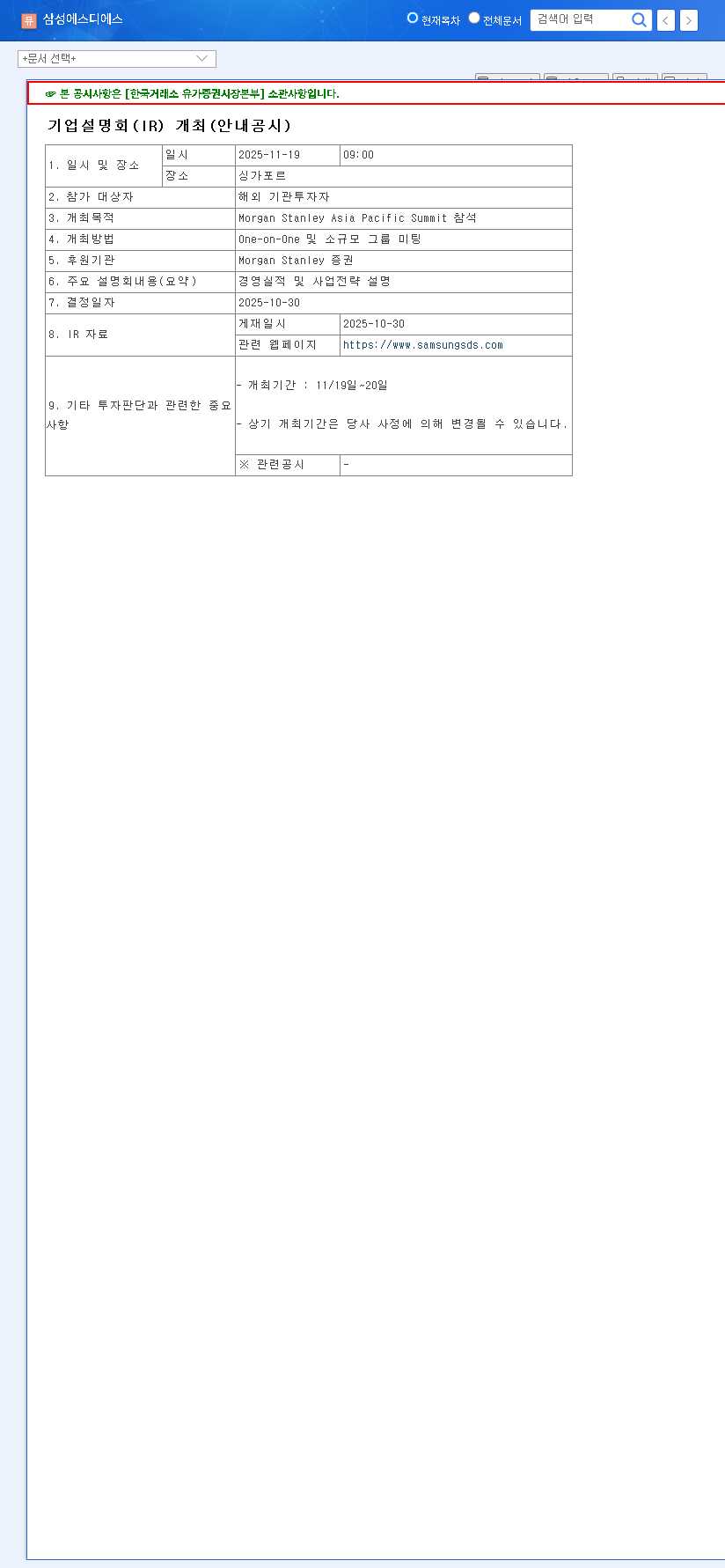

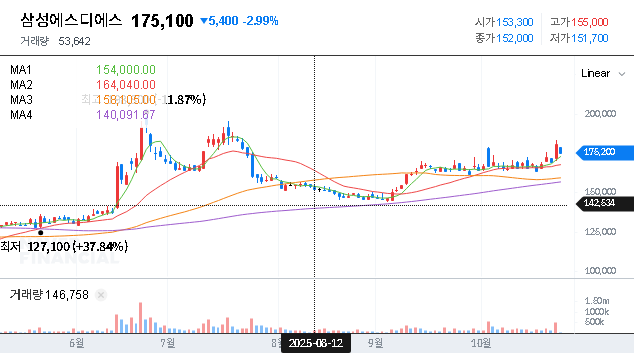

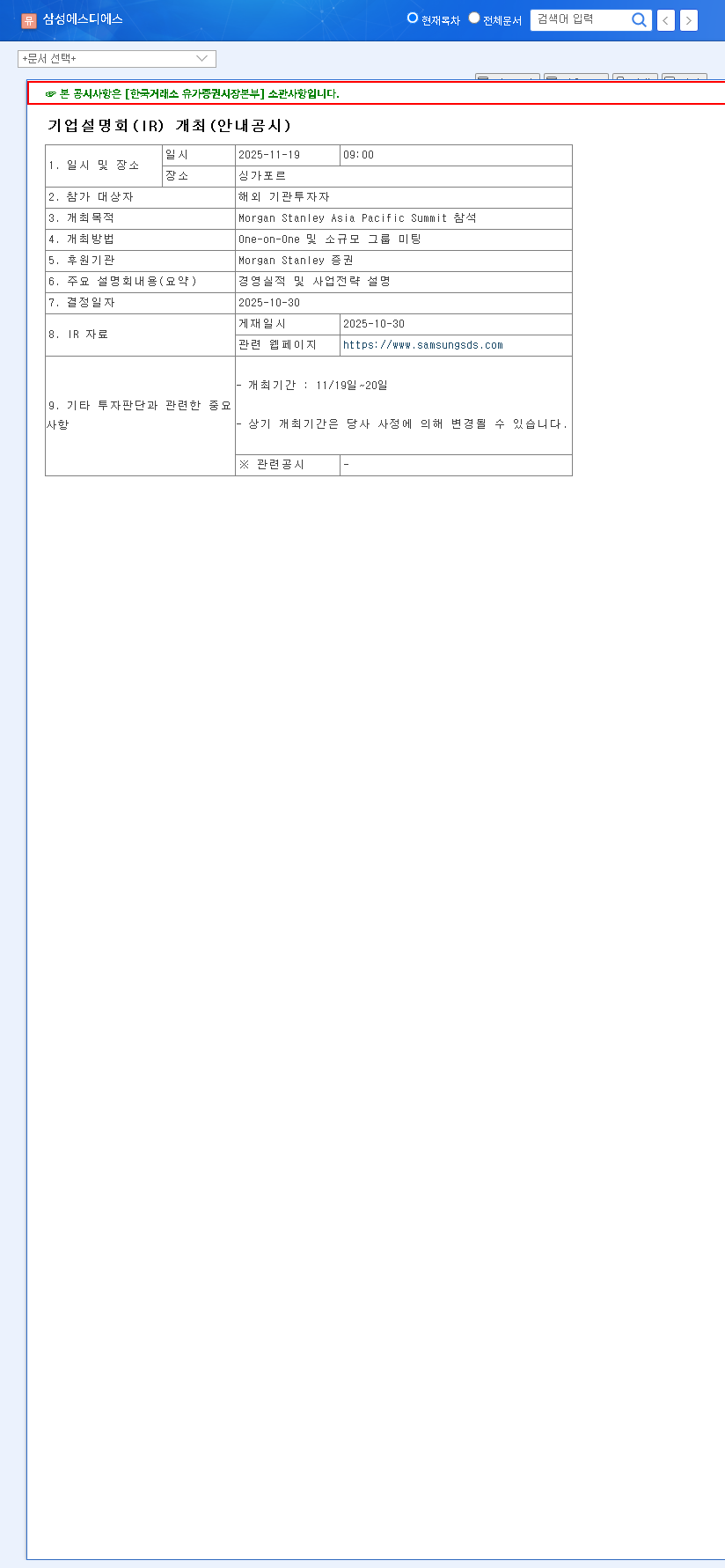

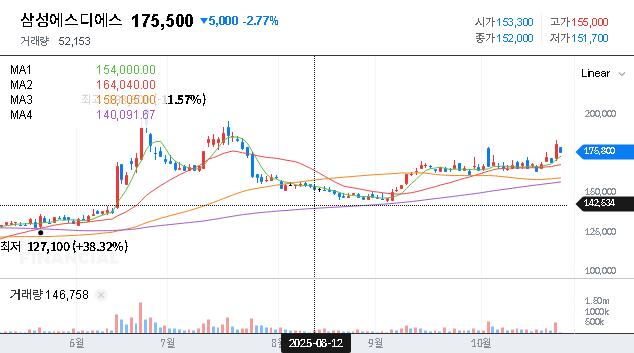

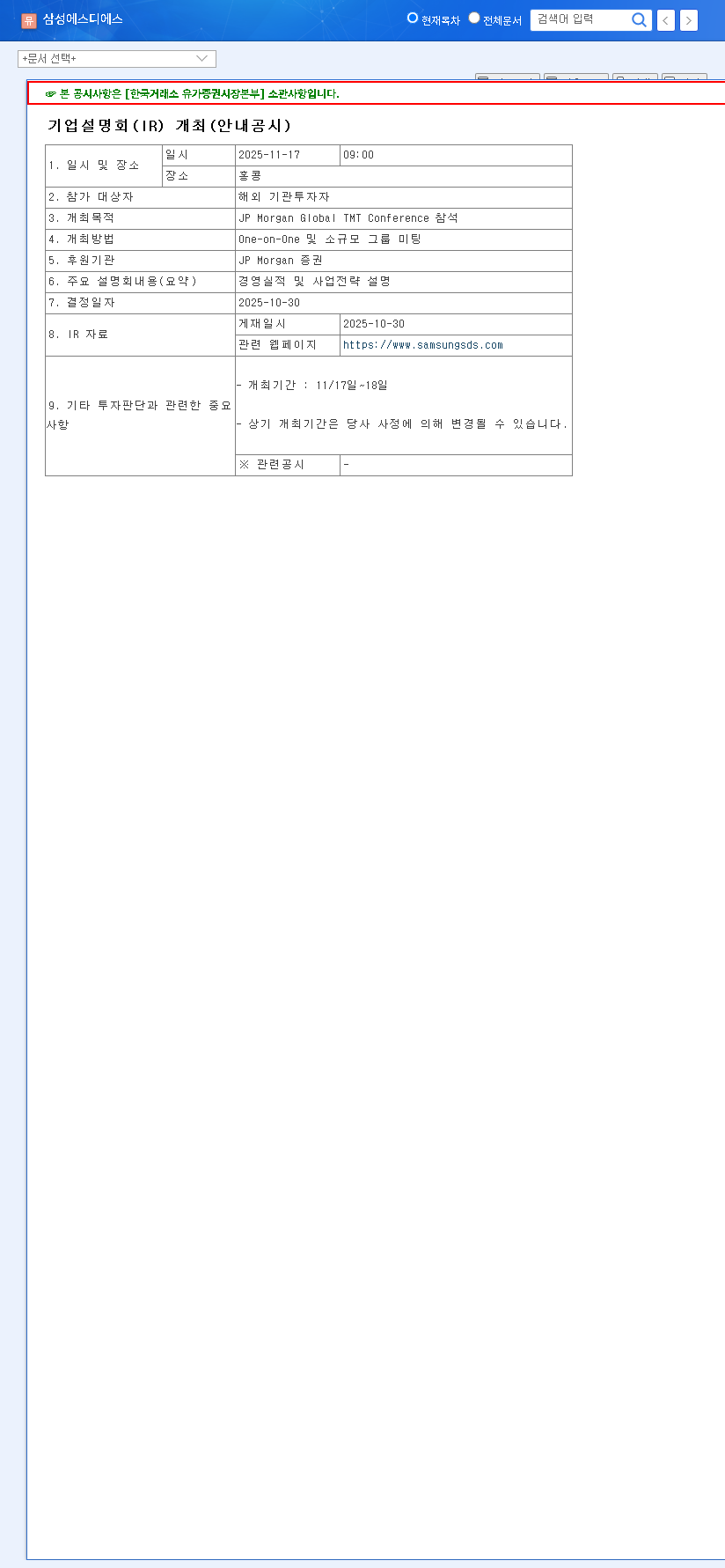

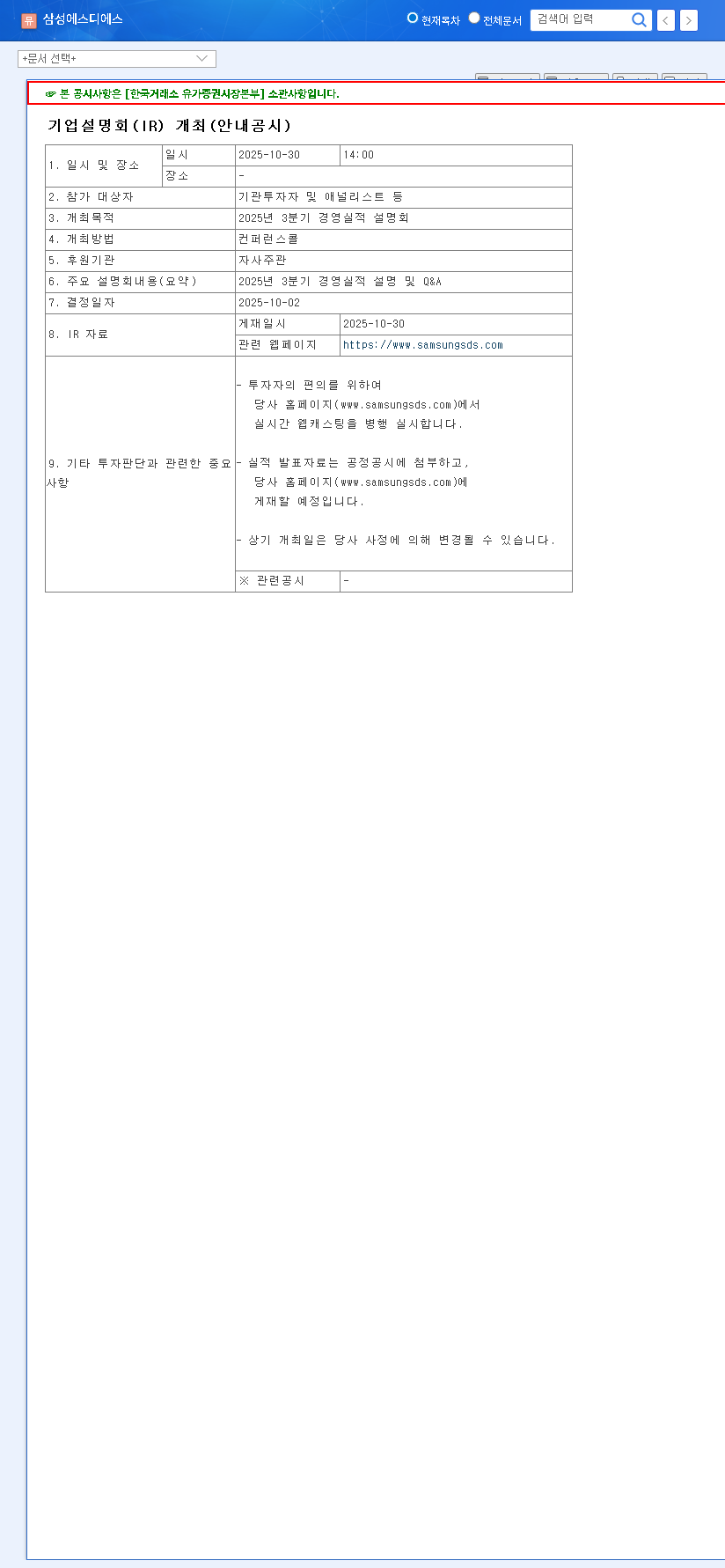

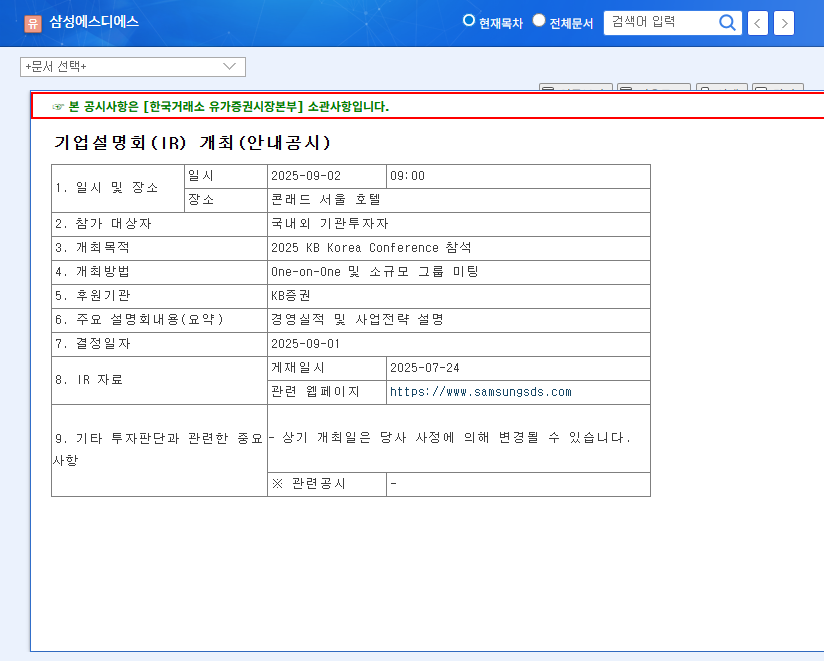

The upcoming EMRO Investor Relations event on November 19, 2025, is poised to be a pivotal moment for the company and its stakeholders. Following the release of its Q3 2025 results, investors are keenly focused on understanding the balance between aggressive strategic investments in AI and global expansion against a backdrop of short-term profitability pressures. This comprehensive analysis will dissect EMRO’s financial health, explore its core growth drivers, identify potential risks, and provide a clear action plan for evaluating the company’s long-term growth potential.

As a leader in Supply Relationship Management (SRM) solutions, EMRO is at a critical juncture. The decisions made today are shaping its trajectory in the competitive global SaaS market. Let’s delve into the data and strategy that will be central to the forthcoming EMRO Investor Relations conference.

