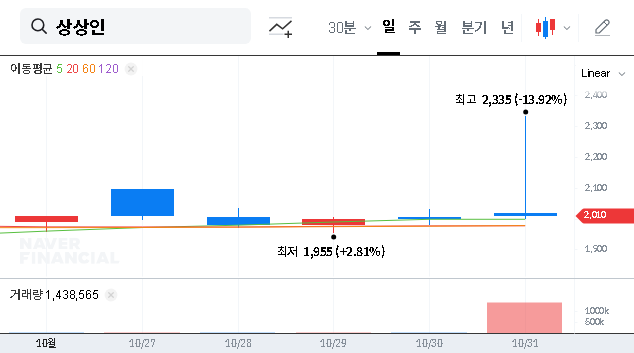

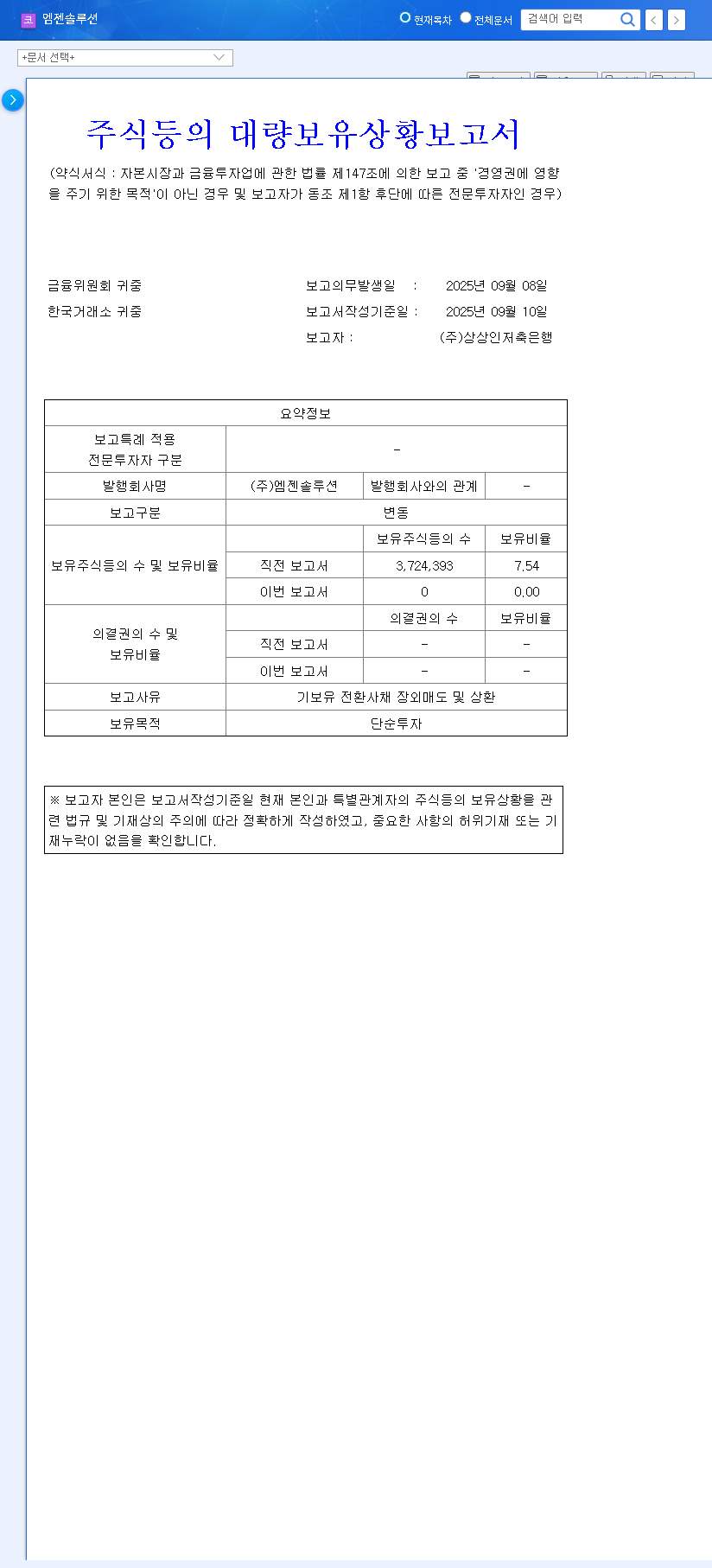

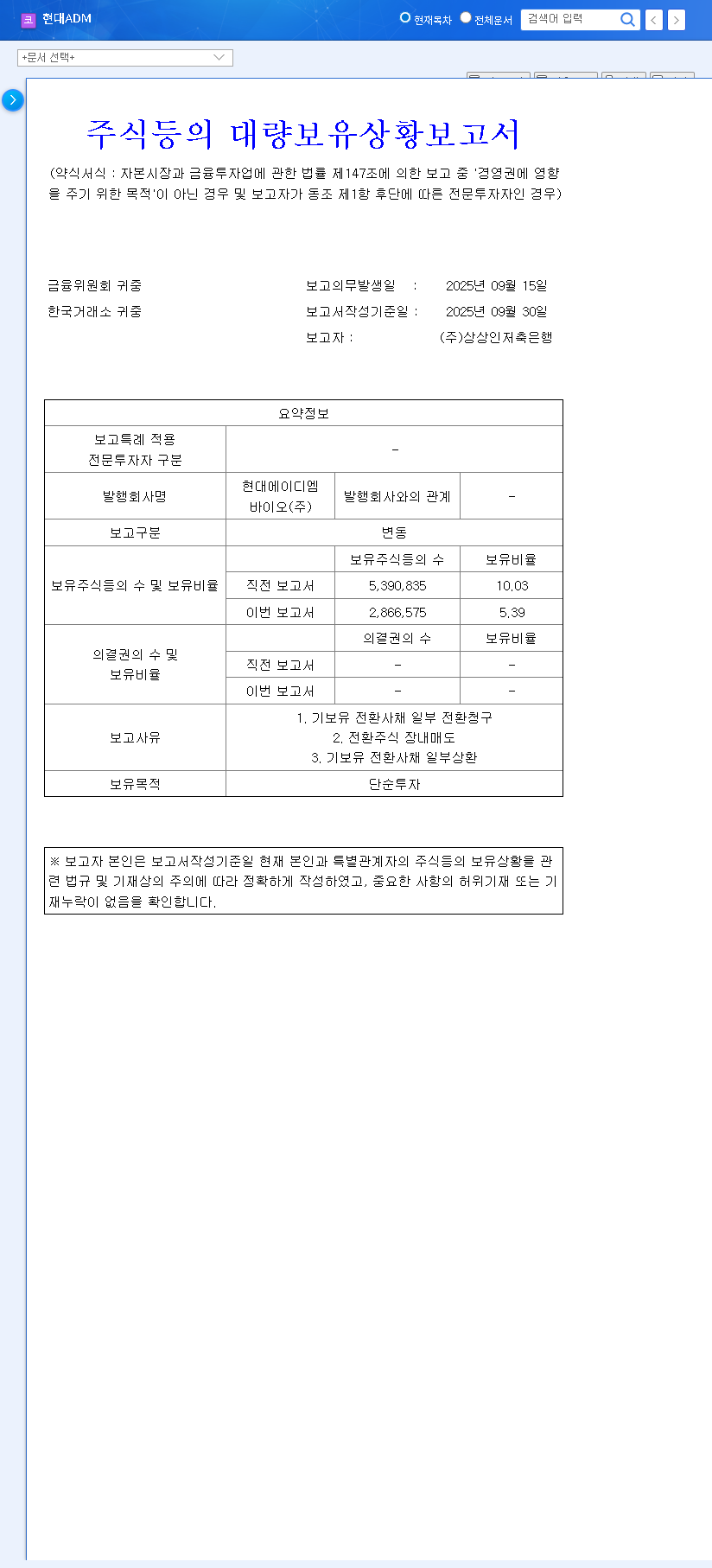

The recent disclosure surrounding a major investment in Jayjun Cosmetic (025620) convertible bonds has sent ripples through the market. Sangsangin Savings Bank, a notable financial institution, has acquired a significant 5.05% stake through this strategic move, sparking intense debate among investors. For a company like Jayjun Cosmetic, which has been navigating a period of fundamental instability, this capital injection could be a pivotal turning point—or a new layer of complexity. This analysis delves deep into the implications of this event, dissecting the financial, strategic, and governance impacts to provide a clear roadmap for investors.

