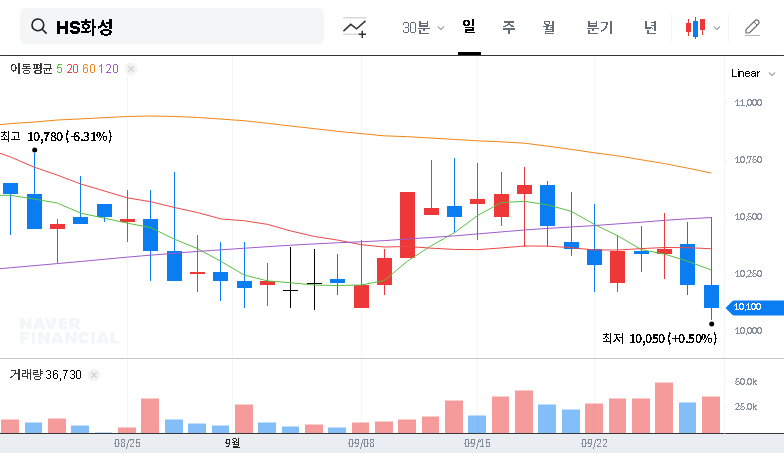

This comprehensive HS Hwasung 002460 investment analysis delves into the company’s recent landmark achievement: securing the ‘Jamwon Hanshin Town Small-Scale Reconstruction Project.’ Amid a challenging construction market, this ₩63.5 billion contract win represents a significant milestone. But what does it truly mean for investors and the future of HS Hwasung stock? We will explore the financial implications, strategic advantages, and potential risks to provide a clear, data-driven perspective.

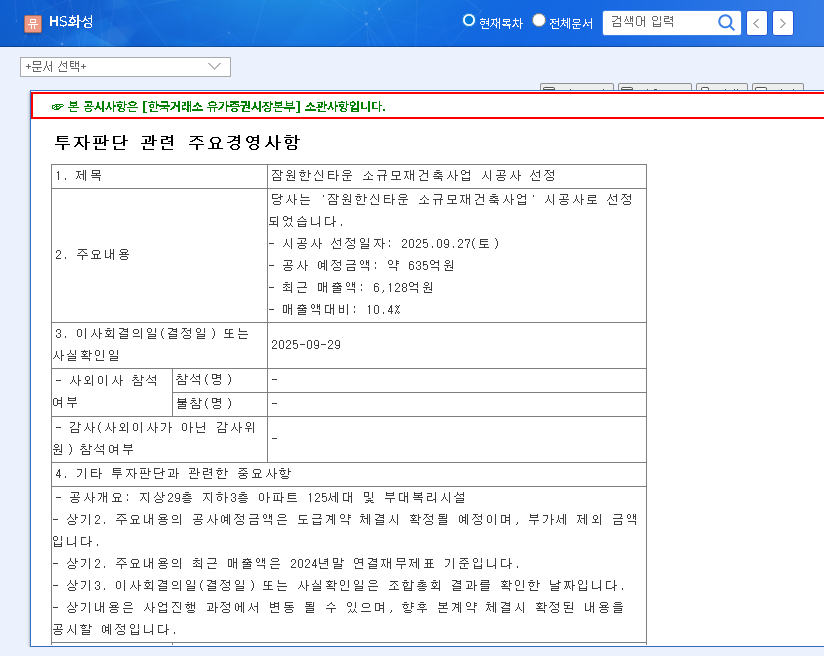

On September 27, 2025, HS Hwasung (002460) officially announced its selection as the main contractor for this key urban renewal project. The contract value is a substantial 10.4% of the company’s recent revenue, sending a strong positive signal to the market in a time of economic uncertainty.

Unpacking the Deal: The Jamwon Hanshin Town Reconstruction Project

The Jamwon Hanshin Town Reconstruction Project is a small-scale urban development initiative located in a prime area, making it a highly sought-after contract. HS Hwasung’s success in securing this deal amidst fierce competition underscores its robust bidding capabilities and solid reputation in the housing sector. According to the official filing, the project is valued at approximately ₩63.5 billion. For verification and further details, investors can refer to the DART Official Disclosure. This victory is not just a number; it’s a testament to the company’s resilience and strategic positioning.

Financial Deep Dive: Impact on HS Hwasung’s Bottom Line

A core part of any HS Hwasung 002460 investment analysis is understanding the direct financial consequences. This new order will have multifaceted effects on the company’s financial health.

1. Revenue Growth and Profitability Outlook

The ₩63.5 billion contract directly translates to future revenue, representing about 23.8% of the company’s H1 2025 revenue. This provides a significant boost to short-term sales forecasts. Small-scale reconstruction projects often boast better margins due to shorter timelines and lower upfront capital needs, potentially enhancing profitability. However, final profit will depend heavily on cost management, especially with volatile raw material prices, a key factor in the broader construction industry outlook.

