The recent announcement regarding the ASIA CEMENT CO.,LTD. share retirement has sent ripples through the investment community. In a strategic move to bolster shareholder value amidst a turbulent construction market, the company plans to retire ₩5 billion in treasury shares. This decision, while seemingly a standard corporate action, carries significant weight in the current economic climate. For investors holding or considering Asia Cement stock, understanding the nuances of this move is critical for navigating what comes next. This comprehensive analysis will dissect the decision, evaluate its impact on the company’s fundamentals, and provide a strategic outlook for investors.

The Core Announcement: A ₩5 Billion Share Buyback

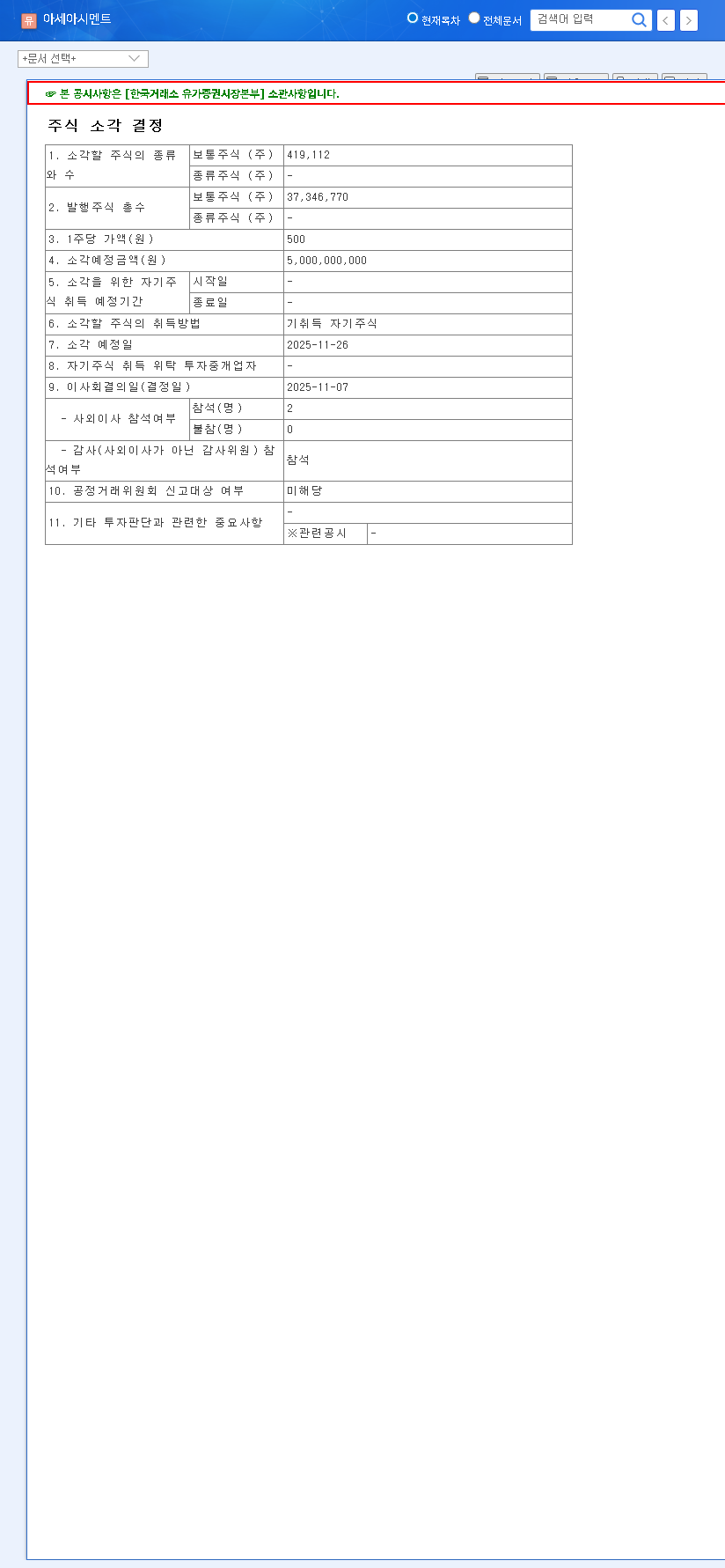

On November 7, 2025, ASIA CEMENT CO.,LTD. (Market Cap: ₩444.4 billion) formally disclosed its resolution to retire a substantial portion of its existing treasury shares. This move is a clear signal of the management’s confidence and commitment to its shareholders. The key details are as follows:

