The SGC Energy Q3 Earnings Shockwave: A Detailed Analysis

The latest SGC Energy Q3 earnings report for 2025 sent a significant shockwave through the investment community. While top-line revenue showed modest growth, a precipitous drop in operating profit and an alarming shift to a net loss have ignited serious concerns about the company’s health and future trajectory. This comprehensive SGC Energy analysis will dissect the performance numbers, explore the fundamental reasons behind the decline, and provide a clear-eyed view of the implications for investors considering SGC Energy stock.

Deconstructing the Q3 2025 Performance Numbers

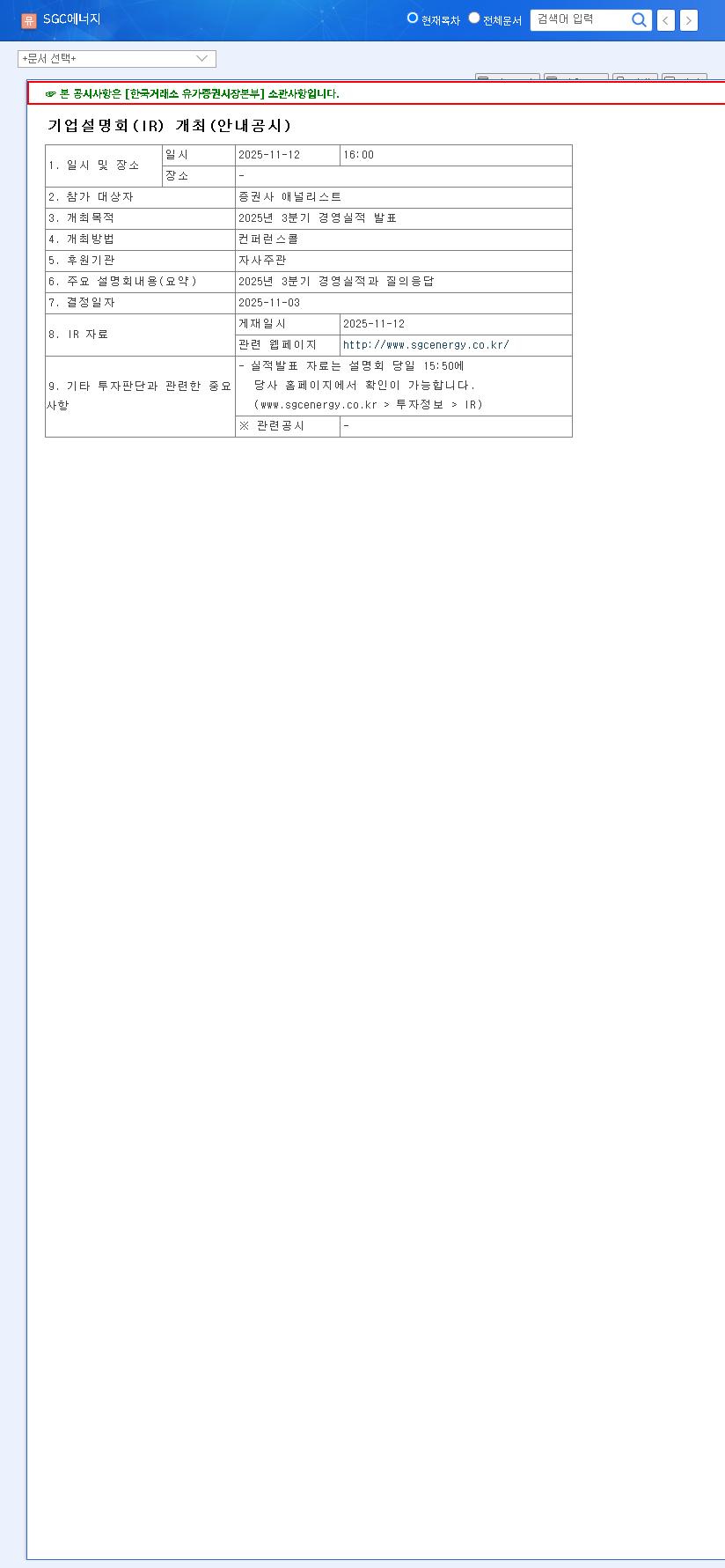

On November 12, 2025, SGC Energy Co., Ltd. released its provisional operating results, revealing a performance that fell far short of market expectations. The headline figures paint a stark picture of the challenges faced during the quarter. These figures are based on the company’s provisional filing, which can be viewed in the Official Disclosure on the DART system.

- •Revenue: KRW 598.9 billion (a 10.5% increase year-over-year).

- •Operating Profit: KRW 25.4 billion (a staggering 42.7% decrease year-over-year).

- •Net Income: KRW -15.1 billion (a complete reversal from a KRW 11.2 billion profit in the same period last year).

The slight revenue increase masks the deep-seated issues within the company’s profitability. The dramatic collapse in operating profit and the swing to a net loss are the critical red flags demanding further investigation.