2. Scrutinizing the Financial Structure

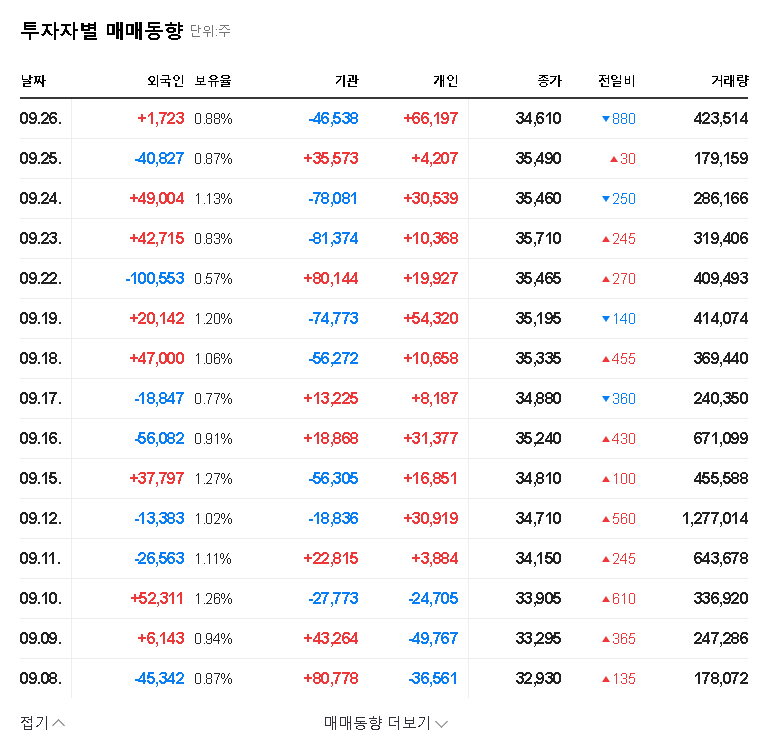

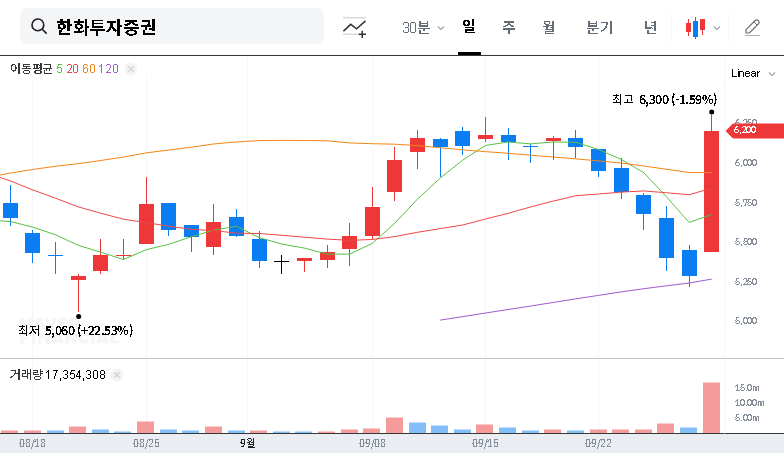

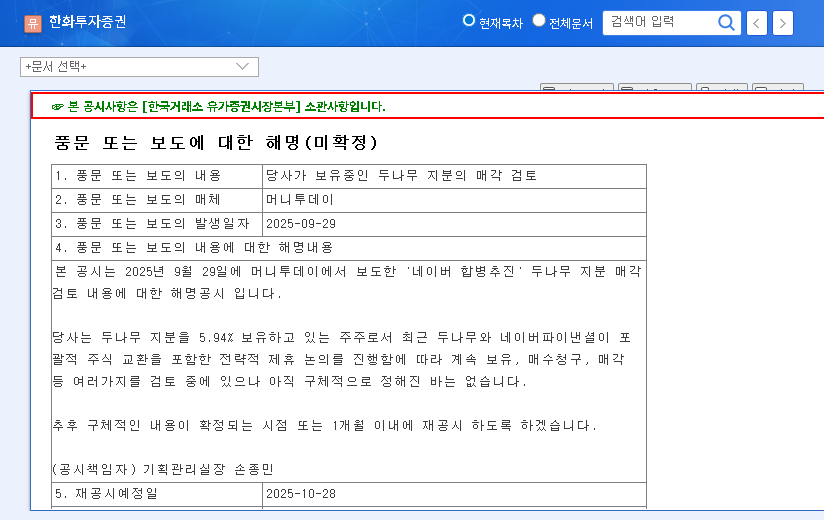

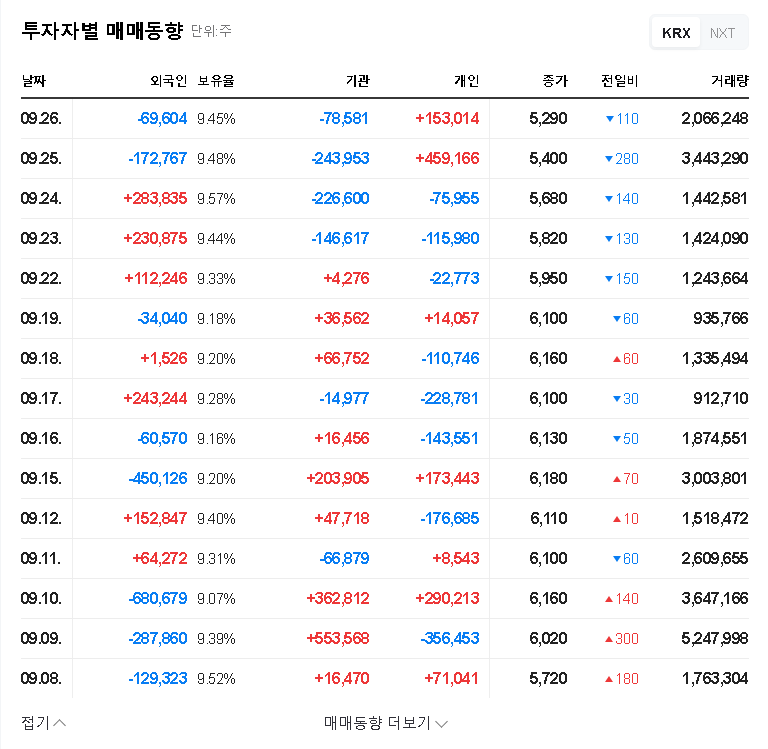

A critical point of concern is HS Hwasung’s debt-to-equity ratio, which stood at 118.3% as of H1 2025. This indicates high financial leverage. While the project win is positive, it may require additional financing, potentially straining the balance sheet. Investors should closely monitor how the company manages its debt and leverages cash flows from property sales to fund this project. For those new to these metrics, understanding key financial ratios for construction stocks is essential for a complete picture.

Strategic Implications and Competitive Edge

Beyond the financials, this contract win fortifies HS Hwasung’s strategic position in the competitive housing market.

- •Strengthened Housing Portfolio: Successfully executing the Jamwon Hanshin Town project will solidify HS Hwasung’s reputation as a reliable partner in urban renewal, a segment with consistent demand even during market downturns.

- •Proven Bidding Power: Winning this bid validates the company’s competitive edge and strategic pricing, which can be a deciding factor in securing future projects.

- •Resilience in a Slow Market: Securing a major order when competitors are struggling demonstrates operational excellence and effective crisis management, boosting investor confidence.

Investor Outlook: A Balanced View

While the news is overwhelmingly positive, a prudent investor must consider both the opportunities and the risks. The Jamwon Hanshin Town Reconstruction Project provides clear short-term momentum for HS Hwasung stock.

Positive Factors to Consider

- •Guaranteed short-term revenue pipeline.

- •Enhanced brand reputation and market position.

- •Demonstrated ability to thrive in a tough economic climate.

