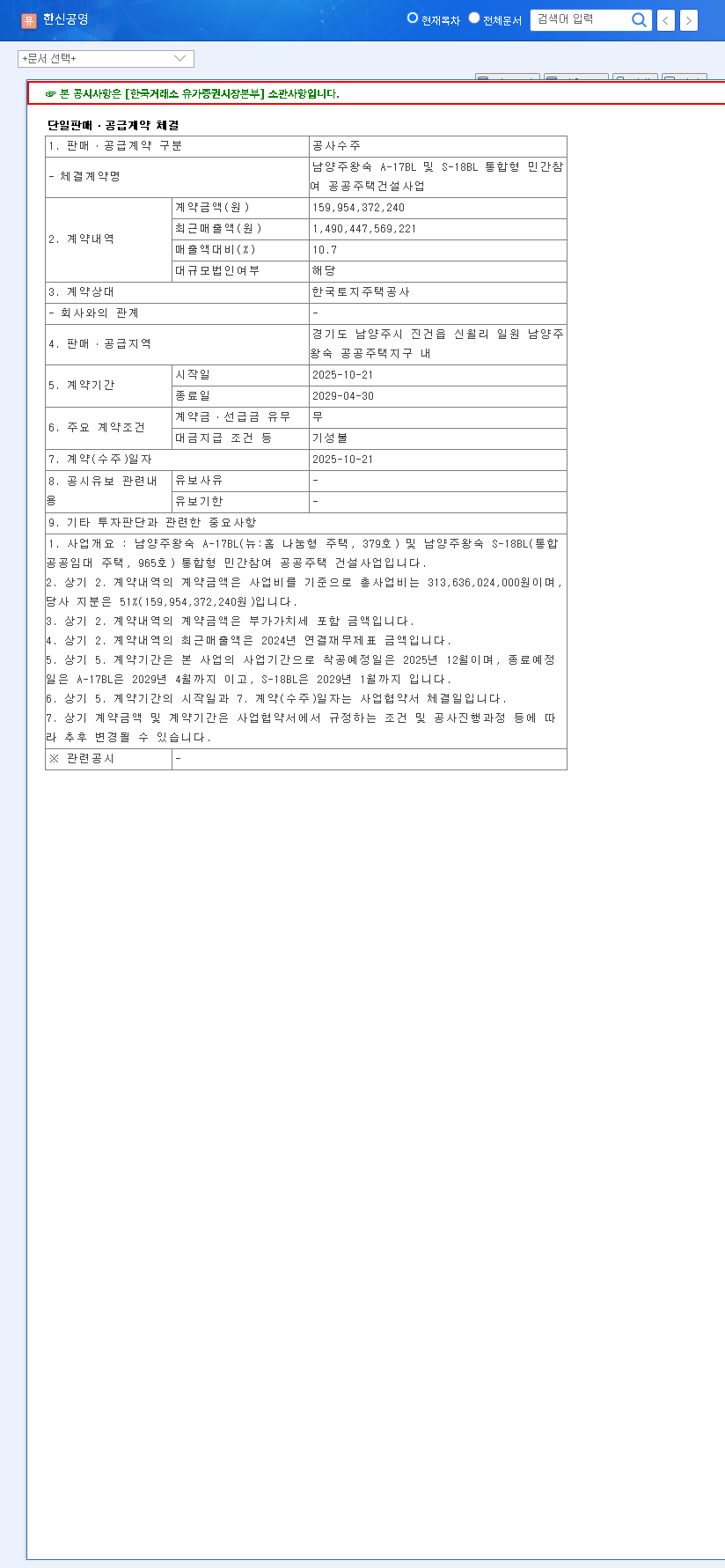

In a significant development for the South Korean construction sector, HANSHIN CONSTRUCTION CO., LTD. has officially secured a major ₩160 billion public housing construction contract with the Korea Land and Housing Corporation (LH). This pivotal agreement for the Namyangju Wangsuk Public Housing Project is set to bolster the company’s order backlog and provides a clear runway for future revenue. For investors, this news warrants a closer look at the company’s performance metrics and its potential stock outlook.