This investment by Sangsangin Savings Bank presents a critical juncture for Jayjun Cosmetic, introducing both a lifeline for financial restructuring and the potential for increased shareholder uncertainty. Understanding the nuances is key.

The Core Event: A 5.05% Stake Acquired

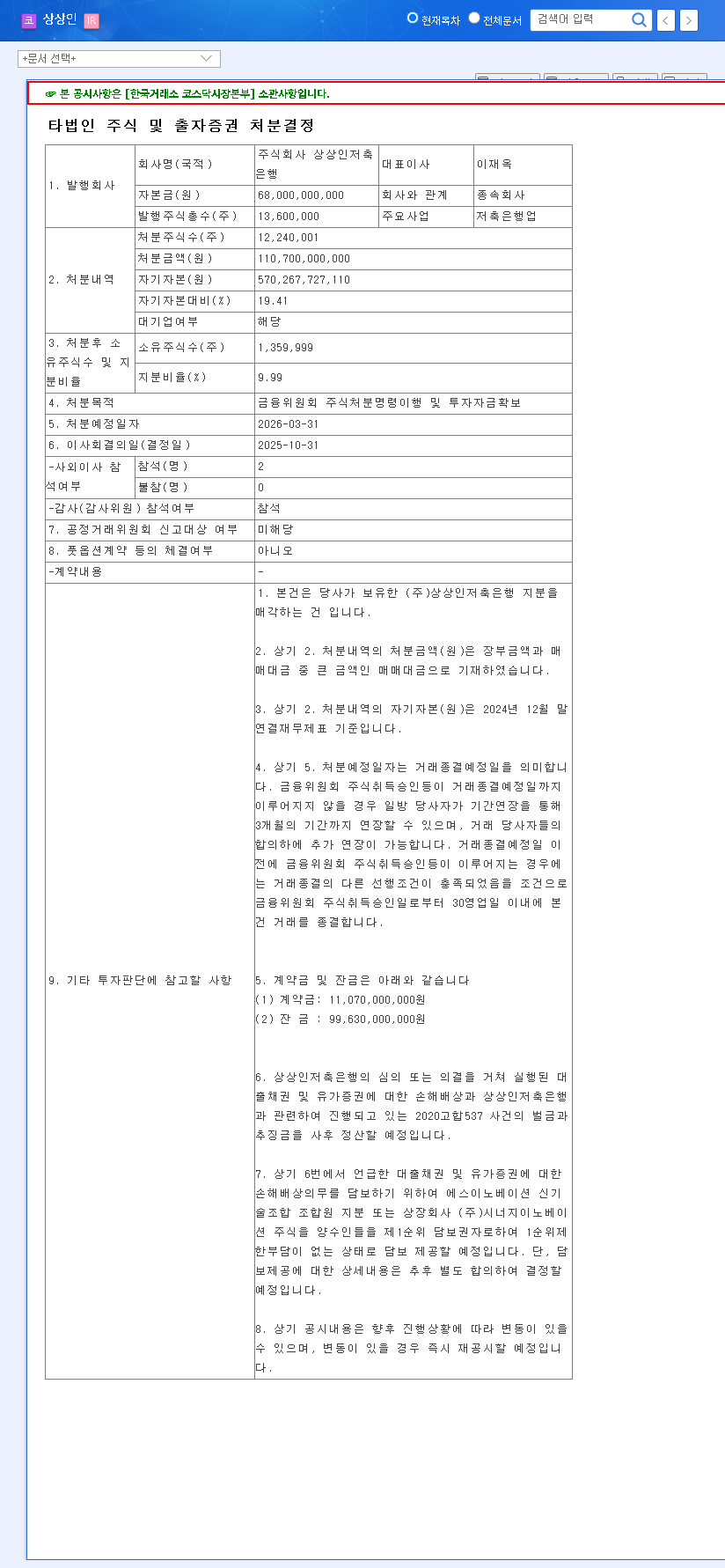

On November 4, 2024, Sangsangin Savings Bank officially reported its new large shareholding in Jayjun Cosmetic Co., Ltd. The acquisition, made through convertible bonds (CBs), was declared for ‘simple investment purposes’, as detailed in the Official Disclosure (DART). Crossing the 5% ownership threshold triggered the mandatory disclosure, bringing this significant financial maneuver into the public eye and raising questions about the bank’s long-term intentions and the future of Jayjun Cosmetic.

