Investors in EM Korea (095190) have been watching closely as its largest shareholder, Shinwha Precision, recently increased its holdings. This pivotal move is more than a simple transaction; it’s a strategic signal that could redefine the company’s trajectory. This in-depth EM Korea stock analysis will unpack the details of this development, scrutinize the company’s current financial health, weigh the potential opportunities against the inherent risks, and outline a comprehensive investment strategy for navigating the path ahead.

Is this a vote of confidence pointing towards untapped value, or a defensive maneuver amidst financial headwinds? Let’s dive in.

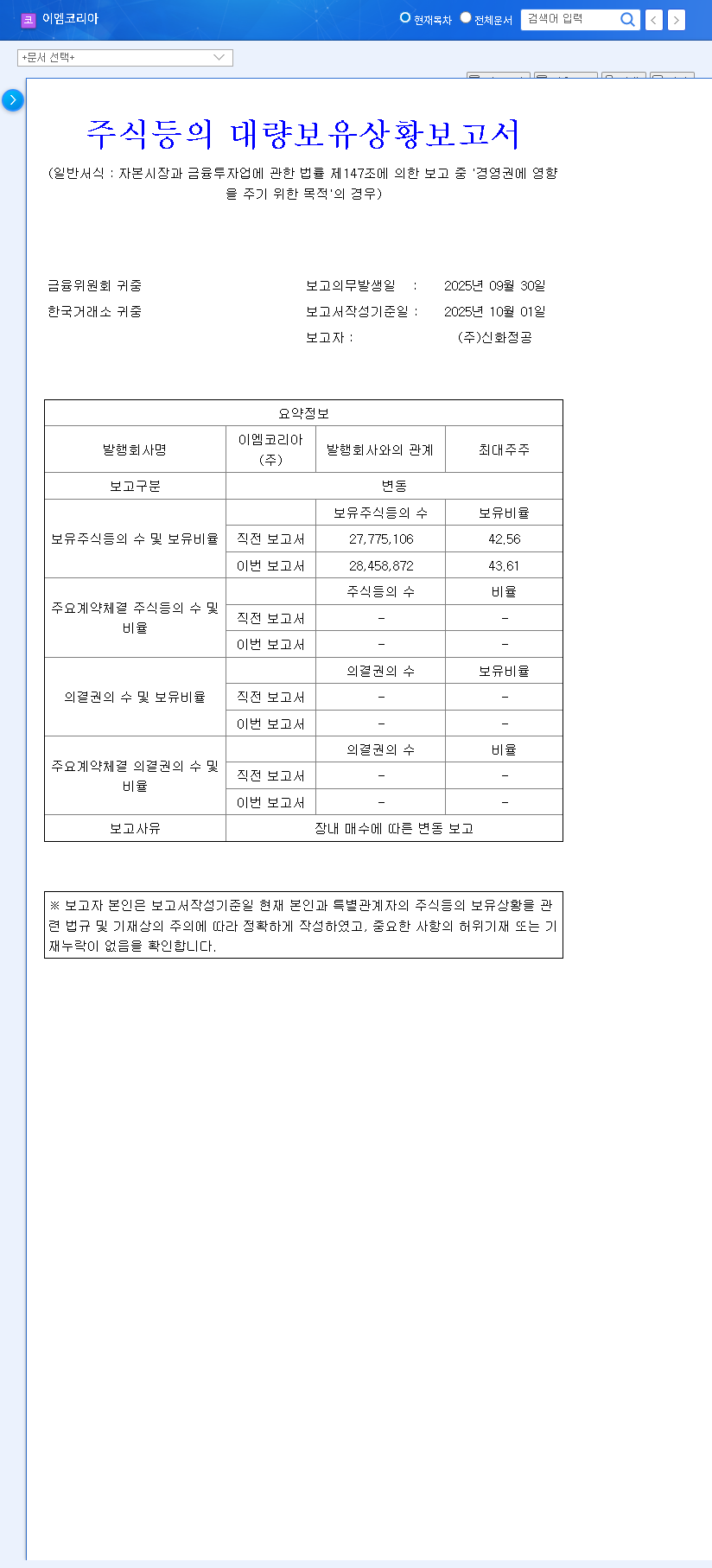

The Shareholder Shake-Up: A Closer Look

According to the latest filings, Shinwha Precision Co., Ltd. has solidified its control over EM Korea by purchasing additional shares on the open market. The specifics of this transaction are crucial for understanding the motive and potential impact.