This comprehensive analysis will dissect the details of this large-scale construction contract, evaluate the multifaceted financial implications, and provide a balanced view of both the opportunities and risks involved. We will explore how this project could shape HANSHIN CONSTRUCTION’s trajectory in the coming years and what it means for stakeholders.

A Landmark Deal: The ₩160 Billion Namyangju Wangsuk Project

On October 21, 2025, HANSHIN CONSTRUCTION formally announced the contract for the ‘Namyangju Wangsuk A-17BL & S-18BL Integrated Private Participation Public Housing Construction Project’. This is not just another project; its scale, representing 10.7% of the company’s recent annual revenue, marks it as a cornerstone for future stability. The details, confirmed in the company’s Official Disclosure, paint a clear picture of its significance.

Key Contract Specifications

- •Client: Korea Land and Housing Corporation (LH), the nation’s premier public housing provider, adding a layer of credibility and payment security.

- •Total Value: ₩160 billion, a substantial sum that will be recognized as revenue over the project’s lifecycle.

- •Project Type: A ‘Private Participation Public Housing Project’, which blends private sector efficiency with public sector objectives, a model gaining traction for large-scale urban development.

- •Duration: A long-term engagement from October 2025 to April 2029, providing excellent revenue visibility for nearly four years.

Financial Impact and Stock Outlook for HANSHIN CONSTRUCTION

This major order is poised to create ripples across HANSHIN CONSTRUCTION’s financial statements and influence its market valuation. A balanced analysis requires examining both the positive catalysts and the potential headwinds.

Bullish Case: Catalysts for Growth and Stability

The direct benefit is a fortified revenue stream. This long-term construction contract provides a predictable source of income, shielding the company from short-term market volatility. Furthermore, successfully executing a high-profile project for LH enhances HANSHIN CONSTRUCTION’s reputation, potentially opening doors to future public-private partnerships and solidifying its position as a reliable industry leader. This improved business stability is a key factor that can positively influence its stock outlook.

Bearish Case: Potential Risks and Headwinds

While the top-line benefits are clear, prudent investors must consider the risks to profitability. The most significant threat is the volatility of raw material prices. Over a multi-year construction period, unforeseen spikes in the cost of steel, cement, and other essential materials could erode profit margins. Additionally, the construction industry is susceptible to delays from regulatory hurdles, labor disputes, or supply chain disruptions, which can lead to costly overruns.

“Securing a large government contract is a clear positive for HANSHIN CONSTRUCTION’s revenue pipeline. However, the market will be keenly watching their ability to manage costs and protect margins in the face of macroeconomic uncertainty and inflation.”

Broader Market Context and Strategic Positioning

The South Korean government continues to prioritize the development of public housing to stabilize the real estate market and provide affordable living options. This policy focus creates a favorable environment for construction firms with proven track records in public projects. By winning the Namyangju Wangsuk Public Housing Project, HANSHIN CONSTRUCTION demonstrates its competitiveness in this key market segment. For more on sector-wide trends, investors may find it useful to review reports on the South Korean construction industry outlook. This win positions the company favorably against competitors and highlights its expertise in navigating complex, large-scale developments.

Frequently Asked Questions (FAQ)

Q1: What is the core nature of this HANSHIN CONSTRUCTION contract?

A1: It is a ₩160 billion agreement with the Korea Land and Housing Corporation (LH) to build the Namyangju Wangsuk Public Housing Project, a significant undertaking that makes up over 10% of the company’s recent yearly revenue.

Q2: How will this impact HANSHIN CONSTRUCTION’s revenue?

A2: The contract is expected to provide a stable and predictable revenue stream for approximately 3.5 years, contributing directly to long-term performance growth and financial stability.

Q3: What are the primary risk factors for this project?

A3: The key risks include rising raw material costs, potential construction delays leading to cost overruns, intense market competition, and broader housing market volatility influenced by economic factors like interest rates.

Q4: What should investors research further?

A4: For a complete picture, investors should analyze recent brokerage reports, review the company’s financial health (e.g., debt levels, cash flow), and monitor macroeconomic trends affecting the housing market. Authoritative sources like the Bank of Korea’s economic outlook can provide valuable context.