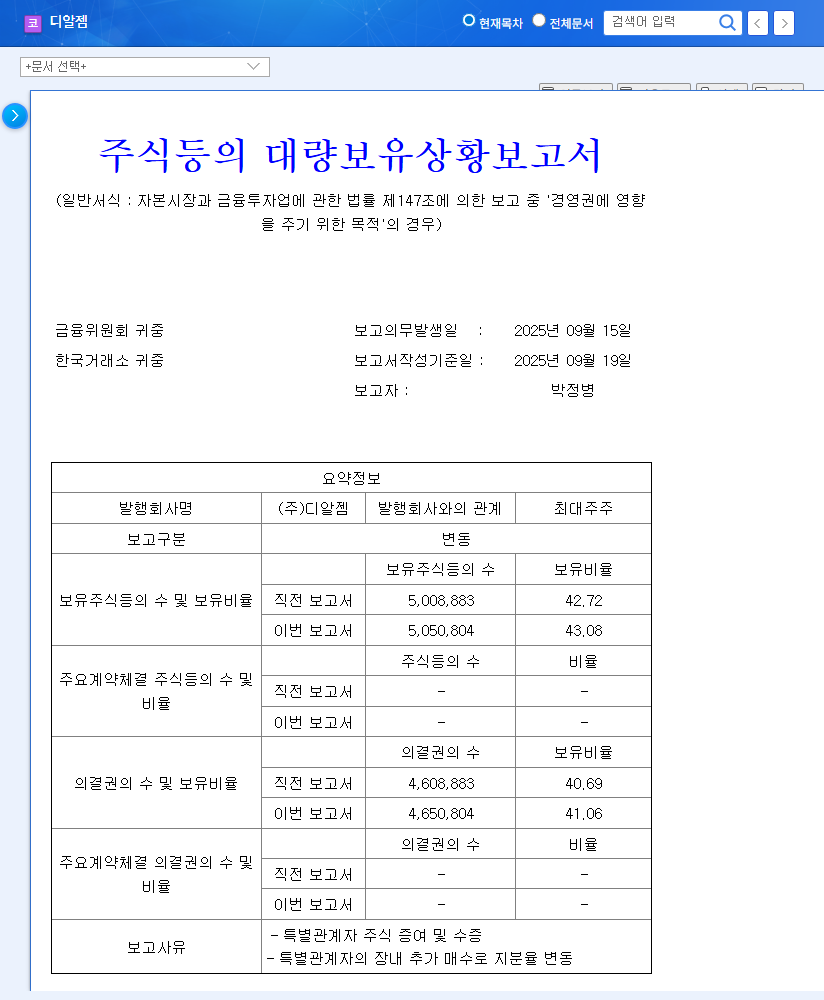

What Happened? : Analysis of DRGEM’s Stake Change Announcement

On September 19, 2025, DRGEM announced that CEO Park Jung-byung and related parties increased their stake from 42.72% to 43.08%, a 0.36%p increase. This resulted from gift transactions between related parties and additional purchases in the open market.

Why Does This Matter? : Analyzing the Positive and Negative Impacts

Positive Aspects: The increased stake suggests stabilized management and strengthened succession planning. Stable management enhances confidence in long-term investment and business plan execution.

Negative Aspects: The stake change alone cannot resolve fundamental issues such as declining sales and deteriorating profitability as highlighted in the 2025 semi-annual report.

What’s Next? : Stock Price and Market Outlook

In the short term, the strengthened management control may positively impact the stock price. However, the mid-to-long-term stock price trend depends on fundamental improvements. Closely monitoring future earnings announcements and the performance of business plans is crucial.

What Should Investors Do? : Key Investment Considerations

- Fundamental Improvement Trend: Verify sales recovery and profitability improvement.

- R&D Performance Materialization: Monitor whether R&D investments translate into tangible results.

- Exchange Rate Volatility Management: Analyze the impact of exchange rate fluctuations on company performance.

- New Business Strategy Execution: Evaluate the progress and results of new business initiatives.

- Market Competition: Pay attention to strategies for securing a competitive edge over competitors.

FAQ

What is DRGEM’s main business?

DRGEM is a manufacturer of medical imaging diagnostic equipment. They develop, manufacture, and sell digital X-ray systems and related solutions.

Will this stake change positively affect DRGEM’s stock price?

It may provide positive momentum in the short term, but the mid-to-long-term stock price trend depends on fundamental improvement.

What should I be cautious of when investing in DRGEM?

Consider factors such as declining sales and profitability trends, exchange rate volatility, and new business uncertainties.