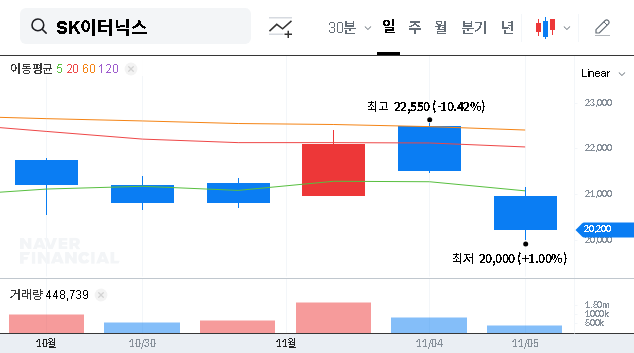

The recent market buzz surrounding SK eternix Co., Ltd. has reached a fever pitch following reports that its major shareholder, SK discovery, is exploring a potential stake sale. This news has created significant uncertainty, leaving investors to parse rumors and navigate potential stock volatility. While an official clarification has been issued, the core question remains: What does this mean for the future of SK eternix Co., Ltd. and its investors?

This comprehensive analysis unpacks the entire situation. We will dissect the company’s fundamental health based on the H1 2025 report, evaluate the potential short and long-term impacts of the SK eternix divestment scenario, and provide clear, actionable insights to help you make informed decisions in this dynamic environment.

