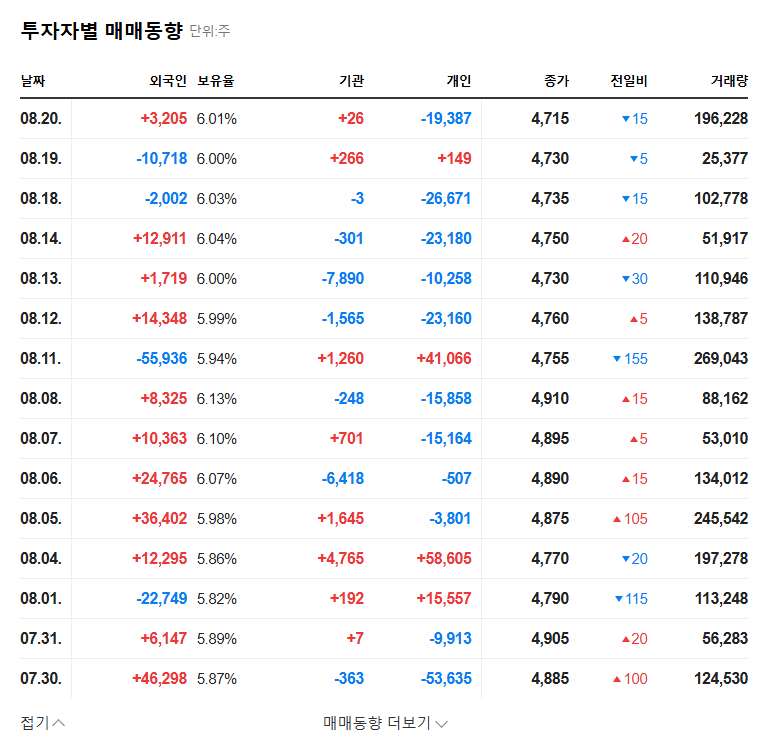

The recent Nextchip stake sale by its largest shareholder, NCN, has sent shockwaves through the investment community. This significant move, involving a 12.24% reduction in shares, isn’t just a simple portfolio adjustment; it’s a critical event that demands a thorough Nextchip financial analysis. For investors, the key question is whether this is a strategic pivot or a desperate signal from a company grappling with severe financial distress, including a state of complete capital impairment.

This article dives deep into the official disclosure, breaking down the implications for Nextchip’s future, its stock performance, and what stakeholders should watch for next. We will analyze the reasons behind the sale and connect them to the company’s precarious financial health to provide a clear, actionable investment perspective.

The Event: NCN’s Substantial Reduction in Nextchip Stake

On November 12, 2025, Nextchip Co., Ltd. filed a ‘Report on the Status of Large Shareholdings,’ revealing a significant change. NCN, the largest shareholder, drastically reduced its stake from 46.62% to 34.38%. A 12.24 percentage point drop from a shareholder whose stated purpose was ‘management influence’ is highly unusual and immediately raises red flags. The official reasons cited are a complex mix of financial maneuvers.

- •Reporting Entity: NCN Co., Ltd.

- •Previous Stake: 46.62%

- •New Stake: 34.38%

- •Net Change: -12.24%

- •Official Source: View DART Report

While reasons like option exercises and block trades were cited, these technical explanations often mask a deeper underlying issue. For NCN Nextchip, this move cannot be viewed in isolation from the company’s alarming financial condition.

Financial Analysis: The Crisis of Complete Capital Impairment

The context for the Nextchip stake sale is the company’s dire financial health. Nextchip, which specializes in automotive semiconductors for a growing ADAS market, is paradoxically facing insolvency. The most critical issue is its state of complete capital impairment.

What is Complete Capital Impairment?

This is a severe financial state where a company’s total liabilities exceed its total assets, resulting in negative shareholder equity. Essentially, the company’s accumulated losses have wiped out all the capital invested by its shareholders. As of Q3 2025, Nextchip’s debt-to-equity ratio was a staggering -4,537.67%, a clear indicator of this crisis. For investors, this means the company is technically bankrupt and poses a significant risk of delisting if not resolved.

The sale of shares by a major shareholder during a period of complete capital impairment is often interpreted as a loss of confidence in the company’s ability to recover, amplifying negative sentiment in the market.

Compounding Risk Factors for Nextchip Stock

- •Persistent Losses: The company continues to post significant operating and net losses with no clear path to profitability.

- •High R&D Burn: While necessary for innovation, a high R&D expense ratio is draining cash reserves without generating sufficient revenue.

- •Market & Financial Risks: Heavy reliance on the Chinese market, currency fluctuations, and outstanding convertible bonds add layers of uncertainty.

Investor Outlook & Action Plan

The combination of the major shareholder’s exit and the grave financial situation paints a bleak picture for the Nextchip stock. The market is likely to view this as a ‘very negative’ signal, leading to significant downward pressure on the stock price.

Investment Recommendation: Very Negative (Sell/Hold)

At present, a ‘Sell’ or ‘Hold’ stance is strongly advised. Without a drastic and credible turnaround plan that addresses the fundamental issue of Nextchip capital impairment and secures a path to profitability, any positive momentum will likely be short-lived. Investors should not be swayed by potential short-term bounces but focus on the long-term viability of the business. For more information on market trends, you can refer to authoritative sources like Reuters Financial News.

What to Monitor Moving Forward:

- •Capital Increase Plan: Closely watch the success and execution of Nextchip’s proposed capital increase. Will NCN participate? Will new investors step in?

- •Management Stability: NCN’s reduced influence could lead to management instability or strategic shifts. Any further changes will be critical.

- •Quarterly Financials: Look for any signs of improvement in revenue, a reduction in losses, and progress toward resolving the negative equity.

Navigating this situation requires extreme caution. For further reading, see our guide on analyzing financially distressed companies.

Frequently Asked Questions (FAQ)

Q1: What does the NCN Nextchip stake sale mean for investors?

It is a significant negative signal. When a major shareholder with management influence sells a large stake during a financial crisis, it suggests a lack of confidence in the company’s recovery, which can lead to a sharp decline in stock price.

Q2: Can Nextchip recover from complete capital impairment?

Recovery is possible but extremely difficult. It would require a massive infusion of new capital through a successful rights offering, a drastic operational turnaround to achieve profitability, or a strategic acquisition. The path to recovery is fraught with uncertainty.

Q3: How will this affect Nextchip’s stock in the short term?

In the short term, the stock will likely face intense selling pressure. The news of the stake sale, combined with the underlying financial weakness, will erode investor confidence and could lead to a significant price drop.