Decoding EMRO’s Q3 2025 Financial Performance

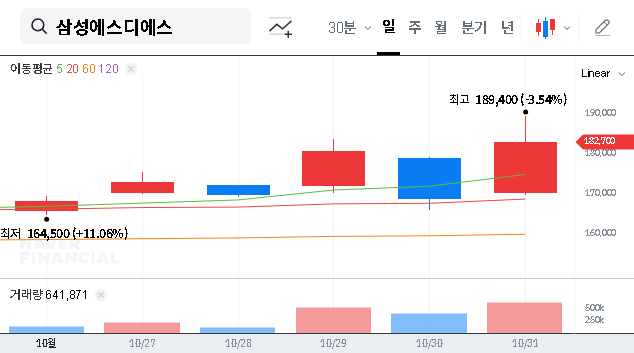

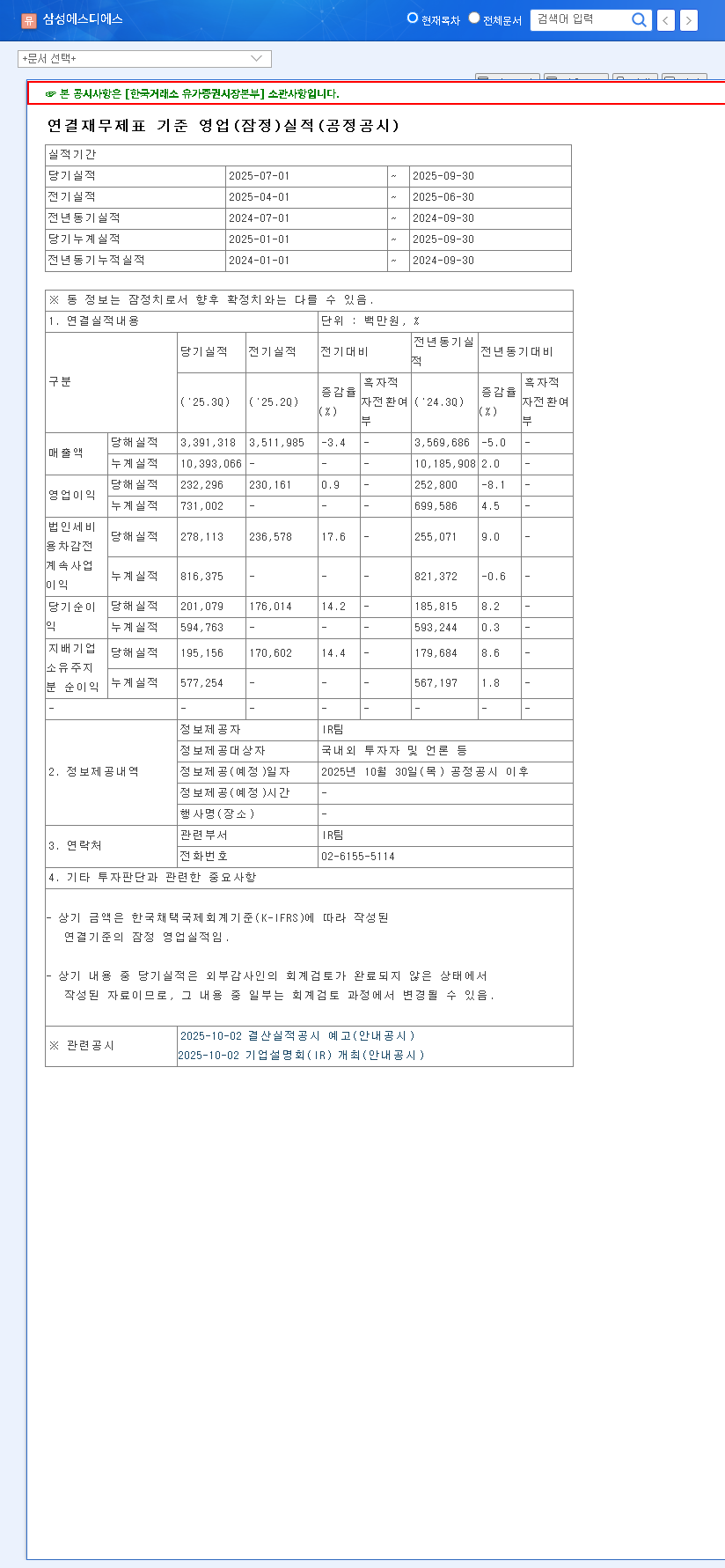

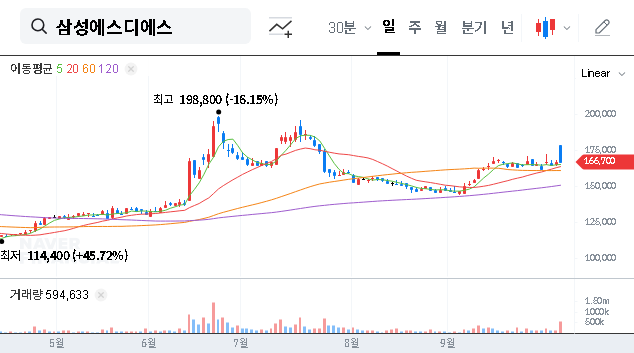

EMRO’s Q3 2025 financial report tells a story of strategic investment. While some headline numbers show a decline, they are the direct result of a calculated push into high-growth areas. Understanding this context is essential for any EMRO stock analysis. For a complete breakdown of the numbers, you can view the Official Disclosure on DART.

- •Revenue: Consolidated revenue reached 63.97 billion KRW. While a slight decrease year-over-year, it’s crucial to note the high dependency on a single client (‘Company A’), a point of risk that demands diversification.

- •Operating Profit: Recorded at 1.43 billion KRW, a significant drop from the prior year. This is primarily fueled by increased R&D and stock-based compensation costs earmarked for developing advanced AI SRM solutions and funding global expansion.

- •Net Income: A bright spot, reaching 2.21 billion KRW. The company successfully returned to profitability on a net basis, largely due to a tax expense refund.

