DYPNF Co., Ltd. has captured the market’s attention with a significant announcement: a 3 billion KRW treasury stock cancellation. This move, a classic DYPNF stock buyback and cancellation strategy, is typically a bullish signal designed to enhance shareholder value. However, it comes at a time when the company is grappling with severe performance headwinds, including a major contract termination. This leaves investors at a critical crossroads: is this a genuine catalyst for long-term growth or merely a temporary boost to a struggling stock price?

This comprehensive analysis dissects the implications of the DYPNF stock cancellation. We will delve into the company’s financial health, the stark contrast of its operational challenges, and what this strategic move means for your investment portfolio in 2024 and beyond.

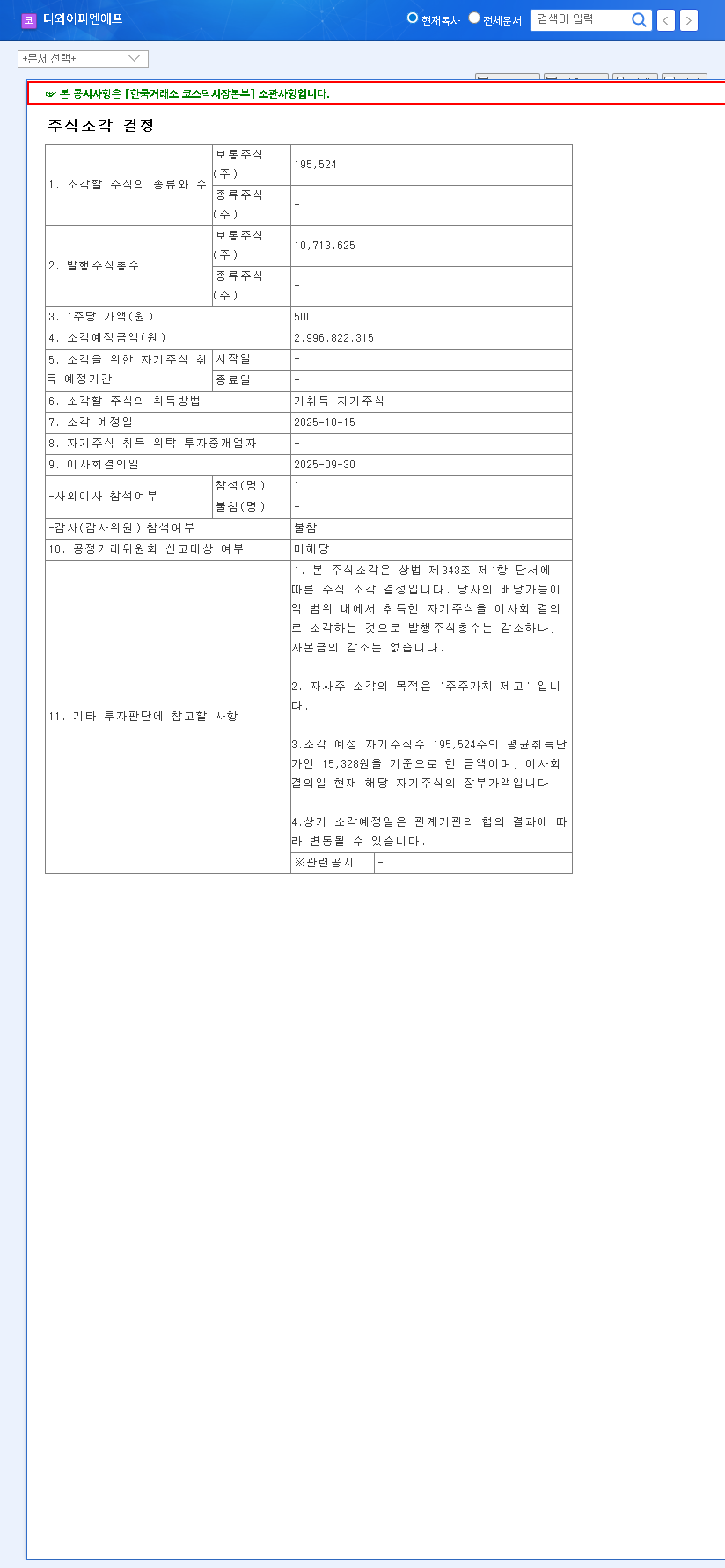

What is the DYPNF Stock Cancellation?

DYPNF Co., Ltd. has committed to canceling 195,524 of its common shares, valued at 3 billion KRW, with the cancellation scheduled for October 15, 2025. This process involves the company using its own funds to buy back its shares from the open market and then permanently retiring them. By reducing the total number of outstanding shares (in this case, by approximately 1.96%), the value of each remaining share theoretically increases. This is a direct method of returning capital to shareholders and is often interpreted by the market as a sign of management’s confidence in the company’s future prospects and undervalued stock price.

