Investors in SCM Lifescience (KOSDAQ: 298060), a pioneering biotech company, are closely monitoring recent developments after a significant change in its ownership structure. The disclosure that former CEO Song Ki-ryung has reduced his stake has sent ripples through the market, raising critical questions about the company’s stability and future trajectory. This comprehensive SCM Lifescience analysis will dissect the implications of this event, evaluate the company’s core stem cell technology, scrutinize its financial health, and provide a clear outlook for investors considering the 298060 stock.

The Catalyst: A Major Shareholding Shift

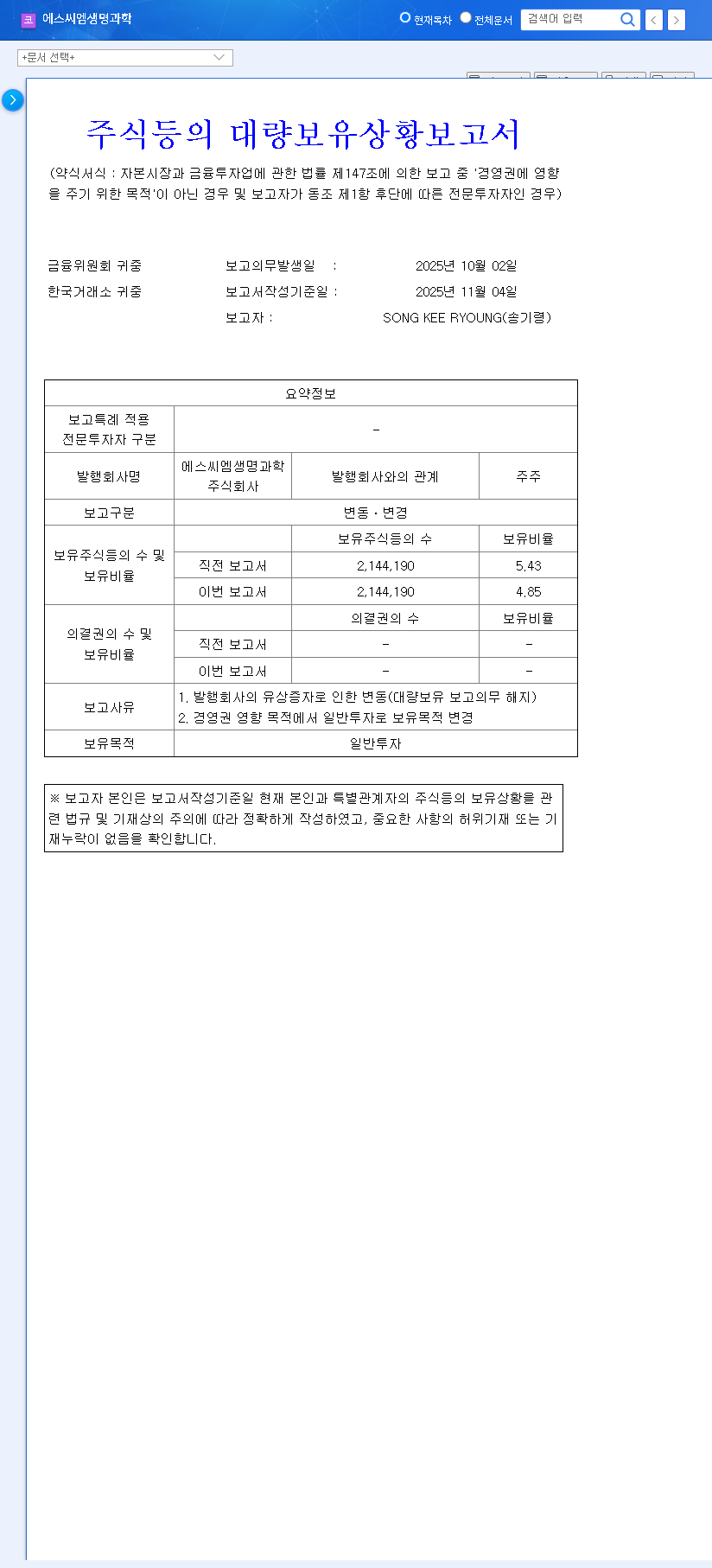

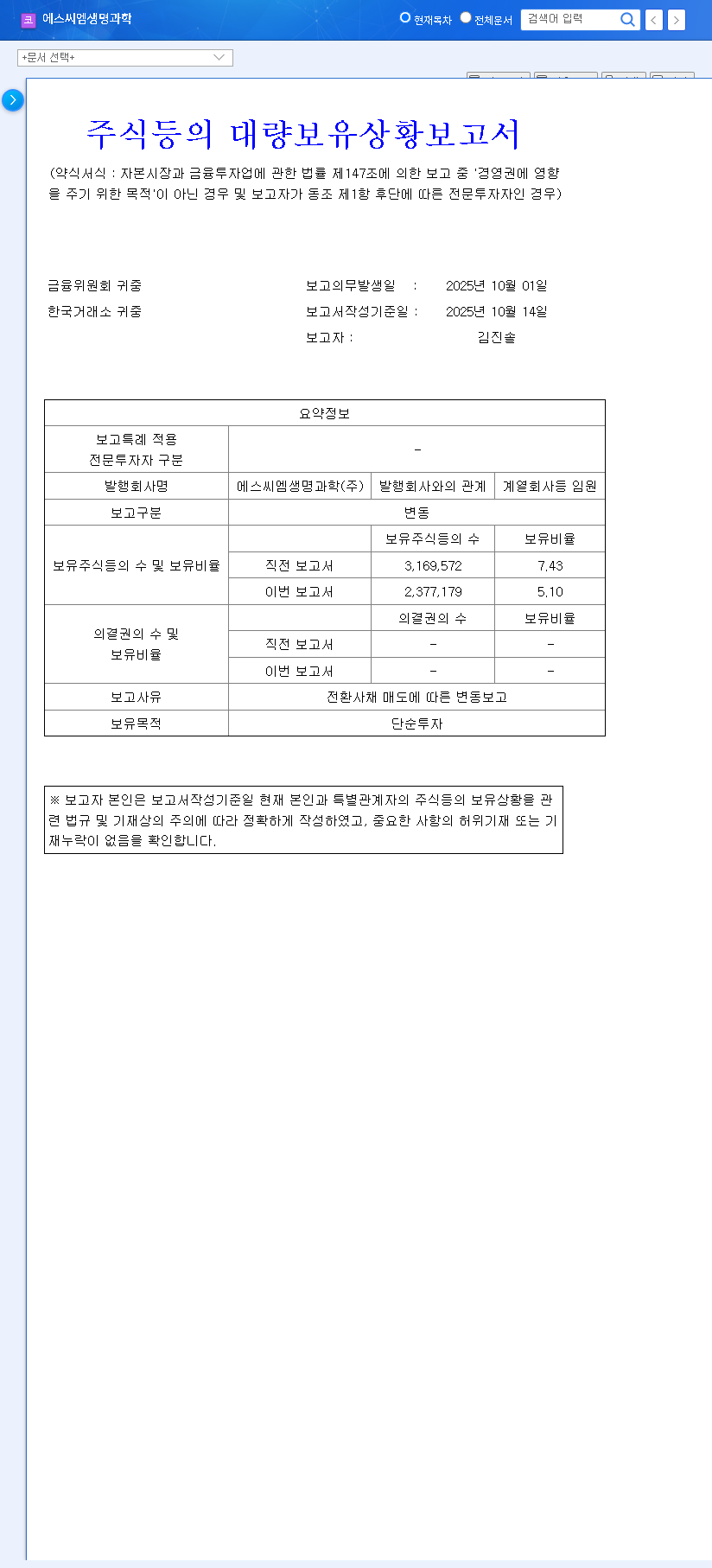

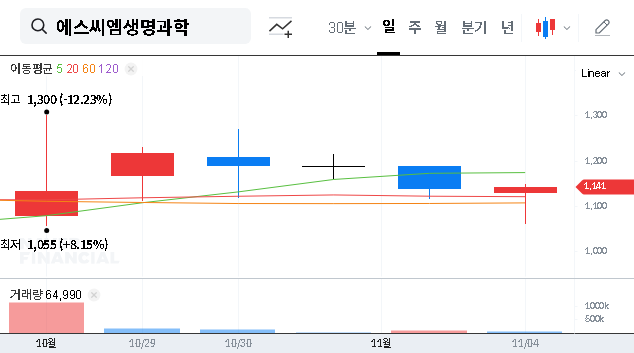

On November 4, 2025, SCM Lifescience formally announced a notable change in its shareholder registry. Former CEO Song Ki-ryung’s ownership stake decreased from 5.43% to 4.85%. More significantly, the stated purpose of his shareholding shifted from ‘management influence’ to ‘general investment purposes’. This change, detailed in the Official Disclosure on DART, signals a pivotal transition for the company’s leadership dynamics.