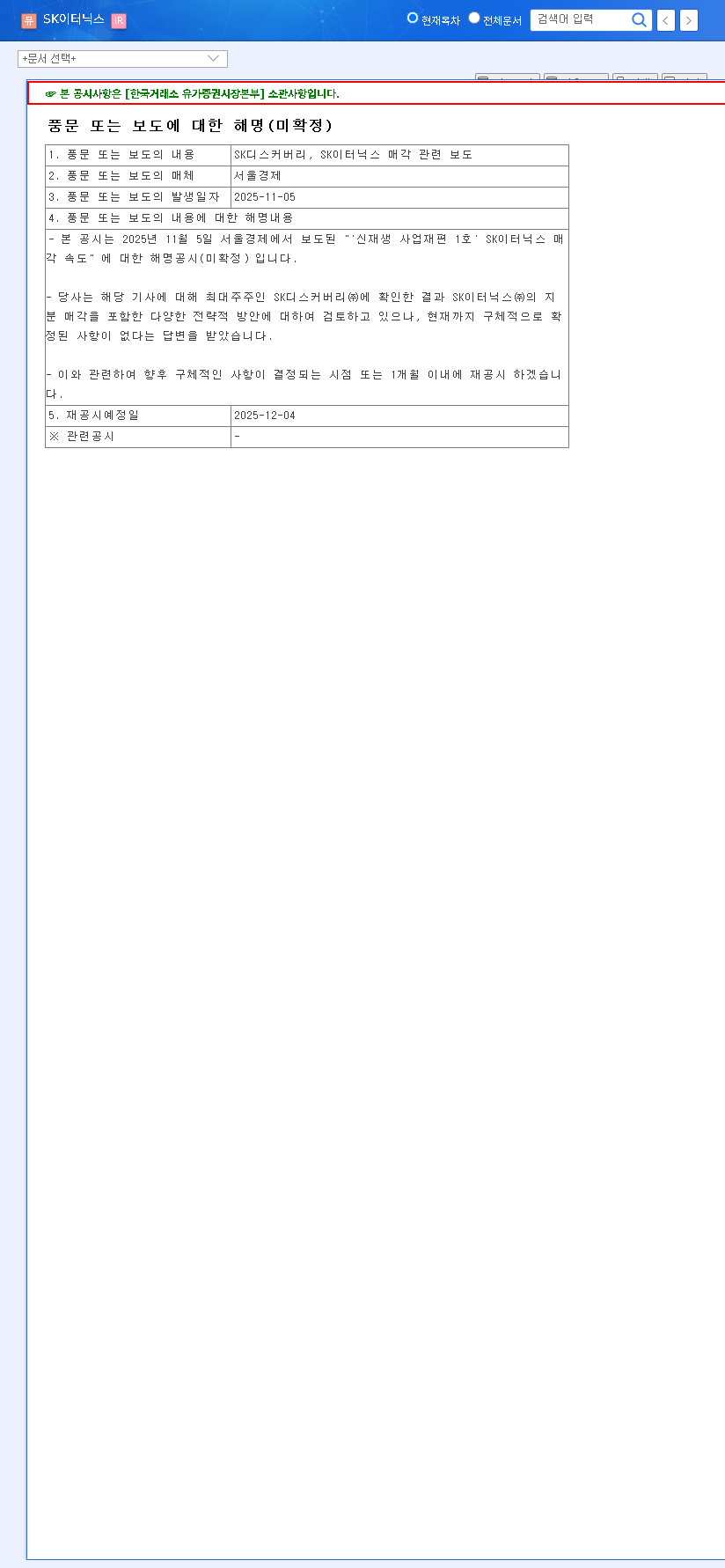

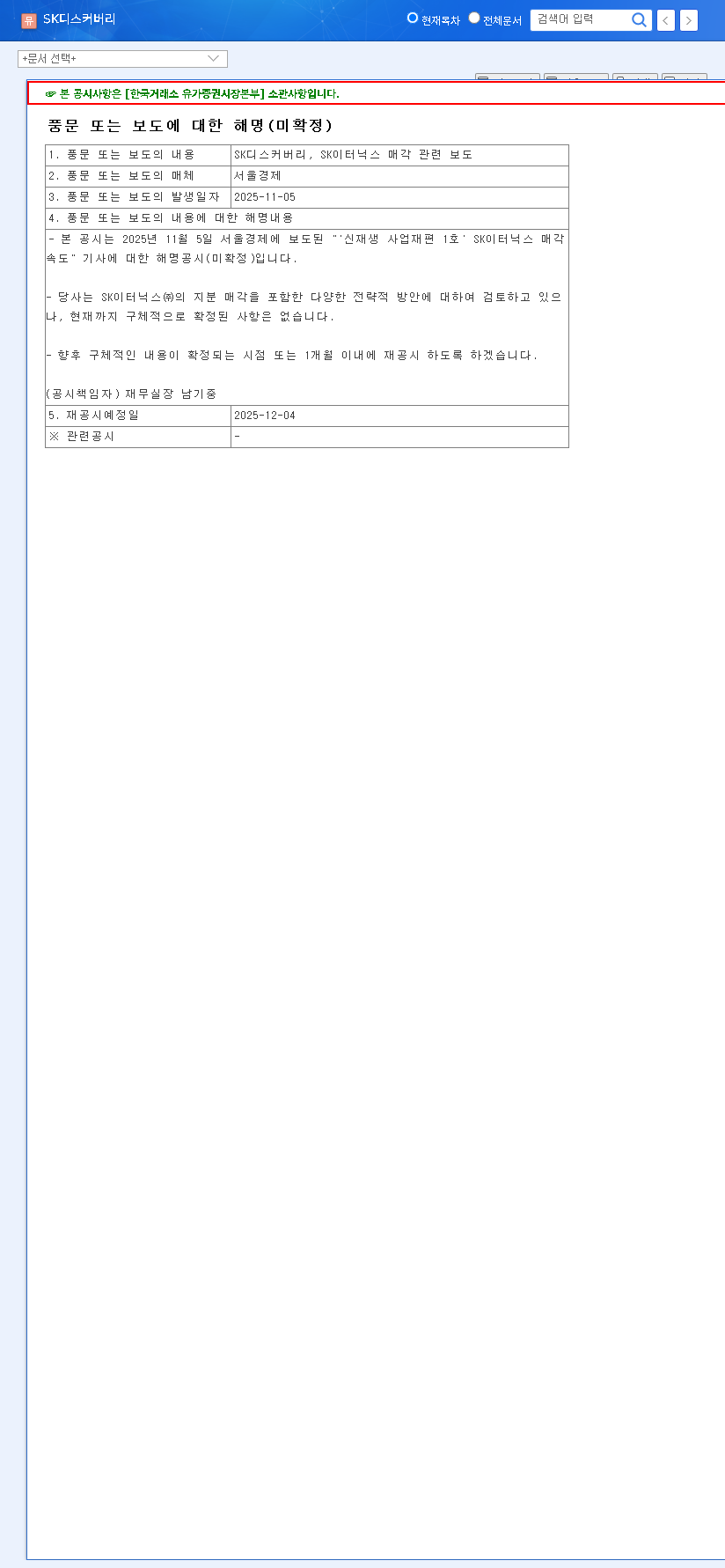

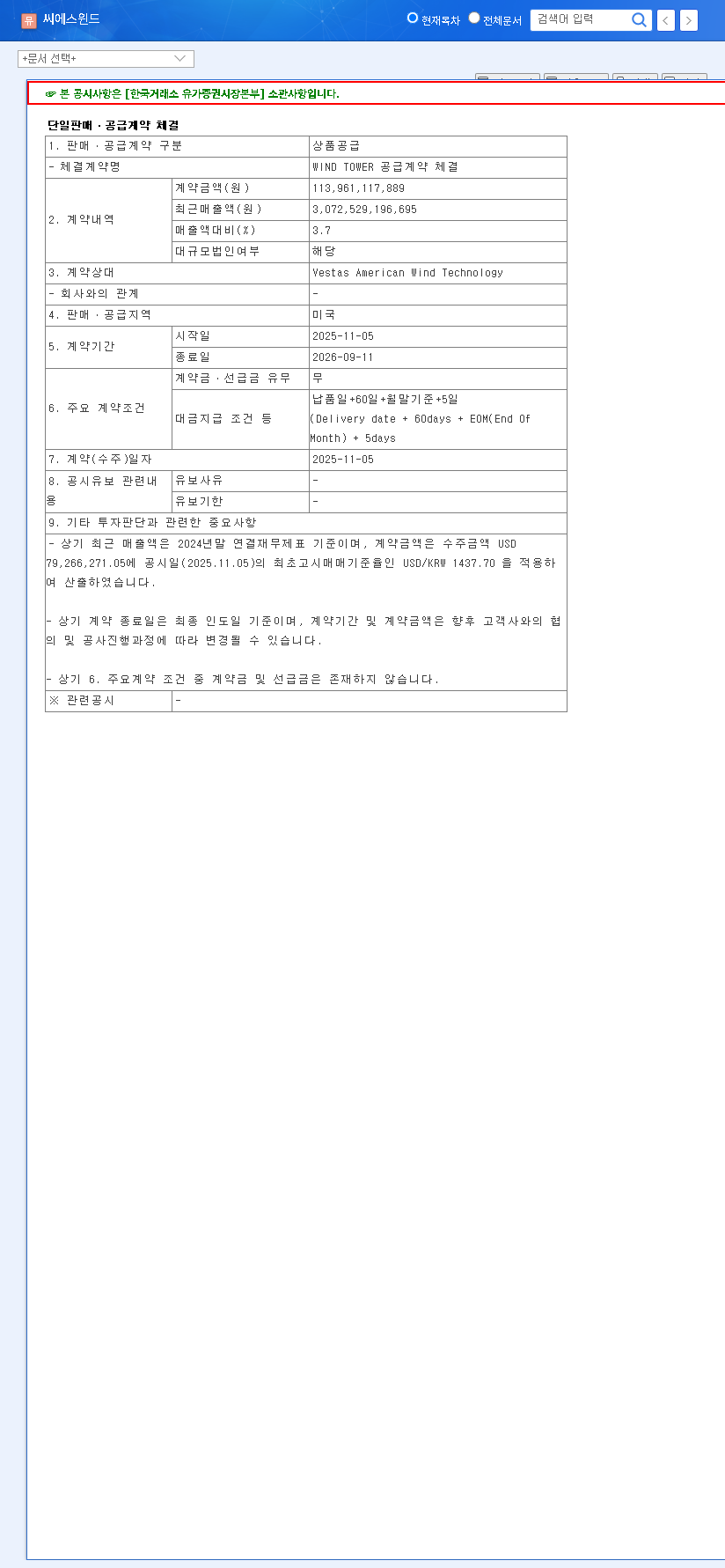

The Divestment Report and Official Clarification

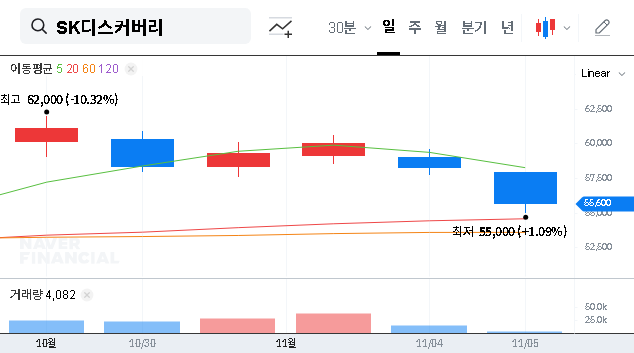

On November 5, 2025, a report from the Seoul Economic Daily catalyzed market speculation. In response, SK eternix Co., Ltd. promptly issued a formal disclosure to address the rumors. The company’s statement provides a crucial piece of the puzzle for investors trying to gauge the situation.

