In the dynamic world of stock market investing, an insider’s transaction can speak louder than a press release. The recent HBL Corporation shareholding change is a pivotal event that demands close attention. This report, detailing a reduction in CEO Kim Jeong-muk’s stake, offers critical clues about the company’s internal confidence, management stability, and future trajectory. For investors, understanding the nuances of this development is key to navigating what comes next for HBL Corporation’s stock price.

This comprehensive analysis will dissect the official filing, evaluate the company’s current financial health, and project the potential short-term and long-term impacts, providing a clear roadmap for your investment strategy.

The Catalyst: Deconstructing the Shareholding Report

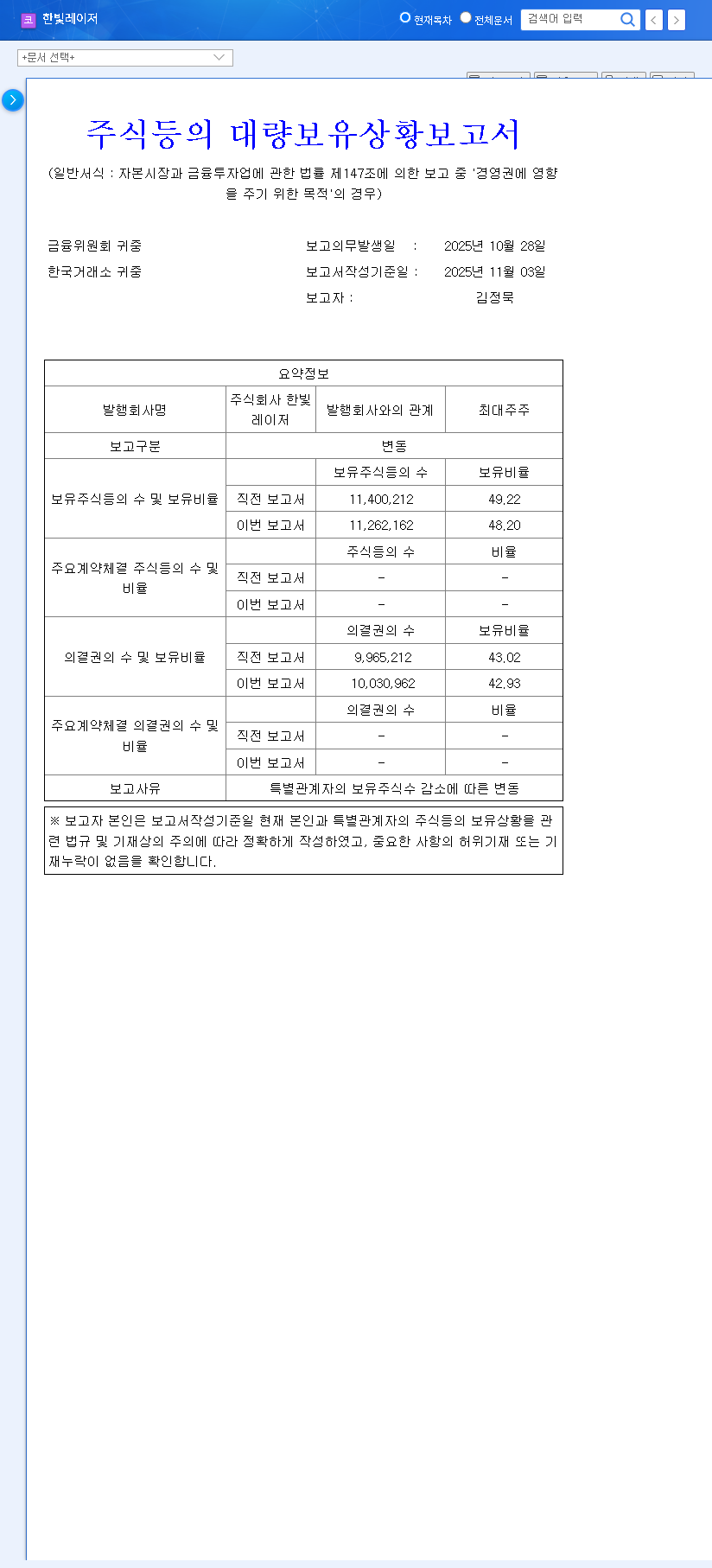

On November 3, 2025, HBL Corporation (also known as 한빛레이저) filed a ‘Report on Large Shareholding Status’ concerning its CEO, Kim Jeong-muk. The core of this announcement was a change in his ownership stake, which is officially held for the purpose of ‘management influence.’ The change was triggered by the open market sale of 30,000 shares by a specially related party, Mr. Cho Young-hoon. You can view the Official Disclosure on the DART system for full details.

