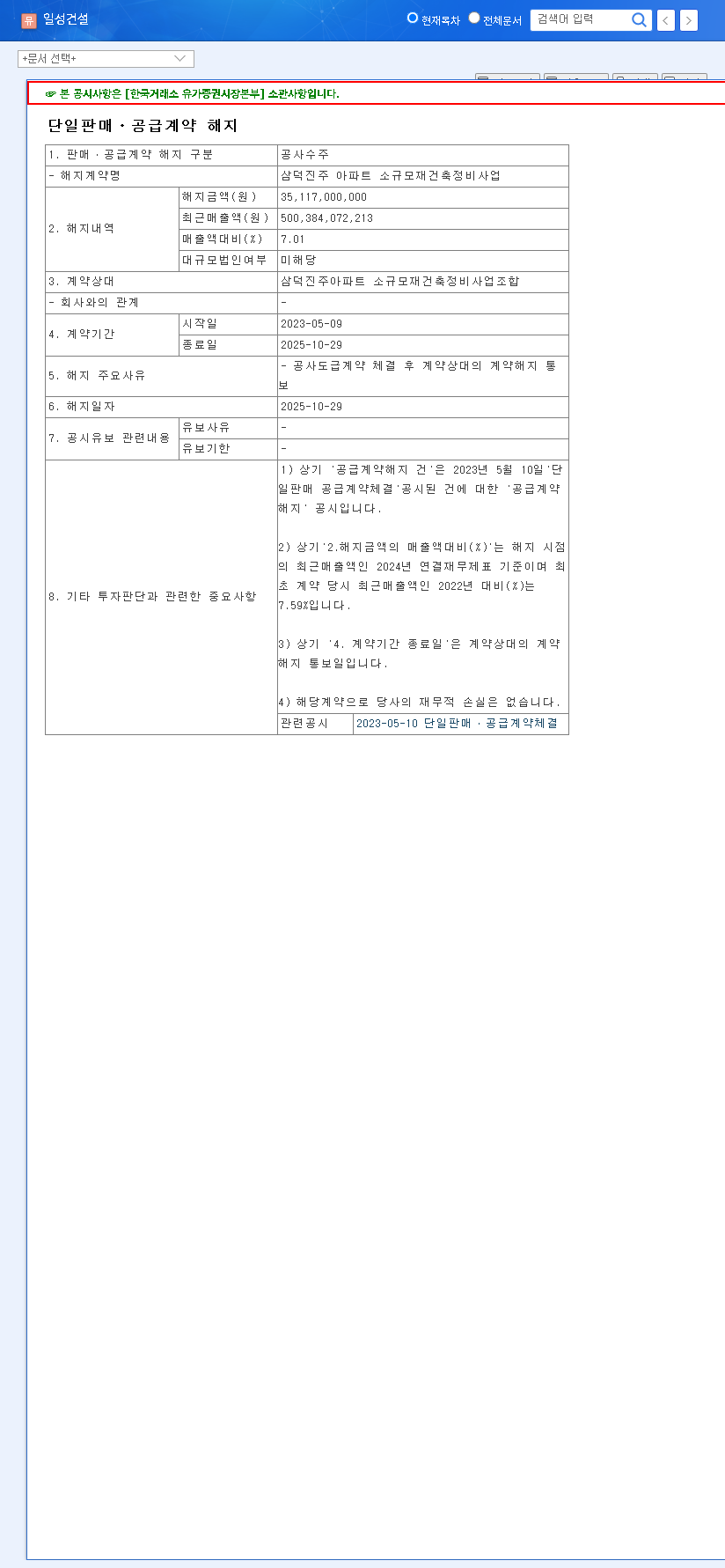

Amid a turbulent market for the construction sector, ILSUNG CONSTRUCTION CO.,LTD (013360) has announced a significant contract win, raising questions among investors. The company secured a ₩26.2 billion project with the Armed Forces Financial Management Group, a development that brings a glimmer of hope. However, does this contract signal a genuine turnaround for a company grappling with deep-seated financial issues, or is it merely a temporary reprieve? This comprehensive analysis examines the contract’s details, dives deep into the underlying fundamentals of ILSUNG CONSTRUCTION CO.,LTD, and provides a clear investment outlook to navigate the uncertainty.

While the new contract is a welcome development, it represents just 5.22% of recent half-year revenue, highlighting the immense challenge ahead in resolving the company’s fundamental weaknesses.

