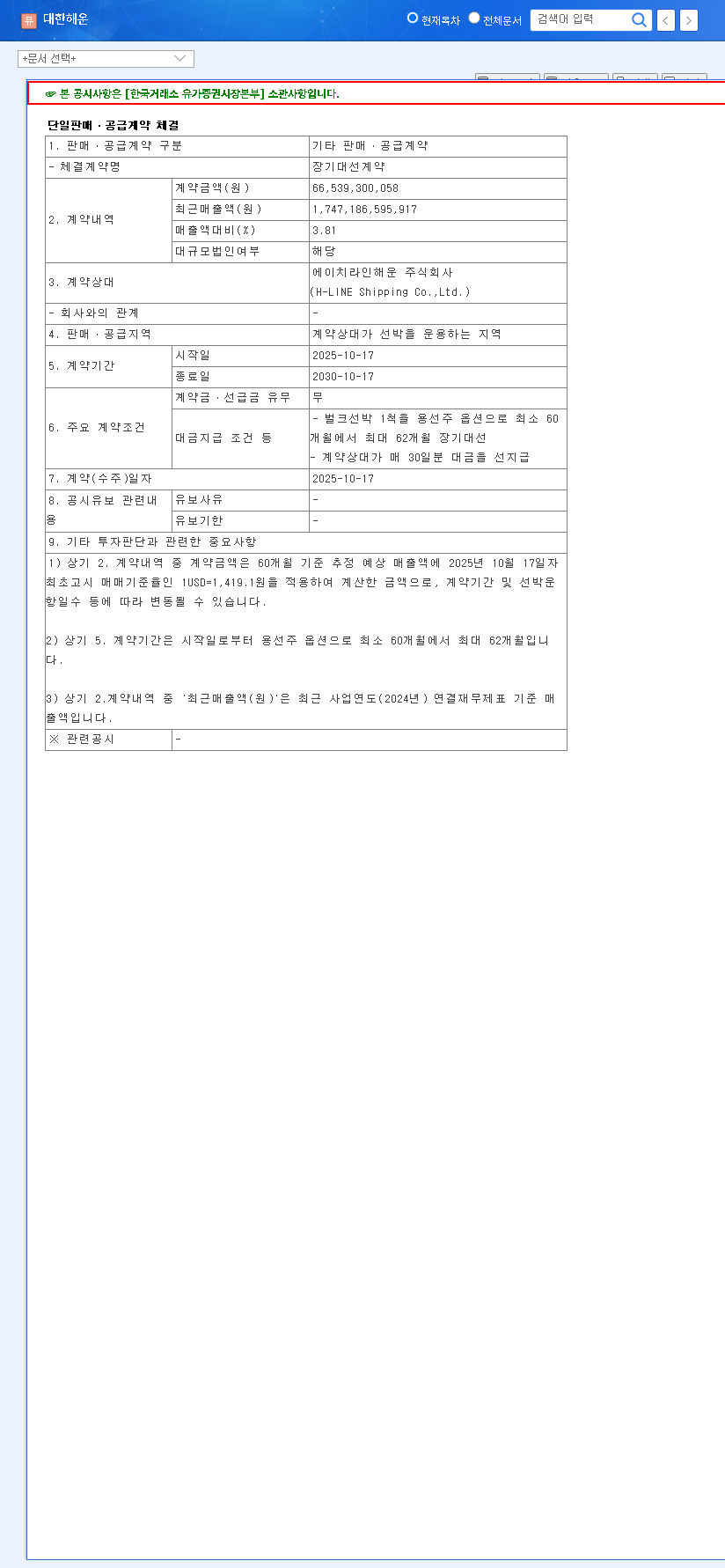

On October 20, 2025, KOREA LINE CORPORATION announced the execution of a single sales/supply contract, specifically a long-term charter, with H-Line Shipping Co., Ltd. This type of agreement involves leasing vessels for an extended period at a pre-agreed rate, offering stability to both the vessel owner (KLC) and the charterer (H-Line). Here are the core details of the agreement:

- •Contracting Parties: KOREA LINE CORPORATION (as the provider) and H-Line Shipping Co., Ltd. (as the client).

- •Contract Value: 66.5 billion Korean Won (KRW).

- •Contract Duration: A five-year term, commencing on October 17, 2025, and concluding on October 17, 2030.

- •Revenue Significance: The total contract value represents approximately 3.81% of KLC’s most recent annual revenue, providing a notable and steady income contribution.

Long-term charter contracts are the bedrock of stability in the shipping sector. They allow companies like KLC to de-risk their operations, secure financing for fleet expansion, and build resilient, lasting relationships with key clients.

Strategic Importance & Financial Impact

The strategic value of this KOREA LINE CORPORATION contract extends far beyond its face value. It’s a calculated move to fortify the company’s market standing and financial health.

Enhanced Business Stability and Predictability

The primary benefit is a significant boost in revenue predictability. The shipping industry is often subject to wild swings in spot market rates, which can make financial forecasting difficult. By locking in a five-year revenue stream, KLC can better plan for capital expenditures, operational costs, and future investments. This stability is highly valued by investors and lenders, potentially leading to a lower cost of capital.

Strengthened Customer Relationships and Market Position

Finalizing a multi-year deal with a major industry player like H-Line Shipping solidifies a critical business partnership. It demonstrates KLC’s reliability as an operator and enhances its reputation in the competitive Asian shipping market. This can serve as a powerful case study when bidding for other long-term contracts, creating a virtuous cycle of growth and solidifying its position within the global maritime industry.

Positive Financial Cascade: Revenue, Cash Flow, and Profitability

From a financial perspective, the contract is expected to have several positive effects. The consistent inflow of charter fees will improve cash flow management, providing liquidity for operations and debt servicing. While the exact profit margin is not public, long-term contracts are structured to ensure profitability by covering operating costs, depreciation, and a healthy margin. This predictable profit contribution will support KLC’s bottom line over the contract’s term.

Navigating Risks and Investor Considerations

While the outlook is positive, a comprehensive shipping investment analysis requires a clear-eyed view of potential risks. Investors should remain aware of several factors that could influence the outcome of this contract and KLC’s overall performance.

- •Counterparty Risk: The agreement’s success hinges on the financial health of H-Line Shipping. Any unforeseen financial distress on their part could disrupt contract fulfillment.

- •Operational Risks: Unforeseen vessel maintenance, downtime, or accidents could impact the efficiency and profitability of the chartered vessels.

- •Macroeconomic Headwinds: Global economic slowdowns, trade disputes, or sharp fluctuations in fuel prices and exchange rates can affect the broader shipping environment, even if the charter rate is fixed.

- •Opportunity Cost: If spot market rates were to surge dramatically and remain high, the fixed rate of the long-term charter might appear less profitable in hindsight. However, this is the trade-off for security.

The complete details of the agreement were filed publicly as required by financial regulations. For those seeking primary source information, the filing is available for review. Source: Official Disclosure (DART).

Conclusion: A Prudent Step Forward

The 66.5 billion won long-term charter contract with H-Line Shipping is a clear positive for KOREA LINE CORPORATION. It enhances financial stability, strengthens a key partnership, and provides a solid foundation for future growth initiatives. While investors should monitor the associated risks, the market is likely to view this as a prudent and value-accretive strategic decision. Understanding the broader trends in global shipping, such as those monitored by the International Maritime Organization, provides further context for KLC’s strategy. For more insights, you can read our full analysis of the bulk carrier market. This move positions KLC to navigate the future with greater confidence and predictability, a quality that is highly prized in the dynamic world of maritime logistics.