The latest financial report from SEBANG GLOBAL BATTERY CO., LTD has sent a ripple of concern through the investment community, raising critical questions about the future of SEBANG GLOBAL BATTERY stock. A significant 2025 Q3 ‘earnings shock’ saw key metrics fall drastically short of market consensus, prompting an urgent re-evaluation of the company’s trajectory and investment viability. This comprehensive analysis will dissect the official figures, explore the root causes of the underperformance, and provide a clear, data-driven investment strategy for navigating the uncertainty ahead.

The Q3 2025 Earnings Shock: A Numbers Deep Dive

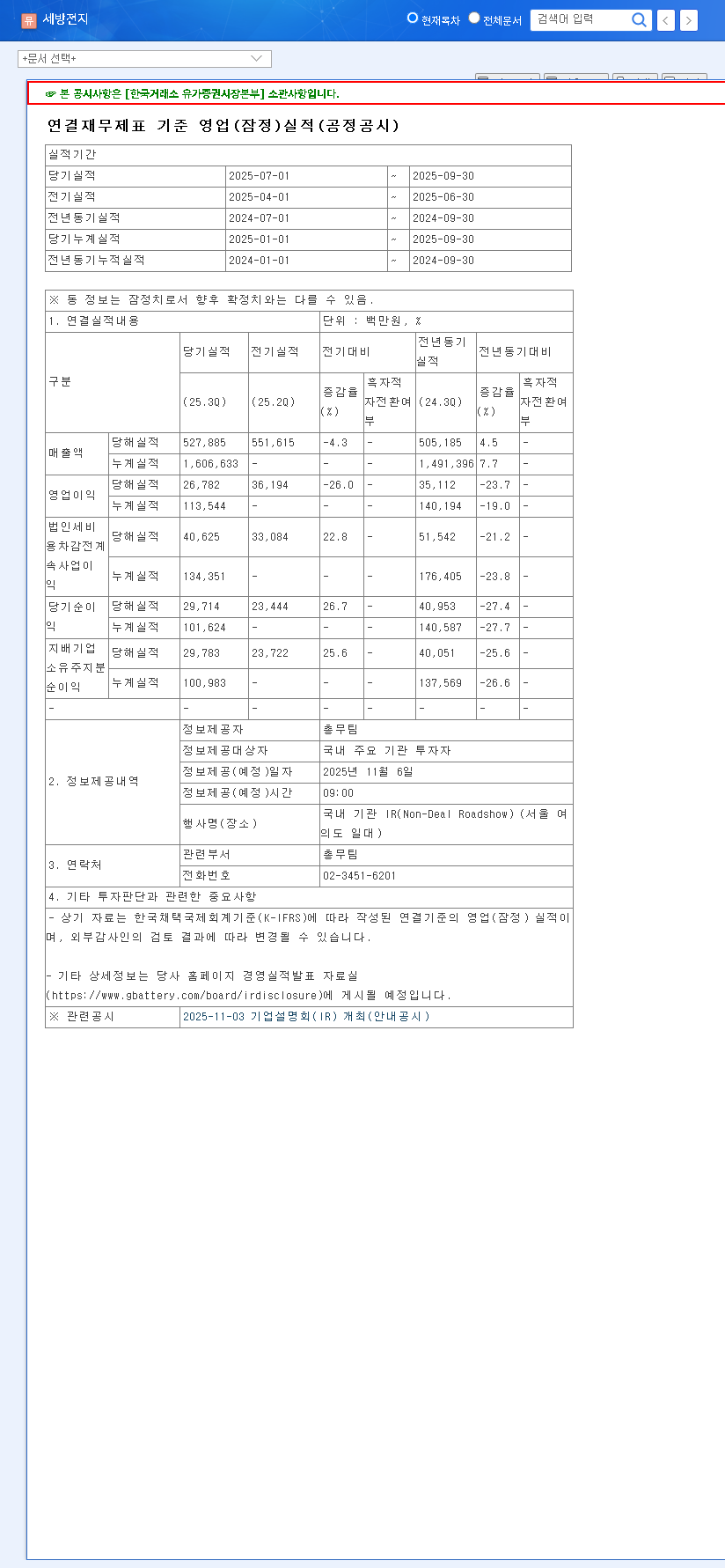

On November 5, 2025, SEBANG GLOBAL BATTERY released its provisional Q3 results, which immediately triggered alarms. The variance between the reported figures and market expectations was substantial, particularly in profitability. The core numbers from the SEBANG GLOBAL BATTERY earnings report paint a stark picture:

- •Revenue: Reported at KRW 527.9 billion, a significant 9.0% below the market’s expectation of KRW 578.4 billion.