- •Purpose of Holding: Explicitly stated as ‘influence over management control’.

- •Stake Before Increase: 42.56%

- •Stake After Increase: 43.61%

- •Transaction Details: Purchase of 653,632 shares between September 25 and September 30, 2025.

- •Source: Official Disclosure (DART)

This move to bolster management control is significant. It suggests a long-term commitment from Shinwha Precision and a desire to steer the company’s strategy with a firmer hand. However, to truly grasp the implications, we must examine the financial ground on which EM Korea currently stands.

Financial Health Under the Microscope (H1 2025 Data)

The latest financial reports for the first half of 2025 paint a challenging picture, raising questions about the company’s immediate performance despite the shareholder’s confidence. A detailed look at the EM Korea financial health reveals several red flags.

While the Defense/Aerospace sector shows promise, significant losses and declining revenue in other key areas demand careful consideration from investors.

Performance & Profitability Concerns

EM Korea’s top-line and bottom-line figures have deteriorated year-over-year. Revenue has fallen by 42.7% to KRW 69.173 billion, driven by slowdowns in the Machine Tools and Power/ITER divisions. More concerningly, the company has swung to an operating loss of KRW 1.003 billion and a net loss of KRW 3.573 billion, impacted by rising administrative and R&D costs.

A Bright Spot: Defense & Aerospace Growth Prospects

Amidst the financial challenges, the Defense/Aerospace division stands out as a core growth engine. With stable sales from supplying critical parts for major projects like the KF-X fighter, K-9 self-propelled howitzer, and T-50 advanced trainer jet, this segment provides a much-needed foundation for the company. The EM Korea growth prospects are heavily tied to the continued success and potential expansion of this high-performing division.

Investment Thesis: The Bull vs. The Bear Case

The decision by the EM Korea major shareholder creates a classic conflict for investors. Do you follow the insider confidence, or do you heed the warning signs in the financial statements? Here’s a breakdown of both sides.

The Bull Case (Potential Positives)

- •Strengthened Management Stability: A larger controlling stake allows for decisive, long-term strategic planning without the threat of external pressures, potentially leading to a more focused turnaround.

- •Positive Market Signal: Insider buying, especially by the largest shareholder, is often interpreted by the market as a sign that the stock is undervalued, which could boost investor sentiment.

- •Focus on Core Strengths: Stable leadership may double down on the highly profitable Defense/Aerospace sector, channeling resources to maximize its growth.

The Bear Case (Potential Negatives & Risks)

- •Persistent Underperformance: Increased ownership doesn’t magically fix operational issues. If the Machine Tools and Power divisions continue to struggle, losses could offset gains from the defense sector.

- •Weak Financial Structure: The company’s high debt-to-equity ratio and rising financial costs are significant burdens that a change in ownership percentage does not alleviate on its own. For more on this, see this guide on how to analyze a company’s balance sheet.

- •Macroeconomic Headwinds: Global economic slowdown, volatile commodity prices, and fluctuating interest rates pose external threats that could further dampen performance, as noted by leading financial analysts at authoritative sources like Bloomberg.

A Smart Investment Strategy for EM Korea

Given the conflicting signals, a prudent and watchful approach is necessary. A complete EM Korea stock analysis must be grounded in monitoring key performance indicators.

- •Monitor Turnaround Efforts: Keep a close eye on quarterly reports for signs of a turnaround in the underperforming divisions. Is management’s new strategy working?

- •Track Defense Sector Growth: Verify that the Defense/Aerospace segment continues its strong performance and look for announcements of new contracts or projects.

- •Assess Financial Deleveraging: Look for concrete steps to improve the balance sheet, such as debt reduction or improved cash flow management, beyond one-off capital raises.

Conclusion: A Cautious Opportunity

The increased stake by Shinwha Precision is a compelling, positive signal for EM Korea’s governance and long-term strategic direction. However, this confidence must be weighed against the company’s stark financial realities. True, sustainable growth in the stock price will not come from ownership changes alone but from a fundamental improvement in performance and financial stability. Investors should view this as a time for diligent monitoring rather than immediate action, waiting for concrete evidence that the company’s operational strength can match its shareholder’s conviction.