A significant development concerning JaeYoung Solutec (049630) has captured the market’s attention, raising critical questions for current and potential investors. The company’s representative reporter, Kim Dae-yong, has executed a substantial sale of his shares. This action, especially when juxtaposed with the company’s recent financial performance, could be interpreted as a major red flag. Is this a simple portfolio adjustment, or a concerning signal from an insider about the fundamental health of JaeYoung Solutec (049630)? This comprehensive analysis will explore the implications of this event, dissect the company’s H1 2025 earnings, and provide a clear action plan for investors.

The Details of the JaeYoung Solutec Share Sale

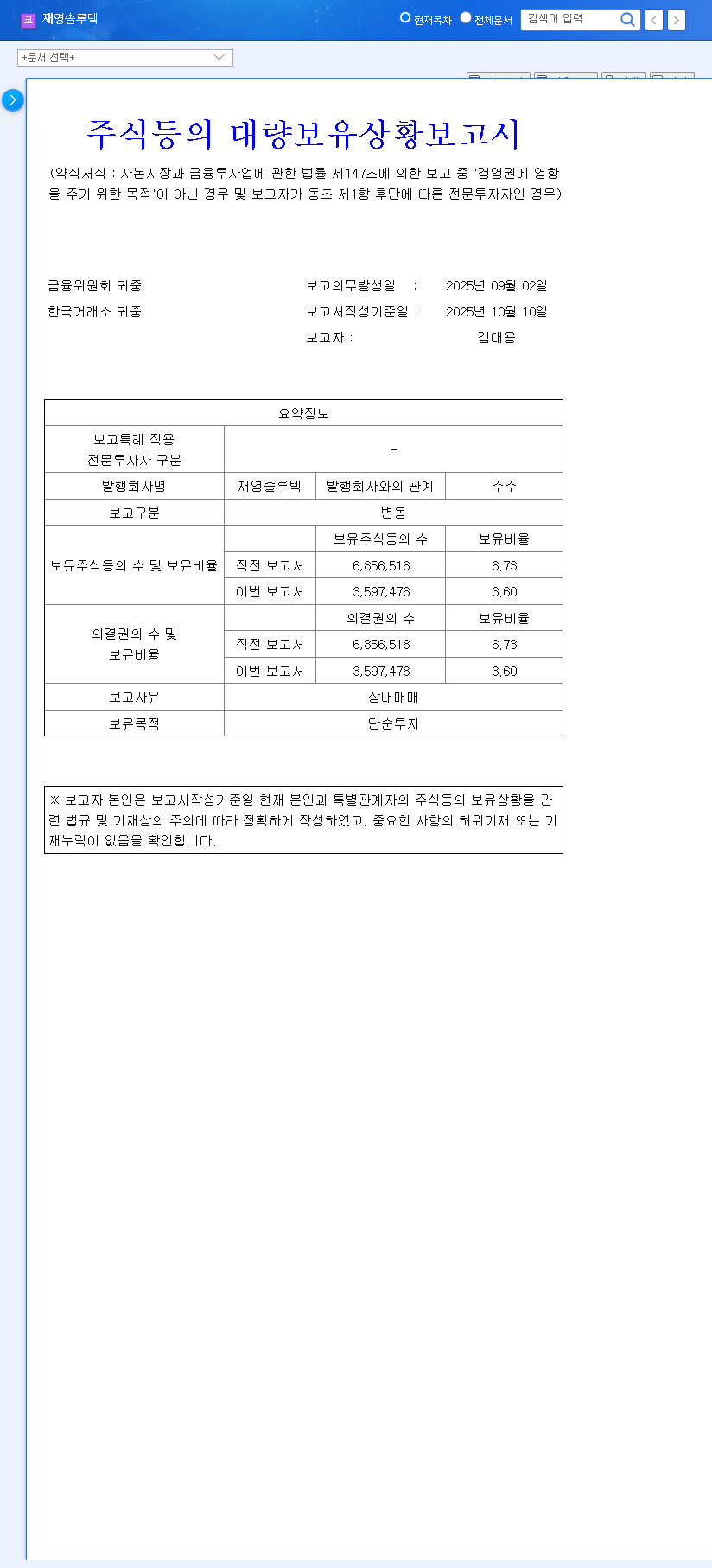

On October 11, 2025, a mandatory disclosure sent ripples through the investment community. According to the filing, Kim Dae-yong’s ownership stake in JaeYoung Solutec (049630) was reduced from 6.73% to just 3.60%. This represents a significant offloading of 3.13 percentage points, executed via a direct market sale. The official filing can be viewed here: Official Disclosure (DART).

