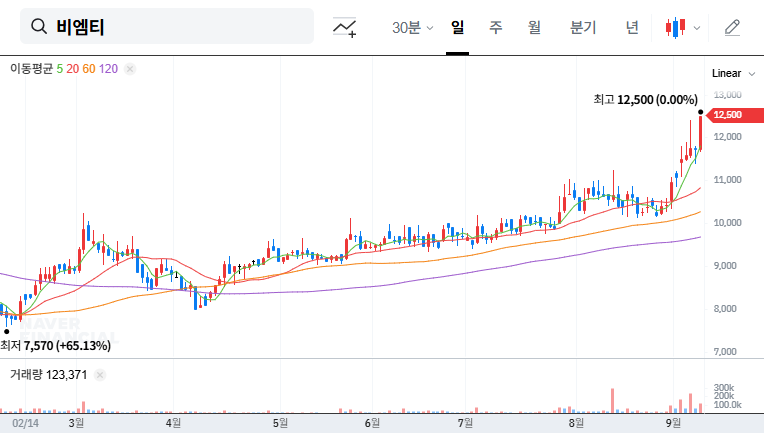

The latest BMTCo.,Ltd. earnings report for Q3 2025 has sent a strong signal to the market, revealing a performance that significantly outpaced expectations. For investors tracking BMTCo.,Ltd. stock (086670), this ‘earnings surprise’ raises critical questions: Is this the start of a sustained recovery, or a temporary bright spot? This comprehensive analysis will unpack the results, explore the underlying drivers, evaluate potential risks, and provide a clear outlook for investors.