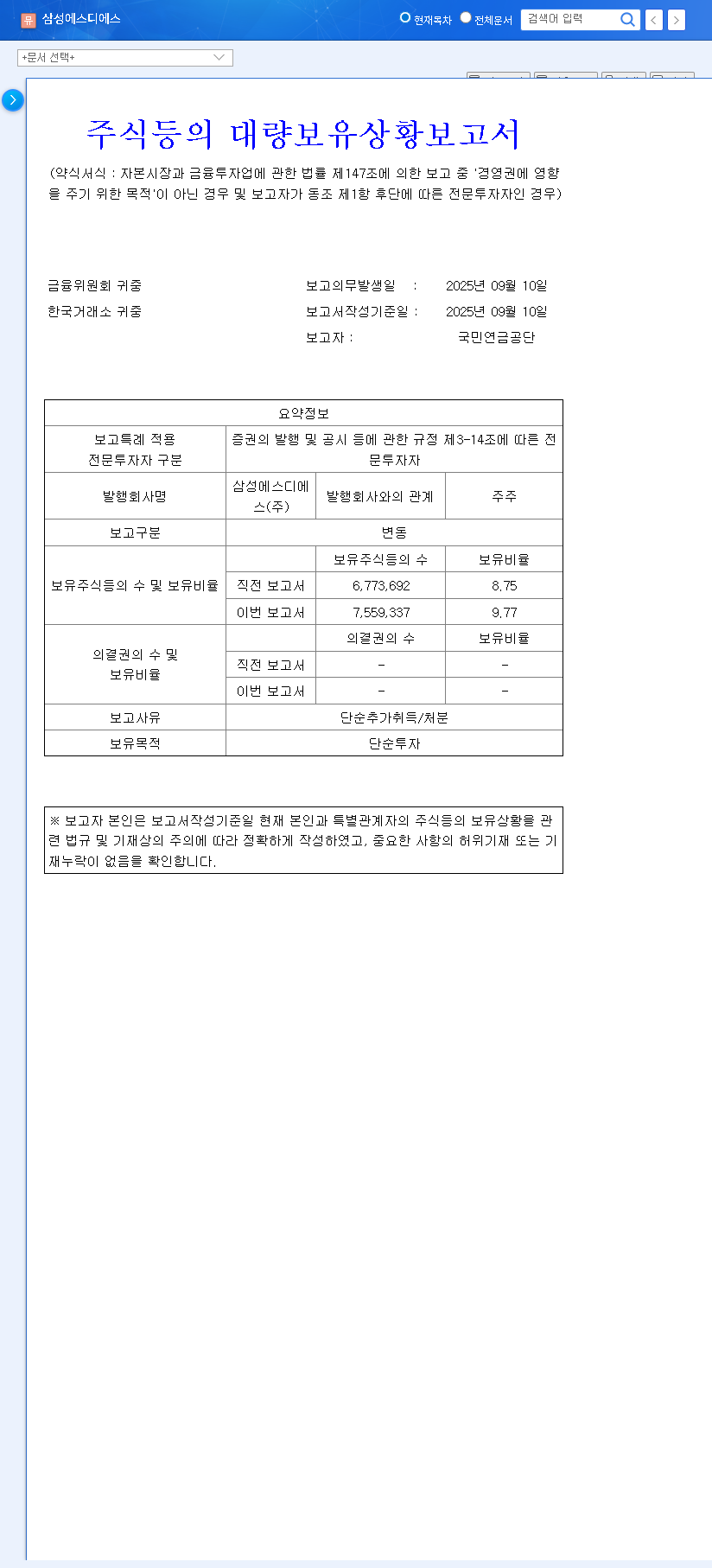

- •Financial Health: The debt-to-equity ratio has increased, reflecting the capital-intensive nature of its current growth phase. Investors will be looking for a clear strategy to manage this leverage moving forward.

EMRO is strategically sacrificing short-term profitability for a commanding long-term position in the global AI-powered supply chain market. The key is execution.

The Engines of Future Growth: AI & Global Markets

The decline in operating profit is not a sign of weakness but rather fuel for EMRO’s future. The company is betting big on two interconnected pillars that define its EMRO growth potential.

1. Advanced AI and Cloud-Based SRM Solutions

EMRO’s core competitive advantage lies in its sophisticated, Agentic AI-based software. Unlike basic automation, these solutions act as intelligent agents that can proactively manage supply chain complexities, predict disruptions, and optimize procurement. This aligns perfectly with the explosive growth in the global AI and SaaS markets, positioning EMRO as a key innovator. This technological edge has been validated by top industry analysis, including the prestigious IDC MarketScape Report, which recognizes EMRO’s strength in the AI-powered Source-to-Pay segment.