Potential Risks to Monitor

- •The high debt-to-equity ratio remains a significant financial concern.

- •Profitability could be squeezed by rising material costs or interest rates.

- •A prolonged construction market downturn could affect other areas of the business.

In conclusion, this contract is a significant positive signal for HS Hwasung. However, it does not erase the underlying financial leverage risks. Investors should view this as a promising development but continue to conduct thorough due diligence, focusing on the company’s efforts to improve its financial structure alongside its project execution capabilities.

Frequently Asked Questions (FAQ)

Q1: How large is the Jamwon Hanshin Town project for HS Hwasung?

A1: The project is valued at approximately ₩63.5 billion, which represents 10.4% of HS Hwasung’s recent annual revenue and about 23.8% of its H1 2025 revenue, making it a highly significant contract.

Q2: What are the main financial benefits of this new contract?

A2: The primary benefits are a direct and substantial boost to future revenue and the potential for improved profitability, as smaller-scale urban projects can offer better margins and require less initial capital than massive developments.

Q3: Why is HS Hwasung’s high debt ratio a concern?

A3: With a debt-to-equity ratio of 118.3%, the company is already highly leveraged. Taking on a new project, even a profitable one, could require more borrowing, increasing financial risk and interest expenses. Investors should watch for improvements in this area.

Q4: What does this win say about HS Hwasung’s market position?

A4: Securing this project during a market slowdown highlights the company’s strong competitive positioning, effective strategy, and resilience. It proves that HS Hwasung can win valuable contracts even when the overall industry faces headwinds.