The recent announcement regarding the Samyang Packaging stock retirement has sent ripples through the investment community. This strategic move to retire a significant number of its own shares raises critical questions for current and potential investors: Is this a genuine signal of strength and a commitment to boosting shareholder value, or a temporary measure to mask underlying performance issues? This comprehensive analysis will dissect the decision, evaluate the company’s fundamentals, and provide a clear investment outlook.

For those looking for a clear strategy for Samyang Packaging stock in a volatile market, this report provides the essential data and insights needed to make an informed decision.

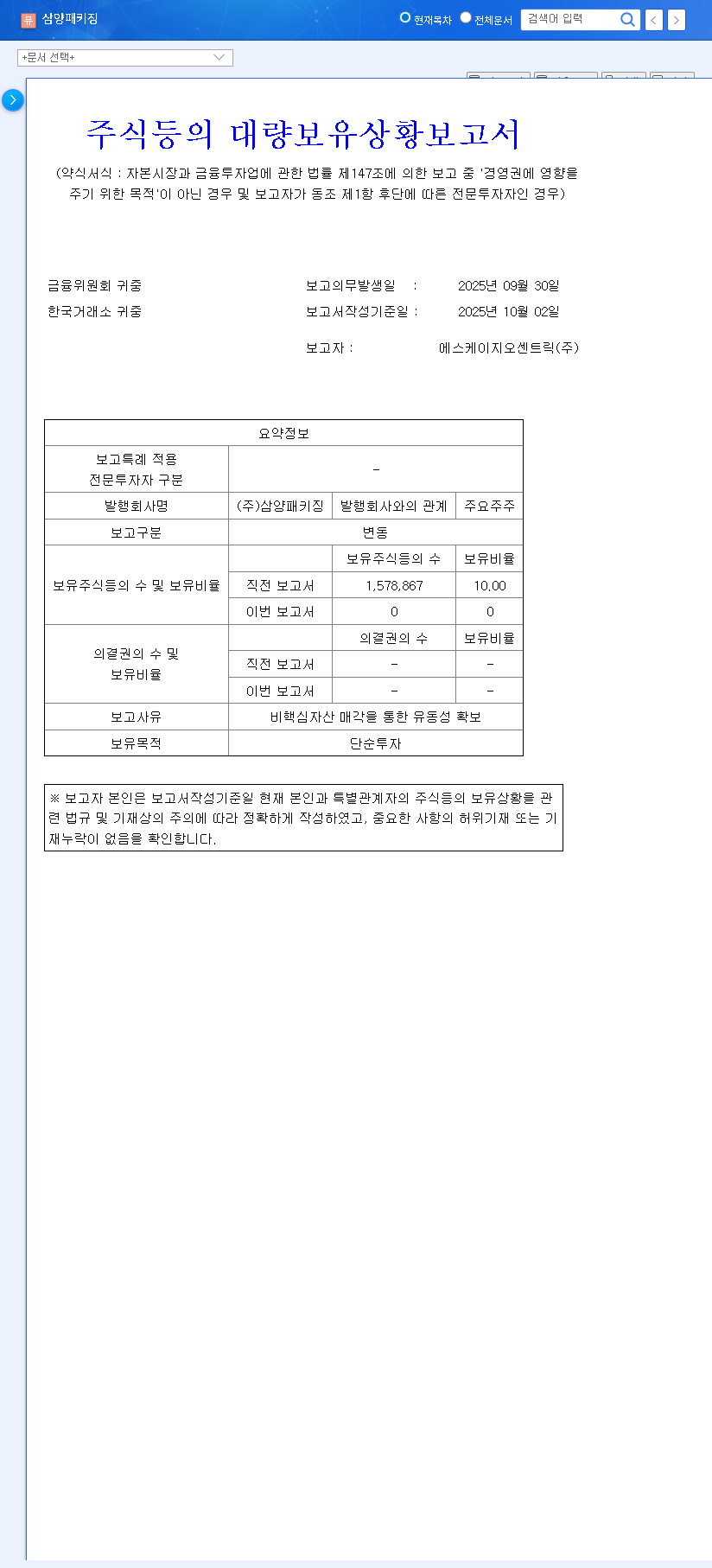

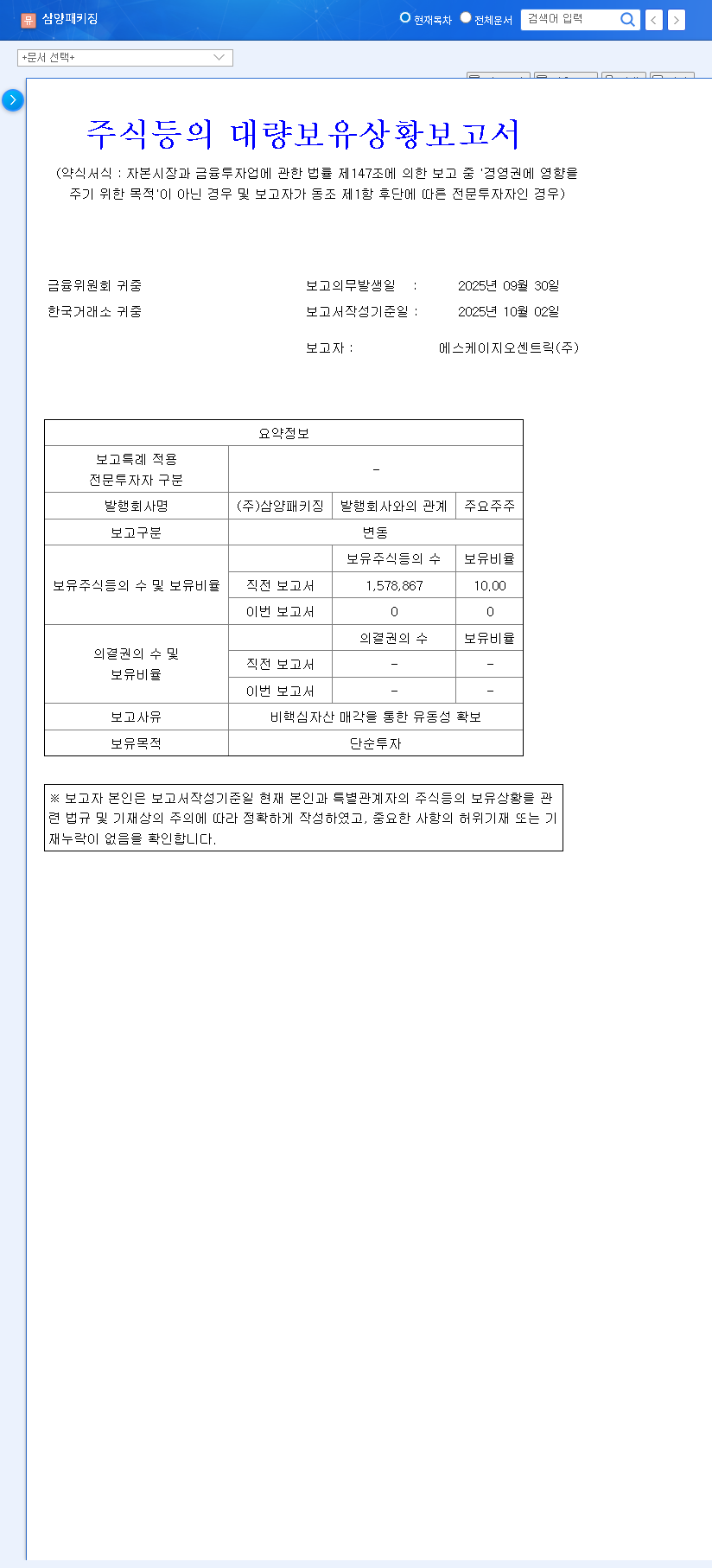

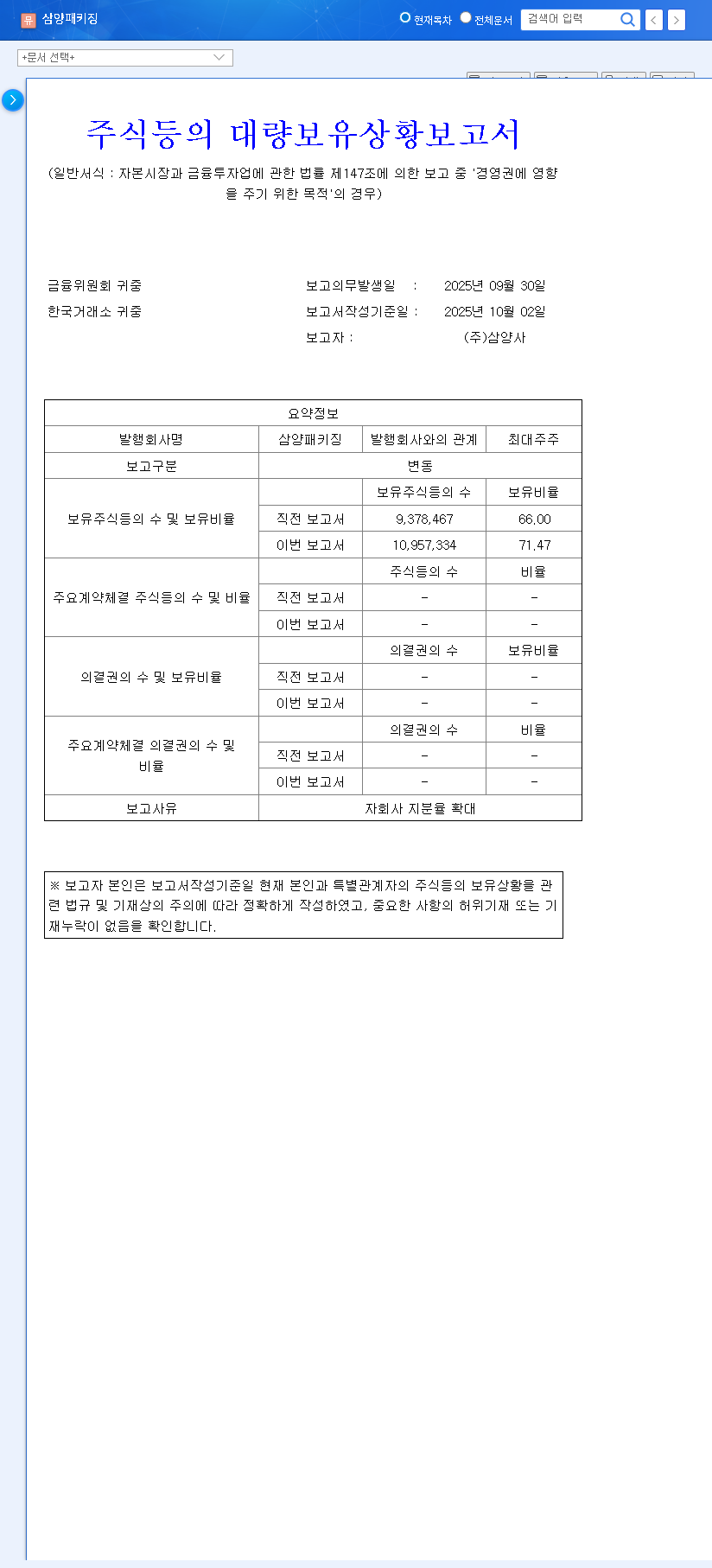

The Announcement: Key Details of the Stock Retirement

Samyang Packaging Corporation has officially declared its intention to retire treasury shares as a direct measure to enhance shareholder value. This is a definitive action where the company permanently cancels shares it has previously repurchased from the open market. Here are the crucial details from the company’s Official Disclosure.

