A Strategic Pivot: Unpacking the SAMYOUNG M-TEK DongAh Hwasung Acquisition

In a significant move poised to reshape its future, SAMYOUNG M-TEK Co., Ltd. (054540) has announced a landmark deal that signals a bold new chapter. The company is set to acquire a major stake in DongAh Hwasung, a leader in industrial special rubber components. This initial analysis will explore the core details of the SAMYOUNG M-TEK DongAh Hwasung acquisition, dissecting the strategic rationale, financial implications, and providing a comprehensive outlook for current and potential investors. This isn’t just a purchase; it’s a strategic diversification designed to build long-term resilience and unlock new growth avenues.

The Core Details of the Landmark Deal

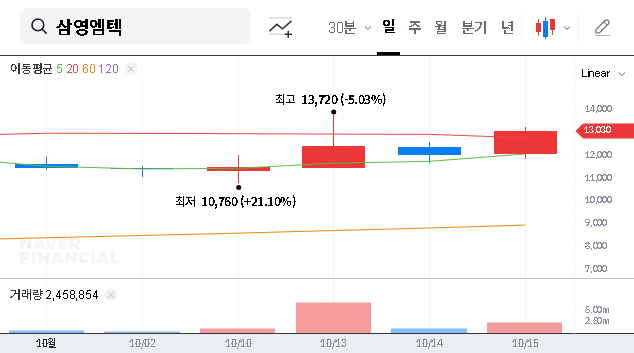

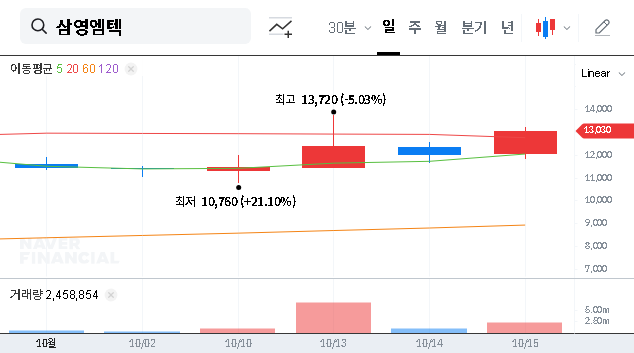

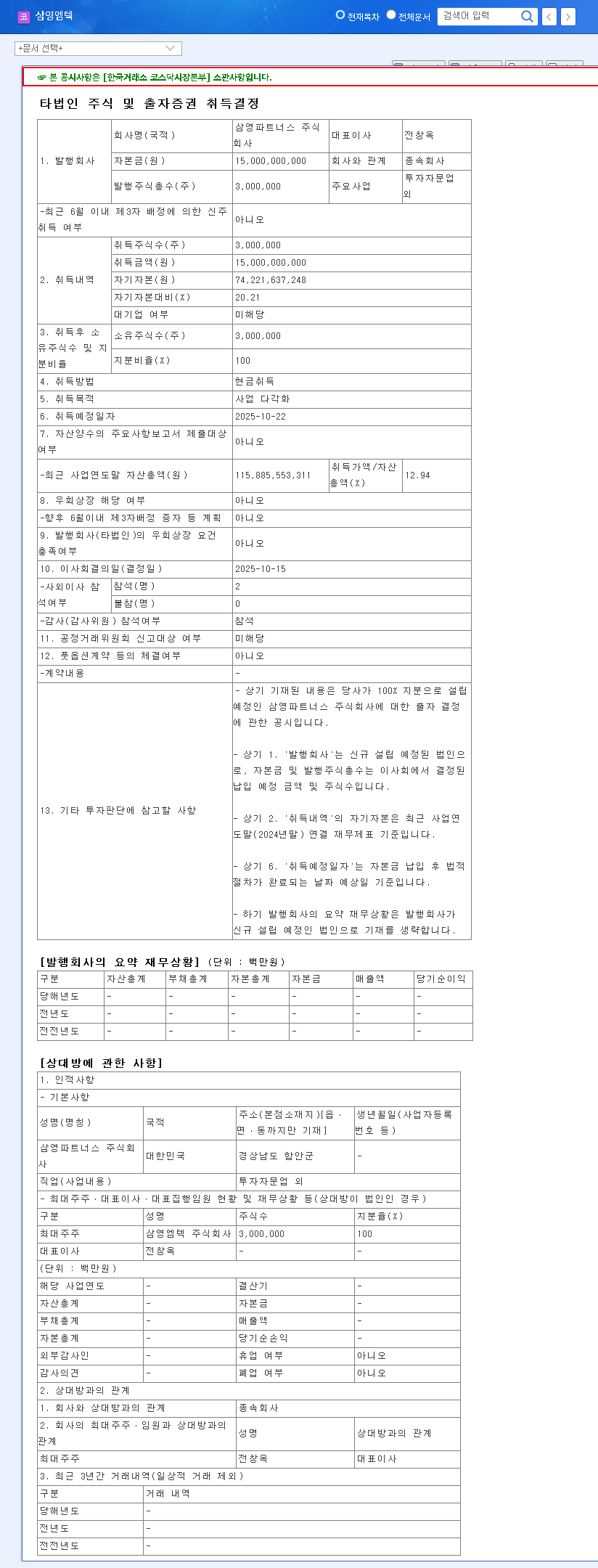

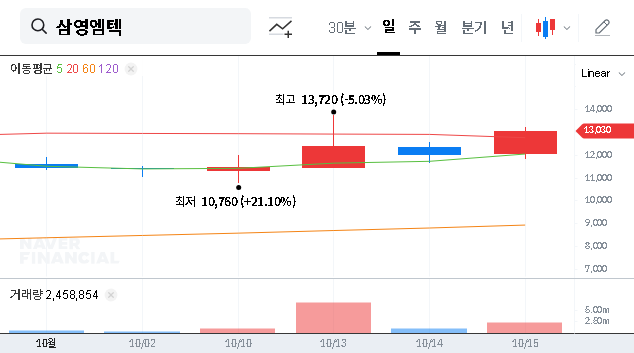

On October 28, 2025, SAMYOUNG M-TEK confirmed that its subsidiary, Samyoung Partners, will acquire a 42.18% stake in DongAh Hwasung for a total of ₩133.3 billion. The transaction is scheduled to be finalized by December 16, 2025. DongAh Hwasung specializes in manufacturing high-performance rubber components essential for various sectors, including automotive, electronics, and home appliances. This move injects a completely new business vertical into SAMYOUNG M-TEK’s portfolio, which has traditionally focused on plant equipment and wind power components. For a complete overview of the official filing, you can view the Official Disclosure on DART.

This acquisition represents one of the most significant strategic shifts for SAMYOUNG M-TEK in the last decade, aiming to create a more balanced and robust business structure capable of weathering industry-specific downturns.

Strategic Rationale: Why DongAh Hwasung?

Diversification Beyond Core Markets

The primary driver behind the SAMYOUNG M-TEK DongAh Hwasung acquisition is strategic business diversification. While the company’s existing divisions in plant and wind power equipment have shown stable growth, they are susceptible to cyclical trends in heavy industry and energy policy. By entering the industrial special rubber components market, SAMYOUNG M-TEK gains exposure to the vast automotive and consumer electronics sectors, reducing its reliance on a narrow set of industries and creating a more predictable revenue stream.

Unlocking Powerful Synergies

The potential for synergy is substantial. Integrating DongAh Hwasung’s technical expertise with SAMYOUNG M-TEK’s manufacturing prowess and global sales network can lead to significant value creation. Key opportunities include:

- •Cross-Industry Innovation: Applying DongAh’s rubber component technology to SAMYOUNG’s wind turbines (e.g., for vibration dampening) or plant equipment could create superior, higher-margin products.