While revenue grew, the core operational efficiency of SGC Energy appears to be under severe strain, turning what should have been a stable quarter into a significant loss-making period.

Unpacking the Root Causes of the Profitability Crisis

This poor SGC Energy performance is not the result of a single isolated event but a confluence of issues across its primary business segments.

Power & Energy Segment: The SMP Squeeze

The core Power Generation and Energy segment saw its operating profit plummet from KRW 90.5 billion to just KRW 23.4 billion in the first half of the year. The primary culprit was a sharp decline in the System Marginal Price (SMP), the standard price for wholesale electricity. Even with increased sales of Renewable Energy Certificates (RECs), the revenue generated was insufficient to compensate for the lower electricity prices. On a positive note, the strategic initiation of the Carbon Capture & Utilization (CCU) business signals a forward-looking approach to sustainable energy, though its financial impact is not yet material.

Construction & Real Estate: A Tale of Two Markets

The construction arm, SGC E&C Co., Ltd., demonstrated resilience through its plant EPC and construction businesses, buoyed by strong overseas sales. However, this international success is contrasted by a contracting domestic construction market. Rising material costs and intense competition at home are creating significant headwinds that could challenge future profitability management.

Glass Segment: Facing Structural Headwinds

The Glass business segment was a notable weak spot, with a significant drop in domestic sales of glass bottles. This underperformance points to an urgent need for either a comprehensive business restructuring or a strategic pivot to enhance profitability in a competitive market.

Investment Implications: What This Means for SGC Energy Stock

For current and prospective investors, understanding the short and long-term impacts of this earnings report is critical for making informed decisions. The confluence of internal business challenges and external macroeconomic pressures, as reported by major outlets like Reuters, creates a complex outlook.

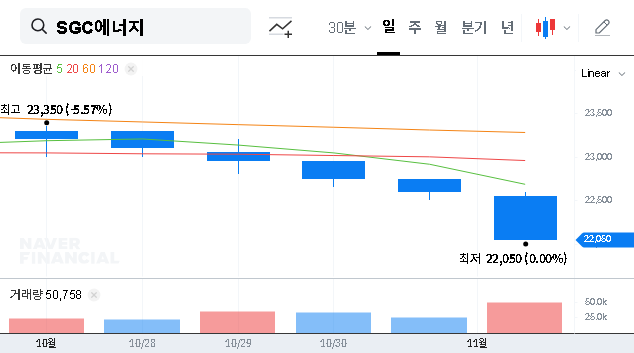

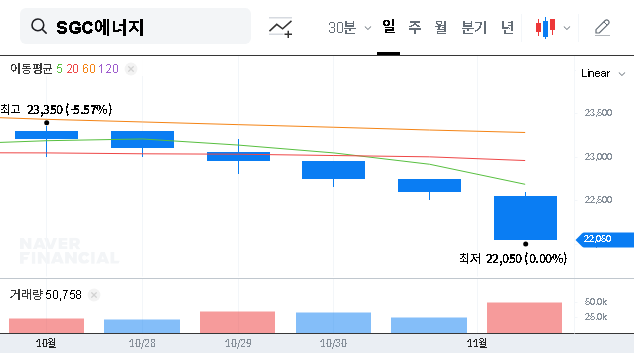

Short-Term Impact: Stock Price Pressure & Investor Anxiety

In the immediate term, the SGC Energy stock price is likely to face significant downward pressure. Earnings that so drastically miss consensus estimates often trigger sell-offs. This will likely be compounded by weakened investor sentiment and potential downgrades in target prices from securities firms, creating a negative feedback loop.

Mid-to-Long-Term View: A Call for Strategic Overhaul

Looking ahead, the market will be watching for decisive action. The path to recovery for SGC Energy depends on a successful overhaul of its underperforming segments and the stabilization of its core energy business. The high debt levels, though recently improved, become a greater concern when profitability falters. Persistent poor performance could risk a credit rating downgrade, which would increase financing costs. For those interested in broader market trends, you can review our guide to navigating volatile energy stocks.

A Strategic Roadmap for Recovery

To regain investor confidence, SGC Energy must execute a clear and effective turnaround plan. Investors should monitor the company’s progress on these key fronts:

- •Profitability Restoration: Implement concrete strategies to hedge against SMP volatility and improve power generation efficiency.

- •Portfolio Restructuring: Make tough decisions regarding the Glass business to enhance its fundamental competitiveness or divest.

- •Accelerate New Ventures: Focus all efforts on making the CCU business a tangible contributor to the bottom line as quickly as possible.

- •Enhance Market Communication: Proactively explain the reasons for the downturn and present a credible roadmap for recovery to rebuild trust.

In conclusion, the SGC Energy Q3 earnings report is a clear wake-up call. While the challenges are significant, they also present an opportunity for management to demonstrate strategic acumen and reset the company on a path toward sustainable growth. For investors, this is a time for caution, diligence, and a close watch on the execution of the company’s recovery plan.