The Bull Case: Why This Buyback is a Positive Sign

Enhancing Per-Share Value

The most immediate benefit of a stock cancellation is the enhancement of key financial metrics. With fewer shares in circulation, metrics like Earnings Per Share (EPS) and Book Value Per Share (BPS) automatically increase. A higher EPS can make the stock appear more attractive to investors, potentially leading to a higher valuation over time. This is a fundamental way to increase shareholder value.

Improving Supply and Demand

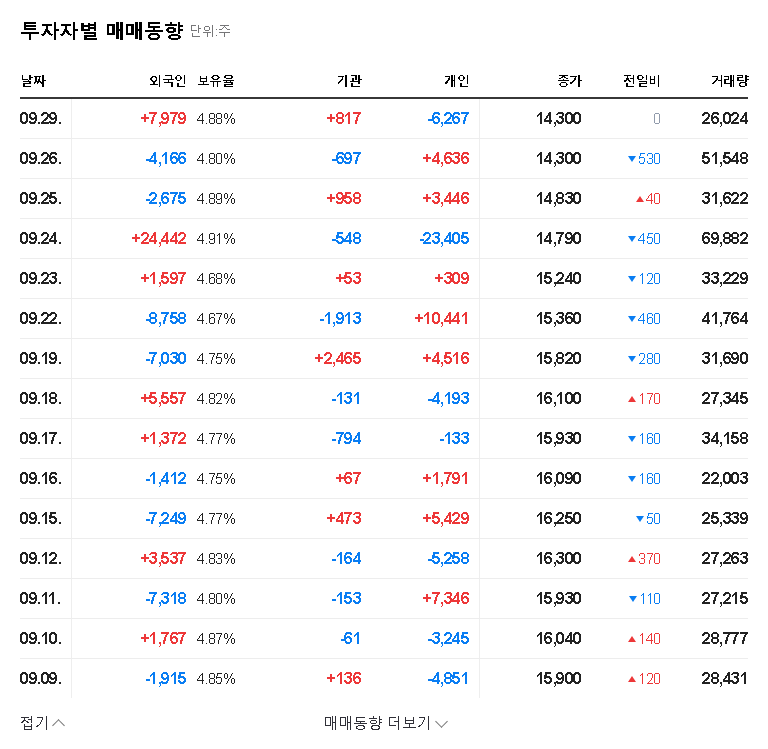

Basic economics dictates that reducing the supply of an asset can increase its price, assuming demand remains constant or grows. By removing nearly 2% of its shares from the market, DYPNF is tightening the available supply. This can help stabilize the DYPNF stock price by absorbing selling pressure and creating a more favorable supply-demand balance for existing shareholders.

The Bear Case: Fundamental Headwinds Persist

A Devastating Contract Termination

The positive news of the DYPNF stock buyback is overshadowed by a significant operational blow: the termination of a 9.019 billion KRW contract with ENTER Engineering Pte. Ltd. This setback, blamed on the global economic downturn, creates a massive hole in the company’s revenue stream and fundamentally alters its 2024 outlook.

2024 Projections for DYPNF are grim: Revenue is expected to plummet to 316 billion KRW from 823 billion KRW in 2023. Operating profit is projected at a staggering loss of -159 billion KRW, with a net profit loss of -14 billion KRW. This represents a severe operating profit margin of -50.29%.

No amount of financial engineering can completely mask such a dramatic decline in core business performance. The key question for the DYPNF stock price is whether the company can secure new contracts to fill this void.

Unproven Growth Engines

While DYPNF is making efforts to diversify into new growth sectors like secondary batteries and hydrogen, these are long-term plays. The company needs to show tangible, revenue-generating results from these ventures soon to convince investors that a sustainable turnaround is underway. Until then, they remain speculative ventures rather than reliable profit centers.

Investment Strategy and Final Verdict

The decision to proceed with a stock cancellation amidst poor DYPNF performance is a double-edged sword. On one hand, it’s enabled by the company’s impressively sound financial health—its debt-to-equity ratio is projected to be a very low 7.90% in 2024. This financial stability allows it to reward shareholders even in tough times.

However, investors should be cautious. A stock buyback can put a floor under a stock price, but it cannot create a ceiling of growth if the underlying business is failing. For more details, investors can review the Official Disclosure (Source: DART). If you are new to this type of analysis, consider reading our guide to analyzing company financials for more context.

Key Takeaways for Investors:

- •Short-Term Positive: The stock cancellation is a clear short-term positive, likely to provide some support for the stock price and reward loyal shareholders.

- •Long-Term Concern: The fundamental issue is the dramatic drop in revenue and profitability. The buyback does not solve this problem.

- •Monitor Core Business: The primary focus should be on whether DYPNF can secure new, large-scale orders to replace the lost contract.

- •Watch New Ventures: Look for concrete progress and revenue generation from the secondary battery and hydrogen initiatives.

Recommendation: While the DYPNF stock buyback is a commendable sign of financial strength and pro-shareholder sentiment, it should be viewed as a defensive maneuver, not an offensive growth strategy. A cautious, long-term approach is advised, prioritizing fundamental business recovery over the short-term hype of the share cancellation.