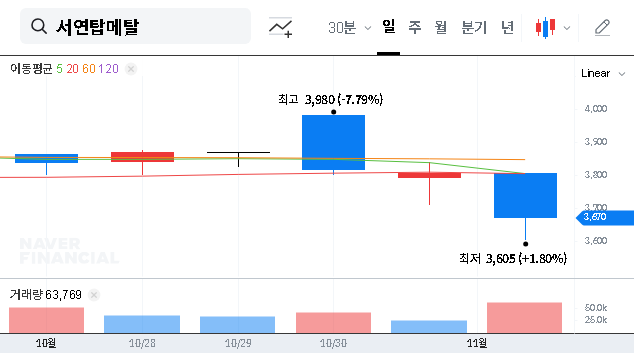

A recent development in SEOYON TOPMETAL stock (019770) has captured the market’s attention: a significant share acquisition by its major shareholder. This move, explicitly intended to ‘influence management rights,’ raises a critical question for investors. Is this a vote of confidence signaling future growth, or merely a defensive maneuver to stabilize a company facing fundamental headwinds? This comprehensive SEOYON TOPMETAL investment analysis will dissect the shareholder action, delve into the concerning H1 2025 financial report, and evaluate the macroeconomic landscape to provide a clear, actionable outlook.

The Major Shareholder’s Move: A Deeper Look

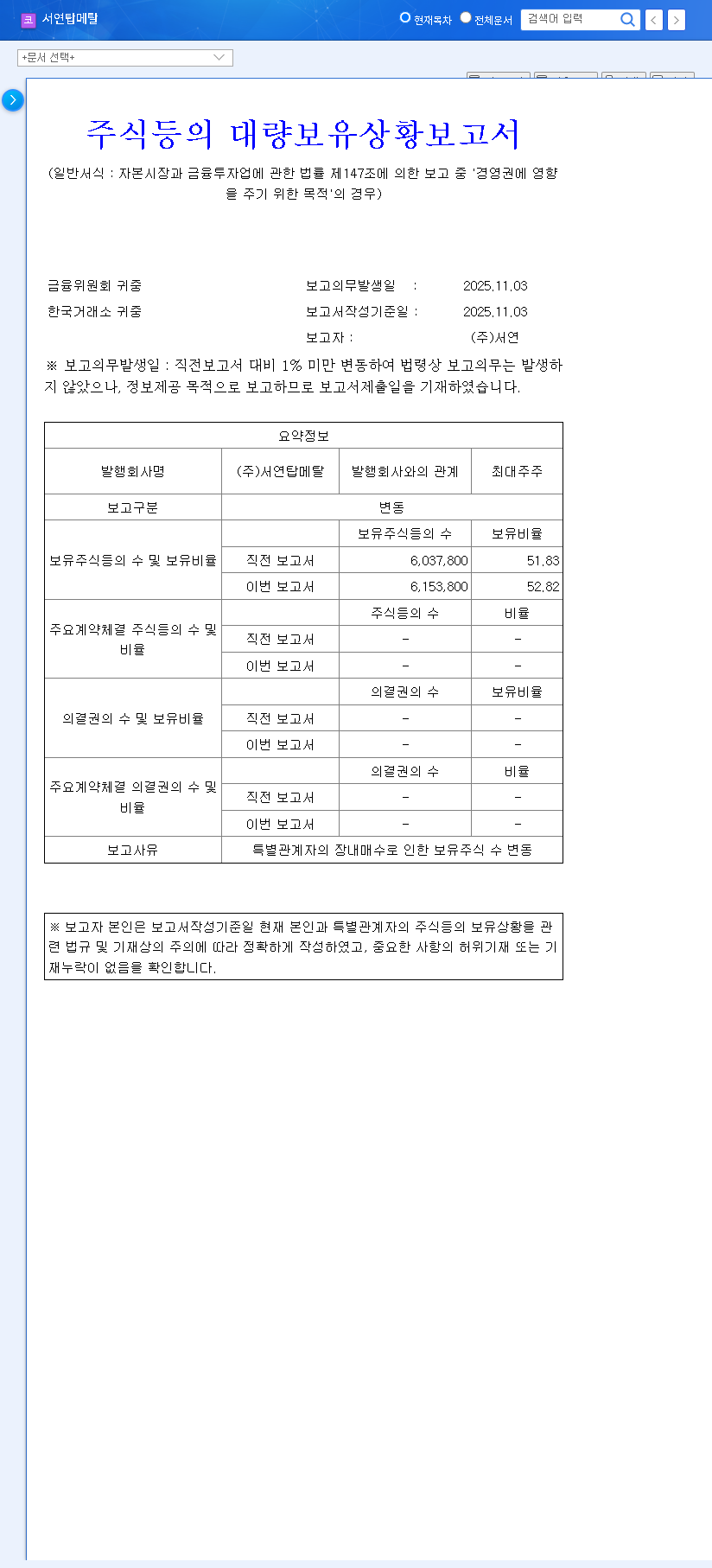

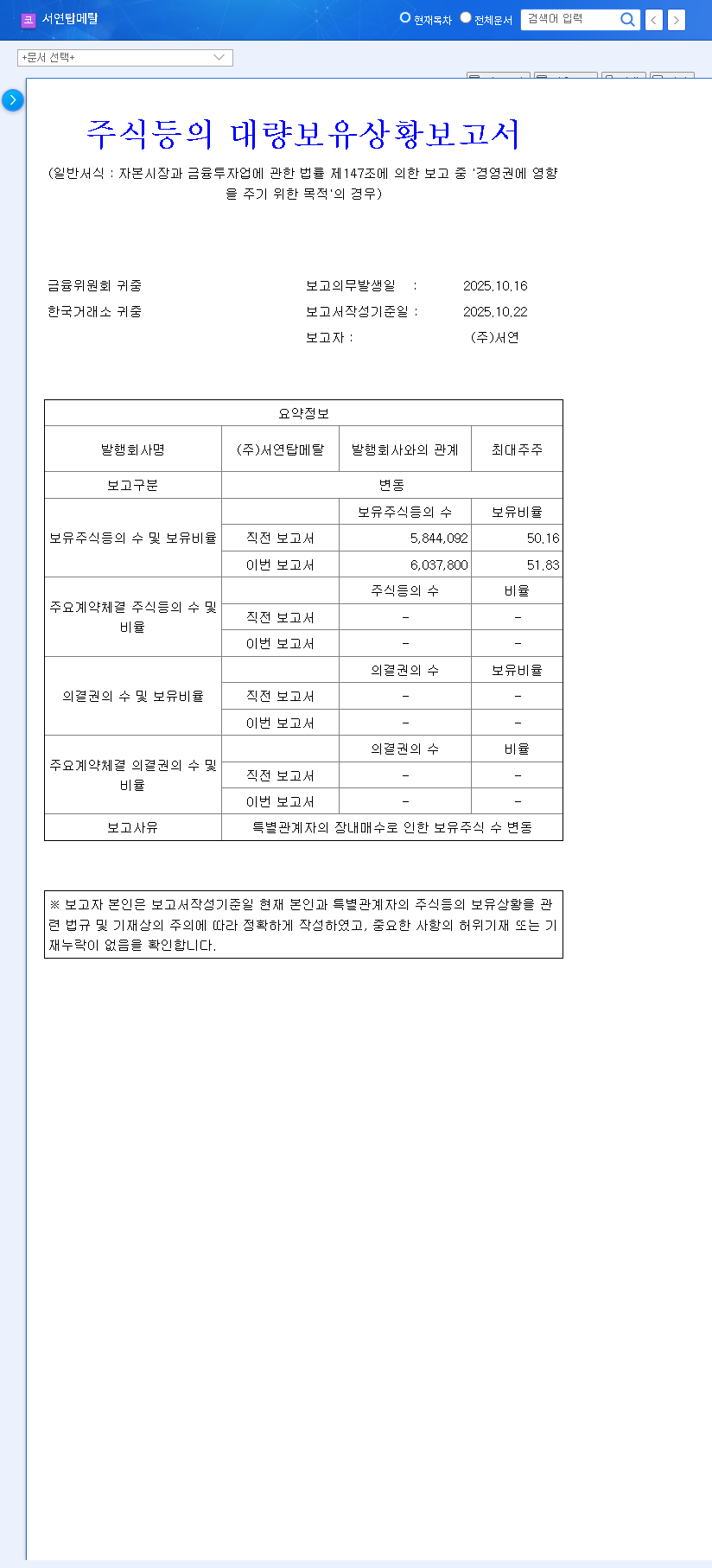

SEOYON TOPMETAL recently disclosed that related parties, led by ‘Seoyon’, executed open market purchases to bolster their holdings. The total stake increased from 51.83% to 52.82%, a rise of 0.99 percentage points. While seemingly small, the stated purpose—’influence on management control’—is highly significant. This action solidifies the major shareholder’s control well above the 50% threshold, signaling a commitment to steer the company’s long-term strategy and enhance corporate value. The details of this transaction were made public in an Official Disclosure on DART (Korea’s electronic disclosure system).

For the market, such a move is often interpreted as a bullish signal. It suggests insiders believe the company’s stock is undervalued and are willing to invest their own capital. This can temporarily boost investor sentiment and provide a floor for the stock price. However, this confidence must be weighed against the company’s actual performance.

Fundamental Headwinds: Analyzing the H1 2025 Financials