Why Convertible Bonds? A Strategic Choice

The choice of convertible bonds is particularly insightful. For Jayjun Cosmetic, it’s a flexible way to raise capital at potentially lower interest rates than traditional loans, without immediately diluting existing shareholder equity. For Sangsangin Savings Bank, it offers a hybrid investment vehicle: they receive interest payments like a bondholder but retain the upside potential to convert the bonds into stock if Jayjun’s share price appreciates. This structure provides a degree of security while preserving the opportunity for significant returns, a strategy often employed in volatile markets. To learn more, you can read our guide on Understanding Convertible Bonds for Retail Investors.

Comprehensive Analysis: Impact on Jayjun Cosmetic (025620)

This investment cannot be viewed in isolation. Its true impact must be assessed across Jayjun’s financial health, business strategy, and governance structure, especially considering the company’s recent challenges in the competitive cosmetics sector.

1. Financial Structure and Performance

The infusion of capital via the Jayjun Cosmetic (025620) convertible bonds brings both potential benefits and risks.

- •Positive Outlook: Conversion of the bonds into equity would decrease the company’s debt-to-equity ratio, strengthening its balance sheet. This improved financial stability could attract further investment and provide the necessary capital to fund new growth initiatives.

- •Potential Drawbacks: Until conversion, Jayjun must service the interest on these bonds, potentially increasing its financial expenses. Furthermore, the overhang of potential conversion can create uncertainty. The conversion price will be a key metric to watch, as a low price could lead to significant dilution for existing shareholders upon exercise.

2. Business Strategy and Growth Outlook

Jayjun has been attempting to diversify beyond its core, yet sluggish, cosmetics business into healthcare and financial investments. This move by a savings bank could act as a catalyst.

- •Opportunity for Synergy: Sangsangin’s financial expertise could provide valuable guidance or even partnership opportunities as Jayjun explores new ventures. The investment validates these diversification efforts to some extent, signaling market confidence.

- •Pressure to Perform: With a sophisticated financial institution now on its cap table, management will face heightened pressure to deliver tangible results from both its core business and new ventures. The market will demand a clearer, more executable strategy.

3. Shareholder Value and Corporate Governance

Existing shareholders of the 025620 stock are right to be concerned about share dilution. If all the bonds are converted, the total number of outstanding shares will increase, which could dilute the earnings per share (EPS) and the ownership percentage of current investors. However, the presence of an institutional investor can also enhance corporate governance, as they provide a new layer of oversight on management decisions, potentially leading to increased transparency and better long-term strategy.

Investor Checklist & Final Verdict

While this development introduces an opportunity for revitalization, a cautious and watchful approach is paramount. The investment in Jayjun Cosmetic (025620) convertible bonds is not a guaranteed signal of a turnaround. Investors should monitor the following key areas before making any decisions:

- •Sangsangin’s Future Actions: Monitor any further disclosures from the bank regarding their intentions. Will they convert, sell, or hold the bonds to maturity?

- •New Business Milestones: Track concrete progress in Jayjun’s healthcare and financial investment ventures. Announcements of partnerships or revenue generation will be critical signals.

- •Core Business Revival: Look for signs of improvement in the cosmetics division’s sales and profitability in upcoming quarterly reports.

- •Macroeconomic Factors: Keep an eye on interest rate trends from central banks like the U.S. Federal Reserve, as this influences corporate financing costs and overall market sentiment.

In conclusion, Sangsangin Savings Bank’s investment is a double-edged sword. It provides Jayjun with much-needed capital and a strategic partner, but it also introduces complexities like potential share dilution and heightened performance expectations. A wait-and-see approach, grounded in diligent monitoring of the factors above, is the most prudent strategy for now.