- •Shareholder: CEO Kim Jeong-muk (and related parties)

- •Ownership Before Report: 49.22%

- •Ownership After Report: 48.20%

- •Net Change: 1.02 percentage point decrease

- •Reason: Open market sale by a related party.

HBL Corporation Fundamentals: A Tale of Headwinds and Hope

This shareholding change doesn’t happen in a vacuum. A thorough HBL Corporation stock analysis must consider the company’s underlying financial health, which presents a mixed picture.

Current Financial Challenges

Based on the semi-annual report for 2025, HBL is navigating significant turbulence:

- •Revenue & Profitability Issues: A downturn in the automotive manufacturing equipment sector has led to declining revenue and an operating loss.

- •Rising Inventory: Sales stagnation is causing inventory to pile up, which can tie up capital and signal weakening demand.

- •High Leverage: The debt-to-equity ratio has climbed to a concerning 230.13%. While not an immediate liquidity crisis, this level of debt increases financial risk. For more on this metric, see this guide on understanding debt ratios from Investopedia.

The Growth Engine: Secondary Battery Business

Despite the challenges, HBL Corporation is not standing still. The company is making a strategic pivot into the high-growth secondary battery business, specifically manufacturing charging and discharging equipment. This move, supported by consistent R&D investment, represents a crucial effort to diversify revenue streams and tap into the burgeoning electric vehicle (EV) and energy storage markets. The success of this venture is arguably the most important factor for the company’s long-term future.

Analyzing the Impact: Management, Sentiment, and Stock Price

Is Management Control at Risk?

With a remaining stake of 48.20%, CEO Kim Jeong-muk’s control over the company remains solid. A hostile takeover is highly unlikely. However, the signal this insider sale sends to the market is more psychological. When a key figure whose stated purpose is ‘management influence’ reduces their holdings—even through a related party—it raises questions about their long-term conviction. The lack of a clear reason for the sale only adds to this uncertainty.

The market often interprets an insider sale as a sign of peaking confidence. While not always the case, it creates a headwind for investor sentiment, especially when a company’s fundamentals are already under pressure.

Short-Term vs. Long-Term Stock Price Outlook

In the short term, the HBL Corporation shareholding change is likely a negative catalyst. It gives skeptical investors another reason to sell or stay on the sidelines. The stock, already down significantly from its 2024 peak, may face additional downward pressure as the market digests this news.

The long-term perspective, however, depends almost entirely on fundamental execution. A turnaround in the stock price will not be driven by shareholding reports, but by tangible business results. If HBL can demonstrate strong growth and profitability from its secondary battery business, this small ownership change will become a footnote in a larger success story. For more on this sector, read our guide to secondary battery investments.

Investor Action Plan & Key Variables to Watch

This event makes a cautious approach prudent. Investors should weigh the following factors:

Bull Case (Opportunities)

- •High Growth Potential: The secondary battery market is expanding rapidly, and successful entry could transform HBL’s financial profile.

- •Stable Management: Despite the reduction, the CEO’s 48.20% stake ensures stable leadership for the foreseeable future.

- •Depressed Valuation: With the stock price already low, much of the negative news may already be priced in, offering potential value.

Bear Case (Risks)

- •Weakening Fundamentals: The core business is struggling, and the turnaround is not yet proven.

- •Negative Insider Signal: The sale, regardless of size, undermines investor confidence.

- •Macroeconomic Headwinds: High interest rates and a global economic slowdown could further hamper the automotive sector and delay recovery.

Ultimately, the HBL Corporation shareholding change serves as a warning sign that amplifies existing concerns. The path to stock price recovery will be paved with improved earnings and tangible success in new ventures, not by stabilizing shareholding reports. Investors should monitor quarterly earnings reports and any news related to the secondary battery division with extreme diligence.