Despite the shareholder’s positive action, the SEOYON TOPMETAL financials for the first half of 2025 paint a challenging picture. Several key indicators point to persistent issues that cannot be ignored.

The core problem remains: declining revenue across all key business segments paired with eroding profitability. This suggests deep-seated operational or market-related challenges that a change in shareholding alone cannot fix.

Persistent Revenue Decline

In Q2 2025, total revenue fell to KRW 103.8 billion, a stark 11.6% decrease year-over-year. This was not isolated to one area; all major business units—injection molds, press molds, and machinery—suffered revenue drops ranging from 30-50%. The poor performance of the core mold business is a significant red flag for the company’s primary revenue stream.

Worsening Profitability

Compounding the revenue issue, profitability has significantly deteriorated. A rising cost of goods sold (COGS) and increased selling, general, and administrative (SG&A) expenses have squeezed margins. Consequently, both operating profit and net profit saw substantial year-over-year declines, confirming a negative trend in operational efficiency and financial health.

Structural Vulnerabilities and Strategic Risks

A thorough SEOYON TOPMETAL investment analysis must look beyond the immediate numbers to the underlying business structure, which reveals several vulnerabilities.

- •High Cyclical Sensitivity: The company’s focus on automotive molds and construction equipment parts makes it highly susceptible to global economic cycles. A slowdown, as indicated by recent global economic reports, directly translates to lower demand from its key industries, leading to earnings volatility.

- •Heavy Customer Concentration: Approximately 70% of revenue comes from a small pool of clients, including HD Hyundai Infracore and Seoyon E-Hwa. This over-reliance means any operational shift, inventory adjustment, or performance dip at these clients has an outsized negative impact on SEOYON TOPMETAL.