BMTCo.,Ltd. Q3 2025 Earnings: A Stunning Performance

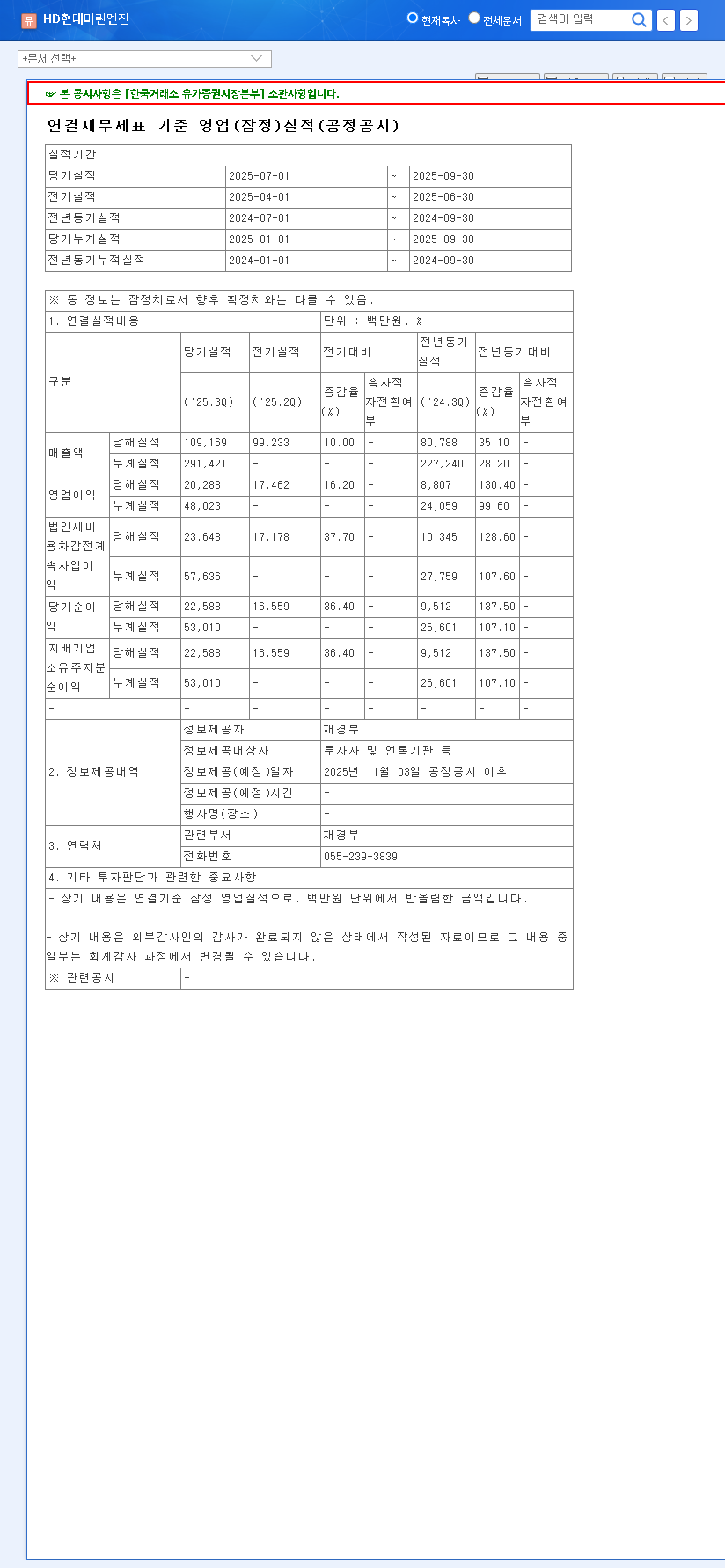

On November 10, 2025, BMTCo.,Ltd. released its preliminary Q3 2025 financial results, showcasing a dramatic turnaround and robust profitability. The numbers, detailed in the Official Disclosure (DART), paint a picture of renewed strength and operational efficiency.

By the Numbers: Key Financial Highlights

The core of the 086670 earnings analysis lies in comparing its performance against previous periods. The year-over-year (YoY) metrics are particularly impressive, demonstrating a significant recovery from 2024.

- •Revenue: 37.5 billion KRW, marking a 14.7% increase YoY, though down 4.8% quarter-over-quarter (QoQ).

- •Operating Profit: 5.8 billion KRW, a significant turnaround from a flat 0 KRW YoY and a 70.6% surge QoQ.

- •Net Profit: 12.6 billion KRW, a massive recovery from a -1.5 billion KRW loss YoY and an astounding increase of over 1,100% QoQ.

This explosive growth in profitability has effectively addressed concerns that arose from a slower H1 2025, positioning the company for a positive re-evaluation by the market.

Decoding the Success: What’s Driving BMTCo.,Ltd.’s Growth?

This impressive earnings report isn’t a random event. It’s rooted in a combination of a solid business foundation, strategic market positioning, and favorable industry trends.

A Foundation in Core Industries

BMTCo.,Ltd. derives stability from its essential role in supplying critical components to key global industries. This includes shipbuilding and offshore plants, power generation (with a focus on nuclear energy), and the high-tech semiconductor sector. This diversification provides a buffer against cyclical downturns in any single market.

Technological Edge and Global Expansion

The company’s global competitiveness is bolstered by proprietary patented technologies and a portfolio of international certifications. Crucially, being qualified for bidding with major players like Chevron opens doors to high-value projects. Furthermore, BMTCo.,Ltd. is actively expanding its footprint into new markets like oil refineries and biochemicals, while also deepening its presence in the Middle East and Europe.

The combination of a diversified industrial base and aggressive market expansion is a core component of the positive investor outlook for BMTCo.,Ltd., suggesting a strategy built for long-term resilience and growth.

Navigating the Headwinds: Potential Risks to Monitor

Despite the strong Q3 results, a prudent investor must also consider the potential challenges. Understanding these risks is essential for a complete 086670 earnings analysis.

Revenue Trends and Financial Health

The minor 4.8% QoQ decline in revenue, while small, requires monitoring to ensure it doesn’t signal a new trend. More significantly, the company’s balance sheet shows a high proportion of current liabilities, including convertible bonds, which presents a short-term financial burden. Investors should watch for improvements in the company’s debt ratio and how they manage their financial soundness. For more on this, you can learn about analyzing a company’s balance sheet.

Macroeconomic and Industry Factors

External factors play a significant role. While stable oil prices benefit the plant business, and a strong USD/KRW exchange rate can boost profitability, these can be volatile. The broader health of the shipbuilding and semiconductor industries, though showing signs of recovery, remains a key variable. For expert commentary on global industry trends, sources like Bloomberg’s market analysis provide valuable context.

Future Outlook: What’s Next for BMTCo.,Ltd. Stock?

The Q3 2025 results have likely set a new floor for investor sentiment. In the short term, this positive surprise is expected to fuel upward momentum for BMTCo.,Ltd. stock. Looking ahead, the company’s long-term value will hinge on its ability to convert its strategic initiatives into sustained, profitable growth. Investors should monitor future BMTCo.,Ltd. earnings reports for evidence of new market penetration and continued improvement in financial health. The key question is whether this quarter marks a true structural improvement or was influenced by temporary factors.

Conclusion: An Action Plan for Investors

BMTCo.,Ltd.’s Q3 2025 earnings are undeniably positive, signaling a powerful recovery. While short-term prospects look bright, long-term investors should maintain a balanced view, weighing the strong operational performance against the financial and macroeconomic risks. A comprehensive investment decision should be based on ongoing analysis of confirmed earnings, order backlogs, and the company’s progress in improving its balance sheet.

Disclaimer: This analysis is for informational purposes only and is based on preliminary data. Investment decisions carry risk and are the sole responsibility of the individual investor.