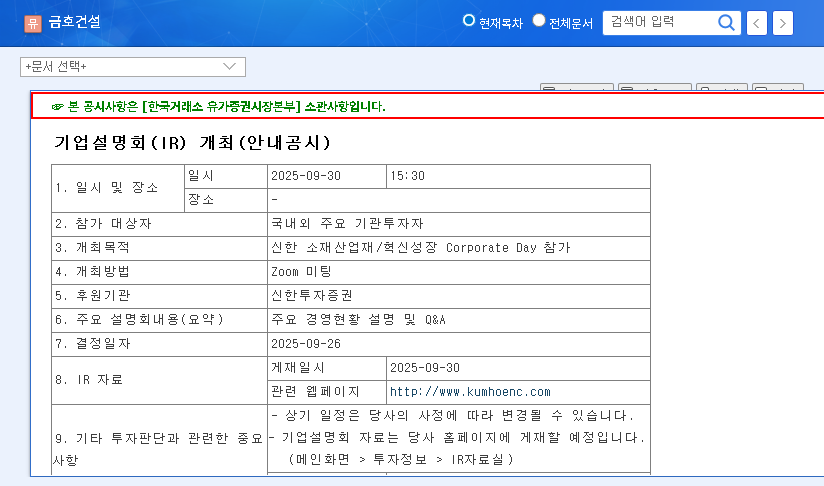

The upcoming KUMHO Engineering & Construction IR event, scheduled for November 14, 2025, at 2:00 PM, is a critical moment for the company and its investors. As KUMHO E&C prepares to present its Q3 2025 earnings, the construction market is fraught with uncertainty, and internal financial metrics raise serious questions. This event represents a pivotal opportunity for management to restore confidence and outline a clear path forward.

This comprehensive analysis will delve into KUMHO E&C’s fundamentals, dissect the macroeconomic headwinds, and provide a detailed investment strategy. Can the company navigate these turbulent waters and emerge stronger, or are the risks too significant for the prudent investor? Let’s explore the key factors that will shape the company’s future.