Contract Details: A Closer Look at the ₩26.2 Billion Deal

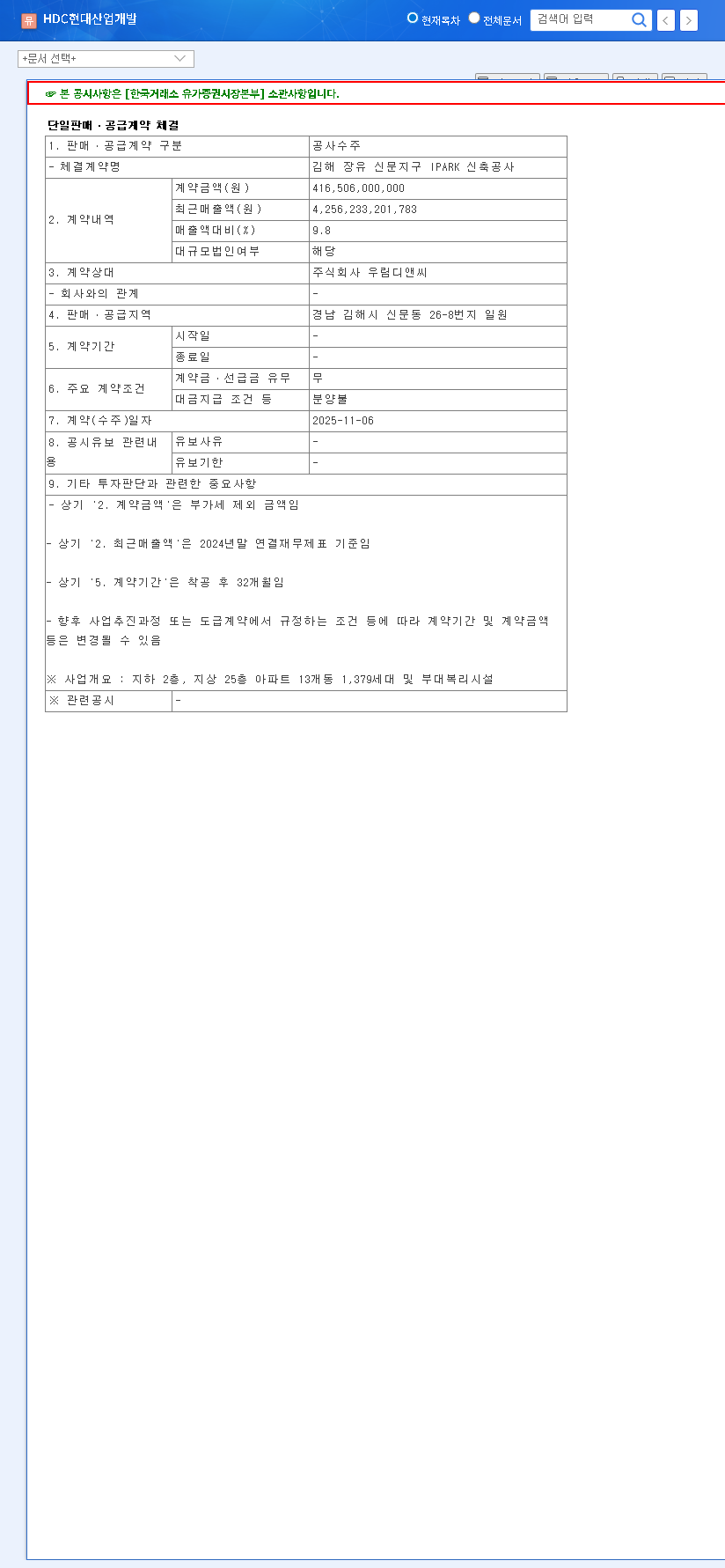

On November 12, 2025, ILSUNG CONSTRUCTION CO.,LTD officially announced the signing of a major public works contract. The project, located in Danyang-gun, Chungcheongbuk-do, involves construction for the Armed Forces Financial Management Group. The details, as per the Official Disclosure (DART), are as follows:

- •Contract Value: ₩26.2 billion KRW.

- •Contract Period: November 12, 2025, to April 22, 2027 (approx. 17 months).

- •Relative Scale: This amount represents 5.22% of the company’s 2025 half-year consolidated revenue of ₩229.23 billion.

Securing a stable public sector contract offers some stability and is expected to contribute positively to revenue streams over the next year and a half. However, a thorough ILSUNG CONSTRUCTION analysis reveals that this win must be viewed within the context of the company’s precarious financial health.

Deep Dive: Persistent Financial Headwinds

The positive news of the contract does little to mask the significant underlying risks detailed in the company’s 2025 half-year report. These issues paint a picture of a company struggling with its core operations and financial structure.

Revenue Collapse and Profitability Concerns

The most alarming indicator is a severe decline in revenue, which plummeted by 54.1% year-on-year to ₩229.23 billion in the first half of 2025. While the company reported an operating profit of ₩6.776 billion, this figure is misleading. It was primarily driven by one-off gains from the disposal of investment properties, not by an improvement in the core construction business. This reliance on non-recurring income suggests that the fundamental weakness in its main operations persists.

Deteriorating Financial Health and Debt Burden

The company’s balance sheet is also under pressure. Total debt increased by 5.5% from the end of the previous year, with a notable rise in short-term borrowings. This indicates mounting pressure to meet immediate financial obligations. Furthermore, the credit rating for ILSUNG CONSTRUCTION CO.,LTD remains at BB0, a speculative grade that signals significant financial risk to credit agencies and investors. You can learn more about how to interpret these risks in our guide on analyzing corporate financial health.

Investment Outlook: A ‘Neutral’ Stance with High Caution

Given the evidence, the ₩26.2 billion contract is insufficient to alter the company’s trajectory fundamentally. Its impact is too limited to offset the sharp revenue decline, improve the debt-laden financial structure, or secure long-term growth. The broader macroeconomic environment, characterized by high interest rates and a slowdown in the global construction market, presents further challenges that this single contract cannot overcome.

Our investment opinion for the ILSUNG CONSTRUCTION stock (013360) is Neutral. The short-term positive sentiment from the news is unlikely to translate into a sustained stock price increase without tangible improvements in the company’s core business.

Key Monitoring Points for Investors

Long-term investment attractiveness will only materialize if the company demonstrates meaningful change. Investors should closely monitor the following developments:

- •Consistent Order Flow: Can the company secure additional, larger-scale contracts to rebuild its order backlog?

- •Financial Restructuring: Are there concrete efforts to reduce debt, improve liquidity, and move away from reliance on one-off asset sales?

- •Core Profitability: Is there a visible recovery in the profitability of core construction projects, independent of non-recurring gains?

- •Market Conditions: How is the company positioned to handle ongoing industry-wide pressures and changes in government infrastructure policy?

Until these fundamental issues are addressed, the recent contract should be seen as a small positive step on a long and challenging road to recovery for ILSUNG CONSTRUCTION CO.,LTD.