- •Insufficient R&D Investment: An R&D investment ratio of just 0.14% of revenue is critically low. In an era of rapid technological change (e.g., EV transition, smart manufacturing), this lack of investment raises serious concerns about the company’s ability to innovate and secure long-term growth engines.

Investor Outlook and Strategic Recommendations

The major shareholder’s stake increase is a clear positive signal of internal confidence. However, it is not a panacea for the company’s fundamental issues. A prudent investment in SEOYON TOPMETAL stock requires cautious optimism backed by tangible evidence of a turnaround. For more background, you can review our guide to investing in automotive suppliers.

Investors should focus on the following key areas before committing capital:

- •Evidence of a Performance Turnaround: Look for concrete signs of revenue stabilization and profitability improvement in the upcoming H2 2025 and H1 2026 reports. Monitor key customer order books and industry-wide demand trends.

- •Strategic Shifts and Management Efficiency: Watch for announcements related to cost-cutting, productivity enhancements, and, most importantly, strategic moves into new, high-value-added business segments to diversify revenue and secure future growth.

- •Continued Shareholder Actions: Observe if the major shareholder continues to increase their stake or makes other strategic announcements. This will be a key indicator of their long-term vision and confidence in the company’s direction.

In conclusion, while the shareholder news provides a short-term psychological boost, investment in SEOYON TOPMETAL (019770) should be predicated on a demonstrable improvement in its underlying financial and operational health. Without this, any stock price appreciation may be limited and unsustainable.