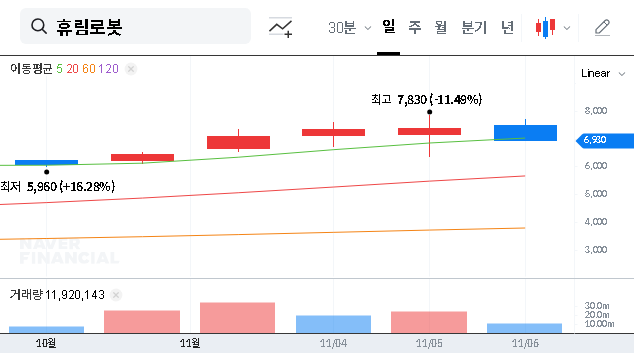

The outlook for Hyulim ROBOT stock has been thrown into uncertainty following the sudden and complete exit of a major shareholder. Edge Foundry, a significant stakeholder, has divested its entire position, sending ripples through the market. Is this a simple case of profit-taking, or does it point to deeper cracks in the company’s foundation? This analysis will dissect the situation, providing investors with a clear path forward.

We will explore the details of Edge Foundry’s sale, conduct a deep dive into Hyulim ROBOT’s current financial health, analyze the potential impact on the stock price, and outline a strategic action plan for current and prospective investors. Navigating this volatility requires a clear understanding of the underlying fundamentals of your Hyulim ROBOT investment.

The Catalyst: Edge Foundry’s Full Divestment

On October 23, 2025, a significant market event occurred. According to the Official Disclosure, Edge Foundry, a key reporting shareholder, executed an on-market sale of its entire stake in Hyulim ROBOT. This amounted to a substantial 3,828,871 shares, which represented 5.13% of the company’s total stock. The stated purpose for holding the shares was ‘simple investment,’ suggesting the move wasn’t aimed at influencing management but rather driven by financial motives. However, the complete liquidation of such a large position inevitably raises questions and fuels market speculation.

The sale of a 5.13% stake is not a minor portfolio adjustment; it’s a statement. The market is now forced to ask ‘why?’, and the answer lies within Hyulim ROBOT’s complex financial picture.

Deep Dive: Hyulim ROBOT Stock Fundamentals

To understand the potential rationale behind the sale and to chart a course for the future of Hyulim ROBOT stock, a thorough examination of its fundamental health is crucial. The picture is mixed, with glimmers of strategic promise overshadowed by significant financial strain.

The Bear Case: Profitability and Financial Instability

Despite ambitious ventures into new sectors like the metaverse and AI semiconductors, Hyulim ROBOT’s core business is struggling. As of the first half of 2025, revenue saw a decline to 103.25 billion KRW. While the consolidated operating profit technically turned positive, this is misleading. It’s largely a statistical anomaly resulting from a massive operating loss of -493.8 billion KRW in the prior year. The more telling figures are the consolidated net loss of 13.22 billion KRW and, more alarmingly, the parent company’s separate net loss of 62.09 billion KRW. This points to a severe profitability crisis at the heart of the company.

The company’s financial structure is equally concerning. The parent company’s separate debt-to-equity ratio stands at a precarious 127.5%, indicating that its debts significantly outweigh its equity. Frequent capital changes through convertible bonds and capital increases have created a volatile financial environment, potentially diluting shareholder value. Compounding these issues is a history of non-diligent disclosures, which can erode investor trust and corporate credibility.

The Bull Case: Glimmers of Potential

Not all indicators are negative. Hyulim ROBOT’s strategic pivot into high-growth areas like AI is a forward-looking move that could secure future growth engines. For a broader view on this sector, you can review our analysis of the global robotics industry. Furthermore, on a consolidated basis, the debt-to-equity ratio has improved to a more manageable 49.4%, and the operating profit did show a positive swing. These points suggest that if the company can stabilize its core operations and successfully execute on its new ventures, there is a potential path to recovery.

Stock Price Impact and Investor Action Plan

Edge Foundry’s divestment will likely have a multi-stage impact. In the short term, the market must absorb nearly 4 million shares, creating significant selling pressure and potentially driving the price down. The exit of a major shareholder also weakens investor sentiment, as it can be interpreted as a vote of no confidence in the company’s future.

In the mid-term, this is a supply-and-demand issue rather than a management crisis. However, this imbalance can lead to heightened volatility. This is amplified by the macroeconomic backdrop of sustained high-interest rates, as noted by sources like Bloomberg, which increases the financial burden on indebted companies like Hyulim ROBOT.

A Prudent Strategy for Hyulim ROBOT Investment

Given the significant fundamental weaknesses and the immediate downward pressure from the share sale, a cautious and conservative approach is warranted.

- •Adopt a Wait-and-See Stance: Rushing into a position now is risky. It’s advisable to observe from the sidelines how the market absorbs the divested shares and where the stock price finds its new support level.

- •Monitor Fundamental Improvements: Before considering an investment, look for tangible evidence of a turnaround. This includes sustained profitability, a significant improvement in the parent company’s financial structure, and concrete, positive results from new business ventures.

- •Watch for Financial Discipline: The key to long-term appreciation is financial health. Pay close attention to any announcements or actions aimed at reducing the parent company’s severe debt load. Without this, any growth will be built on an unstable foundation.

In conclusion, the Hyulim ROBOT stock is at a critical juncture. The short-term outlook is bearish due to overwhelming supply pressure and weak fundamentals. Cautious investors should demand clear signs of financial and operational improvement before committing capital.