- •Shares to be Retired: 262,565 shares of common stock.

- •Estimated Value: Approximately 3.8 billion KRW.

- •Market Cap Impact: Represents 1.79% of the company’s total market capitalization.

- •Acquisition Method: Utilizes previously acquired treasury shares.

- •Scheduled Retirement Date: November 26, 2025.

Analyzing the ‘Why’: Fundamentals and Business Health

This stock retirement initiative appears to be a strategic response to a period of sluggish financial performance. By executing a shareholder-friendly policy, the company aims to bolster investor confidence. A look at the recent half-year report reveals a trend of declining profitability, primarily driven by underperformance in specific business segments and rising operational costs.

While the core PET container and aseptic beverage businesses remain market leaders in Korea, challenges in the PET-Flake and PET-Chip segments have created significant headwinds for overall profitability.

Key Financial Headwinds

- •Revenue Contraction: Half-year revenue saw a 7.7% year-over-year decrease to 212.1 billion KRW.

- •Operating Profit Decline: A more significant 43.2% drop in operating profit to 12.4 billion KRW, largely due to increased selling, general, and administrative (SG&A) expenses.

- •Segment Disparity: The PET-Flake and PET-Chip businesses experienced declining operating rates, which directly impacted the bottom line despite the stability of the core segments.

Impact of the Samyang Packaging Stock Retirement

A stock retirement of this nature is designed to directly benefit shareholders by increasing the value of the remaining shares. The primary mechanism for this is an improvement in key financial metrics.

The Bull Case: A Boost for Shareholder Value

Reducing the number of shares in circulation directly boosts Earnings Per Share (EPS), a critical metric used in stock valuation. A higher EPS can make the stock appear more attractive, potentially leading to a higher price-to-earnings (P/E) ratio. Furthermore, this action is a clear signal from management that they believe the stock is undervalued and are committed to returning capital to shareholders, which can significantly improve market sentiment.

The Bear Case: Fundamentals Still Matter

While mathematically positive, the 1.79% retirement is moderate. Its positive effects could be overshadowed if the company’s fundamental profitability continues to decline. The market may view this as a financial maneuver rather than a sign of a true operational turnaround. Ultimately, sustained stock price appreciation will depend on improved revenue and profit margins, particularly in the struggling PET-Flake and PET-Chip divisions.

Strategic Investment Thesis & Outlook

The Samyang Packaging stock retirement is a clear positive for investors, but it must be viewed within the broader context of the company’s operational health.

Short-Term Strategy (3-6 Months)

In the short term, a bump in investor sentiment may provide some upward price momentum. However, a conservative approach is recommended. Investors should watch for stabilization in quarterly earnings and signs that the company is getting SG&A costs under control before committing significant new capital.

Long-Term Strategy (12+ Months)

The long-term success of Samyang Packaging hinges on three factors: the continued dominance of its core PET container business, a successful turnaround in its recycling and raw materials segments (explore more on the PET recycling market), and the tangible results of its ESG initiatives. The company’s focus on sustainable growth through its Samyang Ecotech subsidiary and efforts to develop recycled PET containers could become a major value driver as global demand for green packaging solutions increases.

Frequently Asked Questions (FAQ)

What is the main goal of the Samyang Packaging stock retirement?

The primary goal is to increase shareholder value. By reducing the number of outstanding shares, the company aims to improve key financial metrics like EPS and signal confidence in its long-term prospects, thereby boosting investor sentiment.

Should I invest based on this news alone?

While the stock retirement is a positive signal, it is not advisable to invest based on this single event. A thorough analysis of the company’s underlying fundamentals, including revenue growth, profit margins, and the performance of its key business segments, is essential for a sound investment decision.