For a company with a market capitalization of approximately KRW 91.6 billion, a single insider selling over 3% of the company’s total shares is a highly material event that cannot be overlooked. Such actions often precede periods of increased stock volatility and negative investor sentiment.

This type of transaction is often referred to as insider selling, and while not illegal, it is closely watched by analysts. When high-level executives sell large portions of their holdings, it can signal a lack of confidence in the company’s future prospects, prompting a re-evaluation by the broader market.

Financial Health: A Look Under the Hood (H1 2025)

The timing of the JaeYoung Solutec share sale is particularly alarming when viewed in the context of its recent financial report. The H1 2025 results paint a picture of a company struggling with profitability, despite top-line growth. For a deeper understanding of financial statements, you can review our guide to fundamental analysis.

Deteriorating Profitability & Balance Sheet Concerns

While revenue saw a healthy increase of 17.7% year-on-year to KRW 71.7 billion, the story ends there. The costs associated with generating that revenue ballooned, leading to a severe profitability crisis.

- •Operating Income Collapse: Operating income plummeted to a mere KRW 270.45 million, a drastic reduction from the previous year, crushed by higher cost of goods sold and administrative expenses.

- •Net Loss Conversion: The company swung from a net profit of KRW 5.52 billion to a jarring net loss of KRW 2.95 billion. This indicates severe issues in managing expenses below the operating line.

- •Weakening Financial Position: Total assets decreased by 8.5%, driven by a reduction in cash equivalents. Meanwhile, total equity also decreased due to an increased accumulated deficit, a major red flag for long-term financial stability.

Core Business vs. Financial Reality

JaeYoung Solutec operates in a high-tech, promising sector. The company is a specialist in manufacturing actuators (OIS, AF, VCM), which are critical components for modern smartphone cameras. Its nano-optics segment is its sole revenue driver, and it holds a strong competitive advantage as the only domestic Korean producer capable of manufacturing a full lineup of actuator products. This aligns well with the technological trend toward more advanced smartphone cameras.

However, this operational strength is completely overshadowed by the grim financial results. A strong business model is meaningless if it cannot translate to profitability and a healthy balance sheet. The current situation suggests that despite its market position, the company is failing to manage costs and generate shareholder value.

Investor Action Plan & Stock Outlook

The combination of a major insider share sale and deteriorating fundamentals creates a powerfully negative signal for JaeYoung Solutec (049630). The market is likely to react negatively for several reasons:

- •Loss of Confidence: The CEO’s sale implies a potential lack of faith in the company’s ability to turn its performance around.

- •Supply Pressure: A 3.13% stake hitting the open market creates significant supply that can depress the stock price in the short to medium term.

- •Heightened Scrutiny: Investors will now look at future earnings reports with extreme skepticism, punishing any further signs of weakness.

Given these factors, our current recommendation for JaeYoung Solutec (049630) is a ‘SELL’. Investors should consider liquidating their positions to mitigate further risk. For those considering an entry, it is prudent to wait for multiple quarters of confirmed financial improvement and stability before reassessing.

Frequently Asked Questions

Q1: What was the exact scale of the JaeYoung Solutec share sale?

A1: Representative reporter Kim Dae-yong sold a 3.13 percentage point stake, reducing his total holdings from 6.73% down to 3.60% through a direct market sale.

Q2: How bad were JaeYoung Solutec’s recent earnings?

A2: In H1 2025, despite revenue growth, operating income collapsed, and the company reported a net loss of KRW 2.95 billion, signaling a severe deterioration in profitability and financial health.

Q3: Why is a major shareholder selling shares a negative sign?

A3: A large sale by a top insider can signal a lack of confidence in the company’s future. It also creates excess supply in the market, which can put significant downward pressure on the stock price.

Q4: What is the current investment recommendation for 049630 stock?

A4: Due to the combination of poor financial performance and the negative signal from the insider share sale, the current recommendation is a ‘SELL’ to avoid potential further losses.