Analyzing KUMHO E&C Fundamentals: A Look Under the Hood

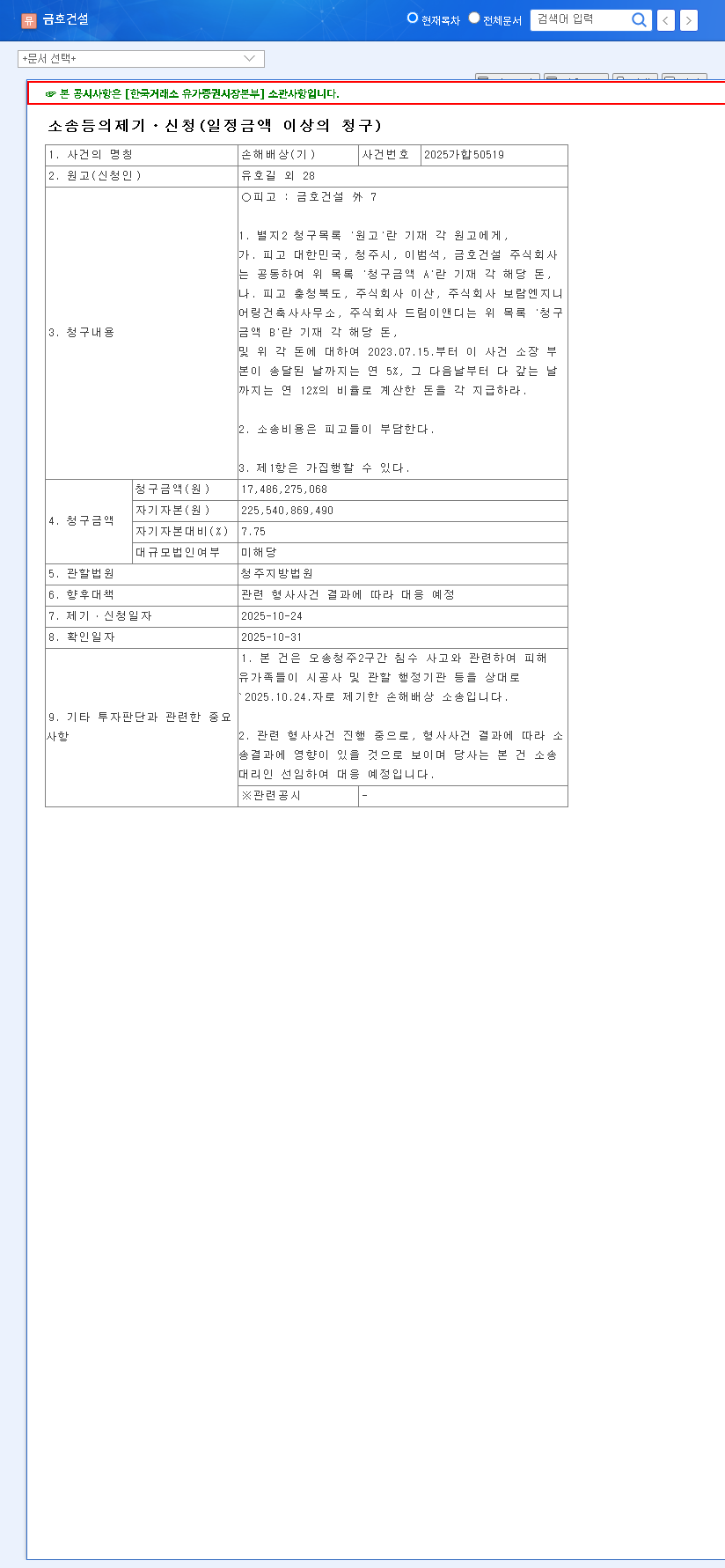

Before evaluating the potential outcomes of the Q3 2025 earnings call, it’s essential to understand the company’s current financial standing. Recent amendments to its business reports provide a mixed but revealing picture.

A Push for Transparency Amidst Financial Strain

In its December 2024 business report amendment, KUMHO E&C took steps to improve information transparency. By providing granular details on sales and supply contracts—including counterparties, terms, and contract amounts for major projects like the Gumi and Gongju Natural Gas Power Plants—the company aimed to reduce information asymmetry. As detailed in their Official Disclosure on DART, this move is a positive step toward rebuilding investor trust. However, transparency alone cannot solve underlying issues.

Despite commendable efforts in transparency, the core challenge remains: the company’s shift to a consolidated operating loss and a worrying decrease in total equity. These financial headwinds are significant risk factors that the upcoming KUMHO Engineering & Construction IR must address directly.

The Lingering Financial Health Concerns

The transition to an operating loss signals that core business activities are not generating profit, a major red flag for investors. This, coupled with declining equity, suggests that the company’s net worth is eroding. The upcoming earnings report will be scrutinized for any signs of a turnaround, specifically in operating profit margins and debt management strategies. The challenging construction market, marked by high costs and real estate project financing (PF) risks, makes a swift recovery difficult.

Macroeconomic Headwinds: A Perfect Storm?

No company operates in a vacuum, and KUMHO E&C is particularly susceptible to external economic pressures. The current environment presents a complex web of challenges that directly impact profitability and project viability.

- •Currency and Interest Rate Pressure: A persistent KRW/USD exchange rate in the high 1,400s increases the cost of imported raw materials and equipment. Simultaneously, rising interest rates in both South Korea and the U.S. elevate financing costs for new projects and existing debt, squeezing margins from both ends.

- •Inflated Input Costs: Global commodity markets, as tracked by sources like Bloomberg, show volatile prices for key materials. Elevated oil prices and shipping indices (like the Baltic Dry Index) translate directly to higher logistics and raw material expenses, further eroding project profitability.

- •Domestic Market Slump: The South Korean construction market is experiencing a significant downturn. High-profile real estate PF defaults, soaring construction costs, and reduced government spending on social overhead capital (SOC) projects have led to fewer new orders and intensified competition for the available work.

An Actionable KUMHO E&C Investment Strategy

Given the complex environment, a sound KUMHO E&C investment strategy requires careful analysis of the information presented at the IR event. Investors should move beyond headlines and focus on specific, measurable indicators.

Key Metrics to Watch in the Q3 2025 Report

During the IR presentation, pay close attention to these critical financial health indicators:

- •Operating Profit Margin: Is it improving, stagnating, or worsening? This is the primary indicator of core business health.

- •Order Backlog & New Orders: A healthy backlog provides revenue visibility, but a decline in new orders signals future weakness.

- •Debt-to-Equity Ratio & Accounts Receivable: Scrutinize the balance sheet. Is debt manageable? Are they collecting payments from clients in a timely manner?

- •Management’s Forward Guidance: Listen carefully to the vision for 2026. Are their plans for profitability and growth realistic, or overly optimistic?

Conclusion: A Cautious but Watchful Approach

The KUMHO Engineering & Construction IR event is a double-edged sword. A transparent presentation of poor results could send the stock tumbling. Conversely, a clear, credible strategy for navigating the market and restoring financial health could be a powerful catalyst for a recovery.

For investors, the prudent approach is to remain on the sidelines until after the IR event. A decision to invest should only be made after meticulously analyzing the Q3 results against the backdrop of the broader industry trends discussed in our Guide to the Korean Construction Sector. The company’s ability to execute its future plans and manage its significant financial risks will be the ultimate determinant of long-term value.