SK discovery, the major shareholder, is reviewing various strategic options, including the sale of its stake in SK eternix Co., Ltd., but nothing has been specifically confirmed to date. The company will re-disclose specific details within one month. — Official Disclosure (DART)

This ‘unconfirmed’ status places the company in a state of limbo. While it confirms that a sale is on the table, the lack of a concrete decision introduces a significant variable that will likely fuel stock price volatility until the follow-up disclosure is released.

Fundamental Health: An H1 2025 Deep Dive

Beyond the M&A noise, the intrinsic value of SK eternix Co., Ltd. is rooted in its operational performance. An analysis of its H1 2025 report reveals a company with powerful growth engines but also notable financial challenges.

Strengths and Growth Drivers

- •Surging Renewable Energy Business: Revenue contribution from this sector skyrocketed from 8.0% to 32.1% year-on-year. This growth is fueled by global demand for RE100 solutions and key domestic projects like the Shinan-Uii offshore wind farm.

- •Expanding ESS Business: The Energy Storage System (ESS) division saw its revenue share double from 7.9% to 15.5%, solidifying its market position and highlighting successful global expansion.

- •Improved Profitability: Strong operating profit margins in both renewable energy (22.3%) and ESS (11.8%) signal enhanced operational efficiency and strong pricing power.

- •Future-Proof Portfolio: Diversification across solar, wind, fuel cells, and ESS, coupled with ambitions to become a Virtual Power Plant (VPP) operator, creates a resilient and forward-looking business model.

Potential Risks and Financial Headwinds

- •High Debt Ratio: A debt-to-equity ratio of 380.96% is a significant concern, increasing financial fragility and exposure to interest rate hikes.

- •Negative Operating Cash Flow: An increase in working capital has strained cash flow, indicating a need for diligent short-term liquidity management.

- •Currency Exposure: Rising foreign currency debt makes the company’s bottom line vulnerable to exchange rate volatility, particularly with USD/KRW and EUR/KRW fluctuations.

- •Rising Inventory Levels: An increase in inventory could signal potential sales slowdowns or inefficiencies in supply chain management that warrant monitoring.

Impact of the Divestment on SK Eternix Stock

The primary driver of the SK eternix stock price in the near term will be the resolution of this divestment issue. The outcome will have vastly different implications.

Short-Term Impact: Heightened Volatility

Until the re-disclosure date, expect significant price swings based on rumors and speculation. Trading patterns from foreign investors will be a key indicator of market sentiment. The global renewable energy sector’s performance, as tracked by agencies like the International Energy Agency (IEA), will also provide a macroeconomic backdrop.

Mid-to-Long-Term Impact: Two Diverging Paths

- •Scenario 1: Divestment is Confirmed. The outcome depends on the buyer and the deal’s structure. A strategic buyer could unlock new synergies and provide capital for growth (positive). Conversely, a sale at a low valuation or to a financially weak entity could be detrimental (negative).

- •Scenario 2: Divestment is Cancelled. This would shift focus back to the company’s fundamentals. If the growth momentum continues and management addresses financial weaknesses, the stock could recover. However, a wave of disappointment-driven selling from speculators could cause a short-term price drop.

Conclusion: Key Observation Points for Investors

SK eternix Co., Ltd. is at a crossroads. Its strong performance in high-growth sectors like renewable energy is undeniable, but this is counterbalanced by financial vulnerabilities and the overarching uncertainty of the potential SK discovery stake sale. The upcoming re-disclosure is the single most important catalyst for the stock’s future direction.

Investors should adopt a cautious stance and monitor the following points closely:

- •The Re-Disclosure Content: The details (or lack thereof) will determine the next major price movement.

- •Financial Health Initiatives: Watch for any proactive steps by the company to reduce debt and improve cash flow, independent of the sale.

- •Business Performance: Continued growth in its core businesses will provide a fundamental floor for the stock’s valuation. For more on this, see our guide to evaluating renewable energy investments.

[Disclaimer] This analysis is for informational purposes and is based on publicly available data. All investment decisions carry risk, and the final responsibility rests with the individual investor.