ASIA CEMENT CO.,LTD. will retire 419,112 common shares, with an approximate value of ₩5 billion. This represents 1.12% of the company’s total market capitalization. The retirement is scheduled for completion by November 26, 2025. – Official Disclosure (DART)

By reducing the total number of outstanding shares, the value of each remaining share theoretically increases. This action directly impacts metrics like Earnings Per Share (EPS) and is often interpreted by the market as a bullish signal, suggesting the company believes its stock is undervalued.

Deep Dive Analysis: Fundamentals and Market Headwinds

Company Financial Health & Competitive Strengths

The H1 2025 report painted a challenging picture, with revenue and profit declining due to a significant slump in the construction sector and growing risks from real estate project financing (PF). However, ASIA CEMENT is not without its strengths. The company boasts several competitive advantages, including ownership of high-quality limestone mines, ongoing development of eco-friendly cement products, and a strong reputation solidified by its role in major projects like the Lotte World Tower. Financially, the company maintains a stable position with an improving debt-to-equity ratio and robust cash holdings of ₩123.1 billion.

Impact of the ASIA CEMENT CO.,LTD. Share Retirement

The ₩5 billion expenditure for this retirement represents only 4.06% of the company’s cash reserves, indicating a minimal financial strain. The expected positive impacts are multifaceted:

- •Enhanced Shareholder Value: The primary goal is to increase per-share metrics like EPS, which directly benefits existing shareholders and can attract new investment. It’s a powerful statement of confidence in a difficult market.

- •Improved Financial Ratios: Reducing the number of shares in circulation can have a positive, albeit minor, cosmetic effect on key financial ratios like Return on Equity (ROE), making the company appear more efficient.

- •Positive Market Signaling: This action communicates to the market that management believes the company’s intrinsic value is higher than its current stock price, which can build investor trust and provide price support.

Macroeconomic and Industry Pressures

Despite the positive corporate action, external factors remain a significant concern. The overarching cement industry outlook is tied to the health of the construction market, which is currently weak. For a broader perspective on global economic trends impacting commodities, sources like Bloomberg’s Market Analysis provide valuable context. Key factors to monitor include volatile international oil and coal prices, which directly affect production costs, and persistently high interest rates, which impact borrowing and investment. While the share retirement is a plus, these macroeconomic headwinds cannot be ignored.

Outlook and Strategic Investment Thesis

Short-Term vs. Long-Term Perspective

In the short term, the share retirement is likely to improve investor sentiment and create a floor for the stock price, providing downside protection. However, a major price surge is unlikely until the fundamental issues within the construction market begin to resolve. The long-term performance of Asia Cement stock hinges on a recovery in construction, stable raw material costs, and the successful execution of its diversification and eco-friendly product strategies. For more information, you might be interested in our deep dive into the South Korean construction sector.

Actionable Plan for Investors

When considering an investment, it’s crucial to weigh the company’s proactive shareholder policies against the challenging market backdrop. Here are key points to consider:

- •Acknowledge the Positive: The share retirement is an unambiguous positive for shareholder returns and demonstrates prudent capital allocation.

- •Evaluate the Risks: The construction slump and commodity price volatility are real and significant risks that directly impact profitability. A comprehensive investment decision must account for these factors.

- •Monitor Key Indicators: Watch for signs of a turnaround, such as an increase in new construction orders, government-led SOC (Social Overhead Capital) investment, or a stabilization of energy prices. These will be the true catalysts for long-term growth.

Disclaimer: This analysis is for informational purposes only and is based on publicly available data. Investment decisions should be made based on your own research and risk tolerance.