2. Aggressive Global Expansion (Caidentia)

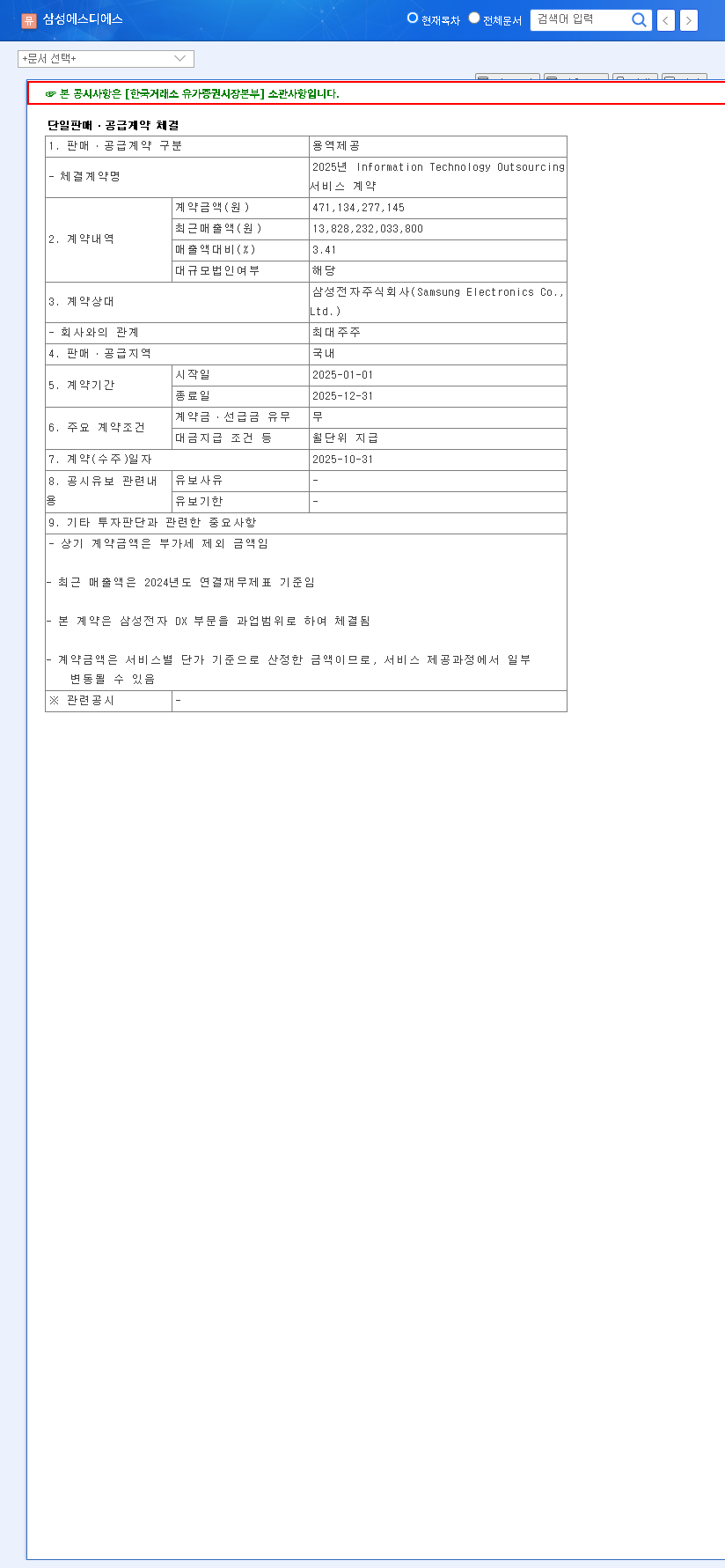

With its global SRM SaaS brand, Caidentia, EMRO is actively targeting the lucrative North American market. This expansion is not just a plan but a necessity for long-term growth and reducing client concentration risk. The synergy with partner Samsung SDS is a critical accelerator for this global push, providing crucial market access, credibility, and integration capabilities that would otherwise take years to build.

Navigating Headwinds: Risks Investors Must Monitor

While the long-term vision is promising, a prudent EMRO stock analysis must account for the challenges ahead. These are the key areas management needs to address at the EMRO Investor Relations meeting:

- •Client Diversification: A concrete plan to reduce the 47.5% revenue dependency on ‘Company A’ is non-negotiable for stable, long-term performance.

- •Path to Profitability: Investors need to see a clear roadmap detailing how and when the current investments will translate into improved operating profit margins.

- •Intensifying Competition: The AI and supply chain software space is crowded. EMRO must continually demonstrate its unique value proposition to fend off competitors.

- •Macroeconomic Pressures: While B2B SaaS is relatively resilient, a global slowdown could impact IT spending. Risk management strategies should be transparent.

Conclusion: A Strategic Bet on the Future

EMRO is at a crossroads, choosing to invest heavily in its future as a global leader in AI-powered SRM solutions. The short-term financial metrics reflect this ambitious strategy. The upcoming EMRO Investor Relations event is the company’s opportunity to articulate its vision, provide clarity on its execution plan, and build confidence that the current sacrifices will yield substantial future rewards. For investors, it’s a critical moment to listen, question, and ultimately decide if they believe in EMRO’s high-growth journey.

Disclaimer: This report is based on publicly available information and is for informational purposes only. It does not constitute investment advice. All investment decisions should be made based on the investor’s own judgment and due diligence.