In a significant development for investors monitoring the SAMPYO Cement Co., Ltd. stock (KRX: 038500), news of a major shareholder divestment has sent ripples through the market. With the company already navigating a challenging construction downturn, this move by KMUS One Co., Ltd. introduces a new layer of uncertainty. This analysis will break down the specifics of the share sale, explore the underlying causes, and evaluate the potential short-term and long-term impact on SAMPYO Cement’s share price and management stability.

This isn’t just a simple transaction; it’s a critical signal about insider confidence amidst severe market headwinds. Understanding the context is paramount for any current or prospective investor.

The Catalyst: A Major Shareholder Makes an Exit

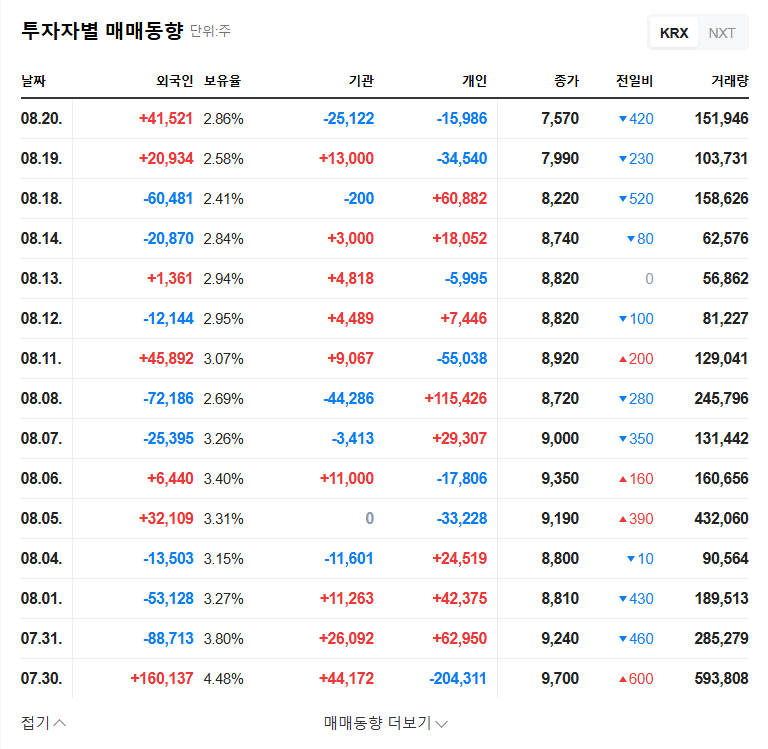

On November 10, 2024, an official disclosure confirmed that KMUS One Co., Ltd., a significant shareholder in SAMPYO Cement, drastically reduced its holdings. The stake was cut from 8.71% down to just 3.89%—a substantial decrease of 4.82 percentage points. Critically, KMUS One’s original holding purpose was cited as ‘management influence,’ which makes this sale more than a simple portfolio rebalancing. It signals a strategic withdrawal, raising immediate questions about the company’s future leadership and stability. The transaction was officially documented in a ‘Report on the Status of Large-scale Shareholding,’ which can be viewed in the Official Disclosure (DART).

Why Now? A Perfect Storm of Challenges

The decision by KMUS One was not made in a vacuum. It comes at a time when SAMPYO Cement is facing a convergence of internal performance issues and external market pressures, creating a ‘perfect storm’ for the company.

Severe Deterioration in Corporate Fundamentals

The company’s 2025 semi-annual report paints a bleak picture. Revenue plummeted by a staggering 58.3% year-over-year, while operating profit fell by an even more alarming 70.6%. This decline is not isolated to one segment; both the core Cement and Ready-Mixed Concrete businesses have suffered from a severe construction market slump. Despite a drop in some raw material costs, falling cement prices combined with rising electricity costs have squeezed profit margins. Furthermore, lower production volumes have increased the fixed cost burden per unit, eroding profitability from multiple angles.

Unfavorable Macroeconomic Environment

The broader economic landscape offers little relief. While there are hints of future interest rate cuts, current high rates continue to suppress new construction projects. A strengthening US Dollar and Euro against the Korean Won reflects a broader ‘risk-off’ sentiment in global markets. While falling international oil prices could reduce logistics and operational costs, this benefit is partially offset by market volatility and the overarching weakness in demand that it signals. For more on market trends, investors often consult sources like Bloomberg’s economic analysis.

Analysis: The Impact on SAMPYO Cement Co., Ltd. Stock

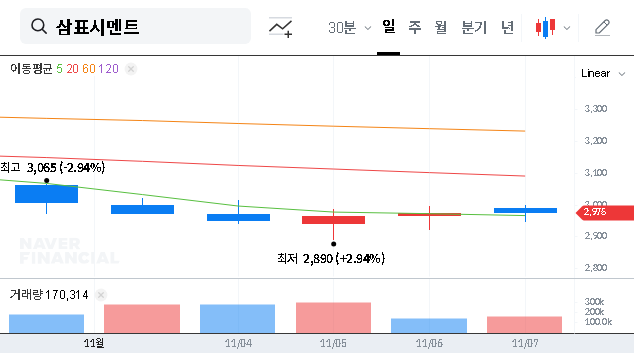

The large-scale SAMPYO Cement shareholder divestment is a bearish signal that is likely to amplify negative market sentiment and exert significant downward pressure on the stock price in the short term. Key consequences include:

- •Eroding Investor Confidence: A major insider cashing out raises red flags, suggesting a lack of faith in the company’s near-term recovery prospects.

- •Increased Selling Pressure: The process of offloading a large block of shares can create a supply-demand imbalance, potentially leading to further price declines as the market absorbs the new float.

- •Compounding Negative Momentum: This news, combined with the already poor financial performance, creates a powerful negative narrative that could scare away potential buyers and encourage existing shareholders to sell.

- •Management Stability Concerns: The exit creates a power vacuum. While it could eventually lead to a new strategic investor, the immediate future is filled with uncertainty about who will fill the void.

While SAMPYO Cement has made positive strides in ESG management and R&D, these long-term initiatives are likely to be overshadowed by the immediate negative sentiment. Investors interested in how such factors are weighed can read about our analysis of ESG investing trends.

Investor Action Plan & Strategic Outlook

Given the circumstances, a cautious and highly observant approach is warranted for anyone invested in or considering the SAMPYO Cement Co., Ltd. stock. A prudent strategy should involve the following steps:

- •Brace for Volatility: Expect heightened price swings in the coming weeks. Avoid making large, emotionally-driven trades and consider risk management tools like stop-loss orders.

- •Monitor Management News: Pay close attention to any announcements regarding the buyer of the divested shares. A strategic corporate buyer would be viewed more favorably than a simple financial investor.

- •Focus on Fundamental Triggers: Long-term recovery will depend entirely on a rebound in the construction market and improved company performance. Watch key industry indicators and the company’s next quarterly earnings report for signs of a turnaround.

- •Re-evaluate ESG Impact: Continue to assess if the company’s sustainability efforts are translating into tangible financial benefits or simply serving as corporate talking points.

In conclusion, the divestment by KMUS One Co., Ltd. is a significant negative catalyst that will likely weigh on the SAMPYO Cement Co., Ltd. stock in the short term. Investors should prioritize caution, monitor new information closely, and wait for clear evidence of a fundamental business recovery before making any significant investment decisions.