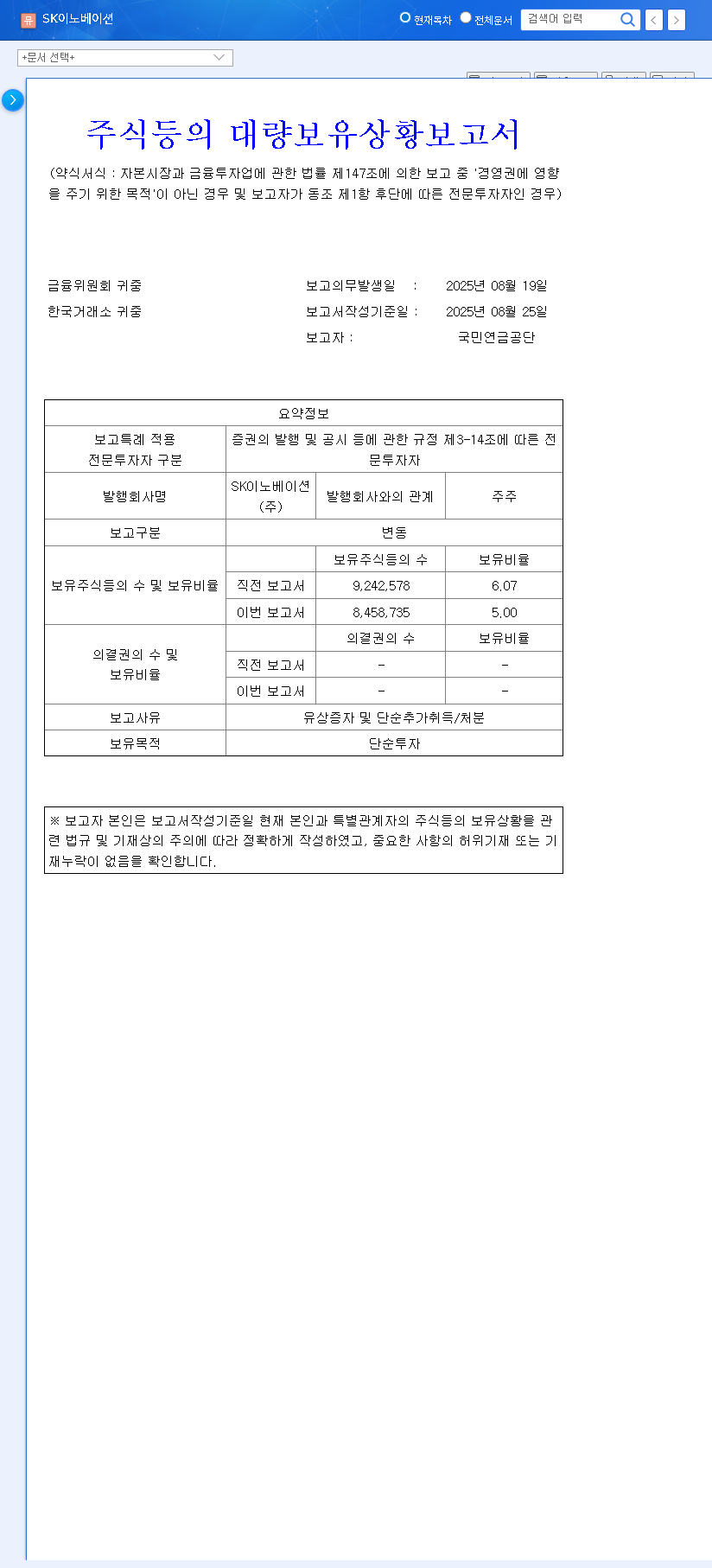

The recent reduction of the SK Innovation stake by South Korea’s National Pension Service (NPS) has sent ripples through the investment community. As the nation’s largest institutional investor, any portfolio adjustment by the NPS is scrutinized for deeper meaning. This move, cutting their holding from 6.07% to 5.00%, raises critical questions: Is this a vote of no confidence in SK Innovation’s future, or simply a routine portfolio rebalancing? For current and potential investors, understanding the context behind this decision is paramount.

This comprehensive analysis will dissect the NPS’s decision, perform a deep dive into SK Innovation’s current financial health and business segments, and provide a strategic outlook for investors navigating this uncertain period. We will explore both the short-term market reactions and the long-term fundamental drivers that will truly define the trajectory of SK Innovation stock.