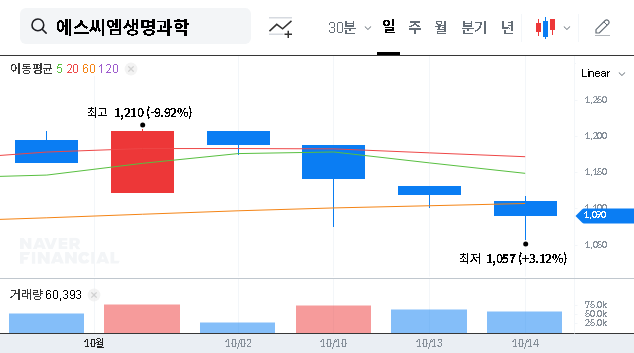

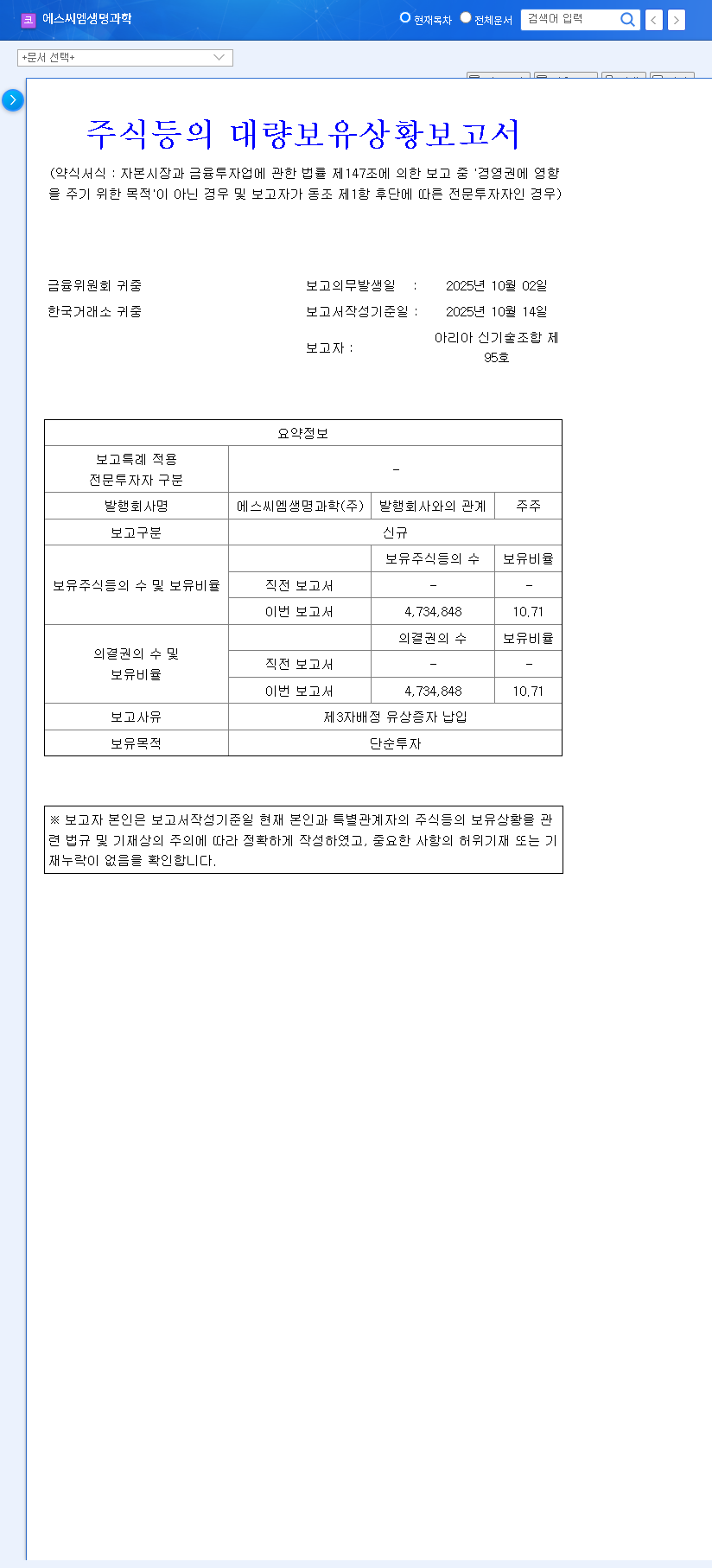

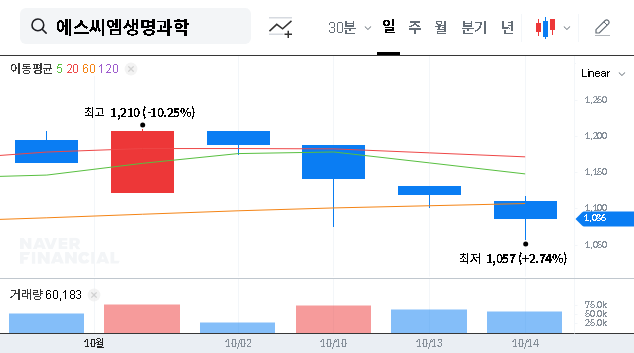

This reduction is primarily attributed to share dilution following a recent rights offering. However, the change in intent is the key takeaway. It suggests the former CEO is stepping back from direct involvement in corporate governance, positioning himself as a passive investor. For the new management team that took the helm in March 2025, this could mean more autonomy. For the market, it introduces a layer of uncertainty and potential for short-term stock volatility.

The shift from ‘management influence’ to ‘general investment’ is a critical signal. It may grant the new leadership team operational freedom but could also lead to selling pressure on SCM Lifescience stock if the former CEO decides to liquidate further.

Core Strengths: A Deep Dive into SCM Lifescience’s Technology

At the heart of SCM Lifescience‘s long-term potential is its proprietary technology. Understanding this is key to any investment thesis. The company’s primary competitive advantage lies in its patented ‘Stratified Isolation Method’ for high-purity stem cell separation and culture. This innovative process allows for the development of potent and consistent cell-based therapies.

Key Technology and Pipelines

- •Proprietary Method: The ‘Stratified Isolation Method’ forms the foundation of its R&D, promising higher efficacy in its therapeutic candidates.

- •Orphan Drug Designation: Its treatment for chronic graft-versus-host disease (e.g., SCM-CGH) has been designated as an orphan drug, which can lead to faster regulatory review and extended market exclusivity. This is a significant de-risking factor.

- •Business Diversification: Beyond therapeutics, the company has smartly leveraged its expertise to launch ‘IROROO’, a derma-cosmetic brand. This generates early-stage revenue to help fund the capital-intensive R&D, a crucial strategy for a pre-profitability biotech firm. The potential of stem cell technology in regenerative medicine is widely recognized by leading research institutions.

Financial Health & Risk Analysis

While the technology is promising, the financial statements reveal significant challenges. As of the first half of 2025, SCM Lifescience is in a high-growth, high-risk phase. The R&D expenditure ratio stands at an aggressive 124.74% of sales, underscoring its commitment to innovation but also its cash burn rate.