- •Operational Efficiency: Combining procurement, R&D, and administrative functions can lead to significant cost savings across the consolidated entity.

- •Market Expansion: Leveraging SAMYOUNG’s international presence to introduce DongAh Hwasung’s products to new global markets where they currently have a limited footprint.

Comprehensive Impact Analysis for Investors

Financial Implications and Balance Sheet Health

The ₩133.3 billion cash outlay is a major investment. While SAMYOUNG M-TEK has a sound financial position, this move will undoubtedly impact its balance sheet. Investors should closely monitor how the acquisition is funded—whether through cash reserves, debt financing, or a combination. An increase in leverage could raise the company’s risk profile. The key question will be how quickly DongAh Hwasung’s profitability can be integrated to contribute positively to SAMYOUNG’s consolidated earnings per share (EPS). For more on this, you can read our guide on understanding key financial ratios in M&A deals.

Navigating Market and Macroeconomic Headwinds

The success of this acquisition will also depend on external factors. The industrial rubber market is sensitive to the health of the automotive and electronics industries. Furthermore, macroeconomic variables like currency fluctuations are critical, especially for an export-heavy company like SAMYOUNG M-TEK. A strengthening KRW could impact export competitiveness, while rising raw material costs could squeeze profit margins for DongAh Hwasung’s operations. These are ongoing risks that require diligent management.

Investor Action Plan & Future Outlook

This transformative SAMYOUNG M-TEK DongAh Hwasung acquisition presents both opportunities and risks. A well-defined investment strategy is essential.

- •Short-Term (3-6 Months): Expect heightened stock price volatility as the market digests the news. It is prudent to wait for more clarity on the integration plan and Q1 post-acquisition financials before making significant new investments. Watch for management commentary on synergy targets.

- •Mid-to-Long-Term (1-3 Years): The key performance indicator will be the successful integration of DongAh Hwasung. Monitor consolidated revenue growth, margin improvements, and debt reduction. If the diversification strategy pays off and synergies are realized, the acquisition could mark the beginning of a sustained growth period, presenting a strong long-term investment case.

In conclusion, SAMYOUNG M-TEK’s acquisition of DongAh Hwasung is a calculated, strategic gamble to build a more diversified and resilient enterprise. While financial risks and integration challenges are real, the long-term potential for growth and synergy is compelling. Careful monitoring of post-acquisition performance will be paramount for investors looking to capitalize on this new direction.