The Filing Details: What Exactly Happened?

On October 1, 2025, the National Pension Service officially reported a change in its major shareholding status for SK Innovation. The disclosure revealed a 1.07 percentage point decrease in their ownership, a significant move for an investor of this scale.

Official Report Summary:

Reporting Entity: National Pension Service

Previous Holding: 6.07%

Current Holding: 5.00%

Change: -1.07%

Stated Reason: Simple investment; participation in capital increase and additional acquisition/disposal.

The stated purpose of ‘simple investment’ implies that the NPS is not seeking management control and retains the flexibility to adjust its holdings based on market performance and its own internal strategies. While a 1.07% reduction might seem minor, it represents a substantial volume of shares being sold, which can create downward pressure on the stock price and signal caution to other market participants. You can view the full filing directly from the Official Disclosure (DART report).

SK Innovation Analysis: Under the Hood

To understand why the NPS might be adjusting its SK Innovation stake, we must look beyond the headline and analyze the company’s fundamental health and strategic direction.

A Company in Transition

Following its 2024 merger with SK E&S, SK Innovation has been aggressively repositioning itself as a comprehensive energy company. The strategy is to pivot from its legacy petroleum and chemical businesses towards future growth engines in green energy. However, this transition is capital-intensive and fraught with challenges. The current business is a mix of old and new:

- •Petroleum/Chemical (68% of sales): The traditional cash cow, but highly susceptible to volatile global oil prices.

- •Battery Business (9% of sales): Positioned to capture growth from the expanding EV market, but currently a major drain on profitability due to high investment costs and fierce competition.

- •E&S CIC (16% of sales): Focused on LNG, hydrogen, and renewables, representing the company’s long-term green energy ambitions.

Financial Health Check (H1 2025)

A look at the recent financial data reveals some concerning trends that likely factored into the NPS’s decision. The first half of 2025 showed sluggish performance, primarily dragged down by the battery division’s persistent losses and mounting financial costs.

The most glaring red flag is the company’s leverage. With a debt-to-equity ratio of 678.57%, SK Innovation is operating with a significant amount of debt. This high leverage makes the company vulnerable to rising interest rates and can limit its ability to fund future growth without further diluting shareholder equity. This financial strain is a key risk that prudent investors like the NPS would be monitoring closely. For more on industry trends, you can read about the global EV battery market challenges.

Investor Outlook: How to Interpret This Move

The reduction in the SK Innovation stake by the NPS can be seen as a risk-management measure. It doesn’t signal an impending collapse but rather a cautious stance given the company’s current challenges.

The Bear Case: Key Risks to Watch

- •Delayed Battery Profitability: The path to profitability for the battery segment remains uncertain. Intense competition, particularly from Chinese manufacturers like CATL, and fluctuating raw material costs could prolong losses.

- •High Financial Burden: The substantial debt load is a major headwind. High interest payments eat into profits and reduce financial flexibility.

- •Macroeconomic Volatility: As a global business, SK Innovation is exposed to swings in oil prices, currency exchange rates (especially KRW/USD), and global economic growth.

The Bull Case: Long-Term Opportunities

- •EV Market Growth: The long-term trend towards vehicle electrification is undeniable. As a key player in the battery supply chain, SK Innovation is well-positioned to benefit if it can navigate the short-term profitability hurdles. Explore our analysis of the renewable energy sector for more context.

- •E&S Synergies: The integration of SK E&S provides a strong foothold in the growing LNG and hydrogen markets, offering diversification and a hedge against the volatility of the oil and battery sectors.

- •Valuation: The recent stock price pressure may present a compelling entry point for long-term investors who believe in the company’s strategic pivot and can tolerate the associated risks.

Actionable Investment Strategy

The NPS’s move should not trigger panic selling. Instead, it should serve as a prompt for investors to re-evaluate their thesis on SK Innovation based on fundamentals.

For Short-Term Investors: The stock is likely to experience continued volatility. A wait-and-see approach is prudent. Look for clear signs of improvement in the battery division’s margins or a concrete plan for debt reduction before committing capital.

For Long-Term Investors: If you believe in the green energy transition and SK’s role within it, the current climate may offer an opportunity for phased accumulation. Rather than making a single large investment, consider a dollar-cost averaging strategy to build a position over time, mitigating the risk of short-term price drops. The key is to focus on fundamental progress—specifically, the timeline for battery business profitability and improvements in the company’s balance sheet—rather than on the day-to-day stock price fluctuations.