Techwing Co., Ltd., a key player in the semiconductor inspection equipment sector, has made a decisive financial move that has the market buzzing. The company’s recent announcement of a significant Techwing treasury stock disposition to fund its expansion into High Bandwidth Memory (HBM) equipment is a classic high-stakes gambit. On one hand, it promises to unlock immense growth in the AI-driven HBM market; on the other, it raises valid stock dilution concerns for existing shareholders. This analysis will dissect the decision, its strategic rationale, and the potential outcomes for investors.

The Announcement Deconstructed: ₩93.3 Billion at Play

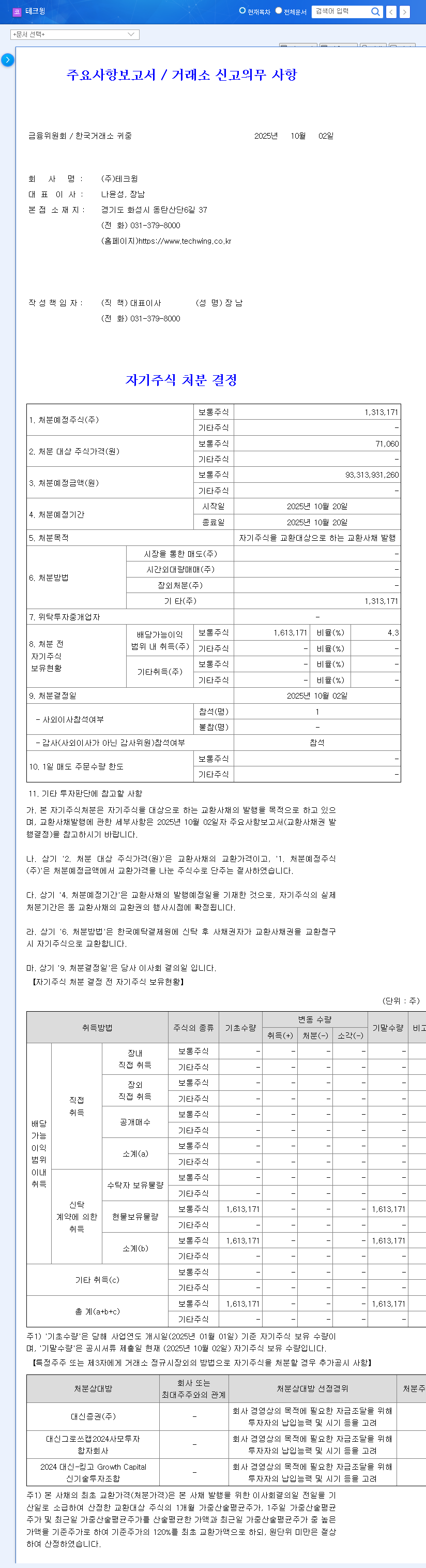

On October 2, 2025, Techwing’s board of directors greenlit the disposition of 1,313,171 shares of its treasury stock, valued at approximately 93.3 billion KRW. The mechanism for this capital raise is the issuance of exchangeable bonds (EB). This isn’t just a routine financial adjustment; it’s a clear signal of the company’s aggressive strategy to secure a leadership position in a next-generation technology segment. The full details of this strategic move were filed and are available for public review in the Official Disclosure (DART report).

Why Now? The Strategy Behind the Exchangeable Bonds

Choosing to issue exchangeable bonds is a calculated move. EBs are a hybrid financial instrument that acts like a bond, paying interest, but also gives the holder the right to exchange it for a set number of the company’s treasury shares at a later date. This allows Techwing to raise a substantial amount of capital at a potentially lower interest rate than a traditional loan, making it an attractive option for funding ambitious projects.

Fueling the Future: Techwing HBM Investment

The primary motivation for this capital injection is clear: to dominate the emerging market for HBM inspection equipment. HBM is a critical component in the AI and high-performance computing revolution, stacking memory chips vertically to deliver unprecedented speed and efficiency. Techwing’s new ‘Cube Prober’ is designed specifically for this market, and the funds will be essential for R&D, scaling up mass production, and solidifying its market entry. As a technology, HBM is foundational to modern AI infrastructure, a fact detailed by industry leaders like NVIDIA on their tech blog.

A Look at Financial Health

While the growth story is compelling, a look at Techwing’s financials reveals a more nuanced picture. The first half of 2025 showed a welcome return to profitability. However, the balance sheet also indicates rising liabilities and a high total debt ratio, suggesting that careful financial management is paramount. The issuance of EBs will add to this debt burden, making the successful and timely launch of the HBM equipment line even more critical to justify the added financial risk.

Techwing is at a crossroads, balancing the immediate financial pressure of increased debt and potential share dilution against the transformative potential of becoming a leader in the HBM semiconductor equipment market.

The Investor’s Dilemma: Weighing Growth vs. Risk

For current and prospective investors, the Techwing treasury stock sale creates a complex scenario with clear potential upsides and significant risks that must be carefully considered.

Potential Positives: The Growth Engine

- •Capital for Innovation: The ₩93.3B provides the necessary firepower to accelerate the development and deployment of new, high-margin HBM products.

- •Market Leadership: A successful HBM equipment launch could significantly increase corporate value and establish Techwing as a critical supplier in the AI hardware chain.

- •Cost-Effective Funding: Using EBs allows the company to secure these funds at a lower cost than other financing methods, preserving more capital for operations.

Potential Negatives & Considerations

- •Shareholder Dilution: This is the primary concern. If and when bondholders convert their EBs into stock, the total number of shares outstanding increases, potentially diluting the ownership stake and reducing the earnings per share (EPS) for existing shareholders.

- •Increased Debt Load: The bonds add to the company’s liabilities, increasing its financial risk profile until the investment in HBM equipment begins to generate significant returns.

- •Execution Risk: The entire strategy hinges on the successful market adoption of the ‘Cube Prober’. Any delays or technical setbacks could strain the company’s finances without the expected revenue to offset the new debt.

Investment Outlook and Strategic Monitoring

Given the balance of factors, the investment outlook remains neutral but cautiously optimistic, pending execution. Investors should adopt a strategy of diligent monitoring. For those interested in this sector, understanding the broader landscape is key, and you may find value in Our Guide to Semiconductor Stock Analysis. Focus on tracking the progress of the Techwing HBM investment, any announcements regarding the ‘Cube Prober’s’ adoption by major clients, and the company’s quarterly reports for signs of debt reduction and improving cash flow.

Ultimately, Techwing’s decision to leverage its treasury stock is a bold bet on its own technological future. Success could redefine its market position and deliver substantial long-term value, but the path is laden with financial risks that demand respect and close observation.