Key Financial Considerations

- •Persistent Losses: The company reported an operating loss of KRW 2.413 billion in H1 2025, contributing to a large accumulated deficit of KRW -178.881 billion. Profitability remains a distant goal.

- •High Debt Load: A debt-to-equity ratio of 230.13% is a major red flag, increasing financial risk, especially in a high-interest-rate environment.

- •Capital Infusion: A recent rights offering raised KRW 16.378 billion, providing a necessary lifeline, but shareholder dilution is the cost. Future fundraising will be critical.

- •Affiliate Issues: The liquidation of its affiliate, CoImmune, could negatively impact asset values and disrupt planned business collaborations, adding another layer of operational risk.

Investor Outlook & Strategic Path Forward

For investors, SCM Lifescience stock represents a classic high-risk, high-reward biotech play. The former CEO’s shareholding change is a near-term headwind that could suppress the stock price. However, the company’s long-term value will be determined by its ability to execute on its clinical and commercial goals. For those looking to learn more about this sector, reviewing our guide to investing in biotech stocks can provide valuable context.

Key Catalysts for Future Growth:

- •Clinical Trial Success: Positive data from its key pipelines, especially SCM-CGH, is the single most important value driver.

- •Licensing & Partnerships: A successful technology transfer or licensing deal with a major pharmaceutical partner would validate its platform and provide non-dilutive funding.

- •Financial Discipline: Demonstrating effective cash management and securing a path to improved financial stability is crucial to rebuilding investor confidence.

- •Derma-Cosmetic Growth: Continued expansion and profitability of the ‘IROROO’ brand can provide a stable revenue base.

In conclusion, while the recent management and shareholder shifts create short-term noise, disciplined investors should focus on the underlying fundamentals. The success of SCM Lifescience hinges on its scientific progress and the new leadership’s ability to navigate a challenging financial landscape. Careful monitoring of clinical data, partnership news, and quarterly financials is essential before making any investment decisions.