- •Operating Profit: Came in at just KRW 26.8 billion, a staggering 36.9% miss compared to the anticipated KRW 42.5 billion.

- •Net Profit: Stood at KRW 29.8 billion.

The nearly 37% plunge in operating profit relative to expectations is the primary driver of market concern. This level of deviation suggests that underlying operational or market challenges are more severe than previously understood, eroding investor confidence in the SEBANG GLOBAL BATTERY stock. For full transparency, these figures are based on the company’s report, which can be viewed in the Official Disclosure filed with DART.

The magnitude of the operating profit miss indicates a fundamental issue with cost control and margin management, a recurring theme that now demands immediate attention from leadership.

Analyzing the Underperformance: What Went Wrong?

This isn’t an isolated incident but rather the culmination of a worrying trend. A deeper SEBANG GLOBAL BATTERY analysis reveals decelerating growth and systemic profitability weaknesses that have been building over several quarters.

Persistent Profitability Pressures

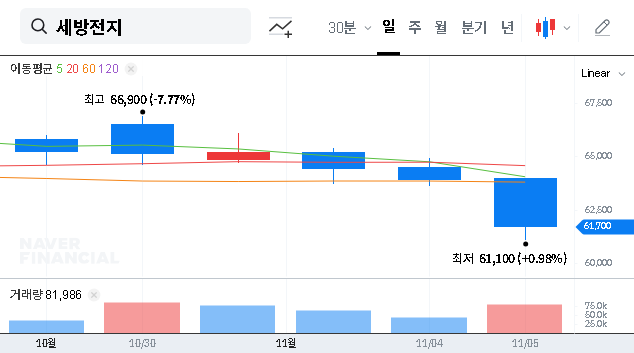

Operating profit has been in a steady decline since its peak in Q1 2025, with Q3 marking a four-quarter low. While year-on-year revenue saw a modest 4.5% increase, the overall growth trajectory is slowing. The primary culprits identified in earlier reports—including adverse US tariffs, volatile exchange rates, and temporary cost hikes—appear to have intensified. The sharp decline in profitability, even as raw material prices like lead have fallen, points to a structural inability to manage costs effectively. This is a significant red flag for any potential SEBANG GLOBAL BATTERY investment.

The EV Battery Question Mark

The company’s Electric Vehicle (EV) battery division, which accounts for 15% of revenue, has been touted as a key growth engine. However, it’s now unclear whether this segment is failing to meet sales targets or if its expansion is coming at the expense of margins. To learn more, you can read our full analysis of the global EV battery market. Without clarity from management, investors are left to speculate whether the core business is deteriorating or if the high-growth venture is draining resources. Both scenarios are deeply concerning for the valuation of SEBANG GLOBAL BATTERY stock.

Stock Outlook and Investment Strategy

Given the severity of the Q3 performance, investors must adopt a cautious and strategic approach. The short-term and long-term outlooks present different challenges and potential pathways.

Short-Term: ‘Sell’ Recommendation

In the immediate term, the earnings shock is expected to severely weaken investor sentiment, placing significant downward pressure on the stock price. The lack of a clear explanation or a credible turnaround plan from management exacerbates this risk. Therefore, our current investment opinion is a ‘Sell’. The downside risk is high until the company provides a transparent analysis of the Q3 failures and outlines concrete steps for cost efficiency and margin improvement. Without this, the stock is likely to underperform, according to broader market sentiment analysis.

Mid-to-Long Term: A Cautious Path to Recovery

Recovery is possible but not guaranteed. The long-term health of SEBANG GLOBAL BATTERY stock hinges on two factors: stabilizing the profitability of its core business and successfully scaling its EV battery division. The competitive landscape for accumulators demands relentless innovation and cost competitiveness. Investors should watch for key indicators of a turnaround, such as:

- •A detailed and credible management plan for cost reduction.

- •Visible margin improvement in the upcoming Q4 2025 and Q1 2026 reports.

- •Clear performance metrics and growth in the EV battery segment.

Until these signs emerge, a defensive stance is the most prudent course of action. Investors should prepare for continued volatility and prioritize capital preservation.