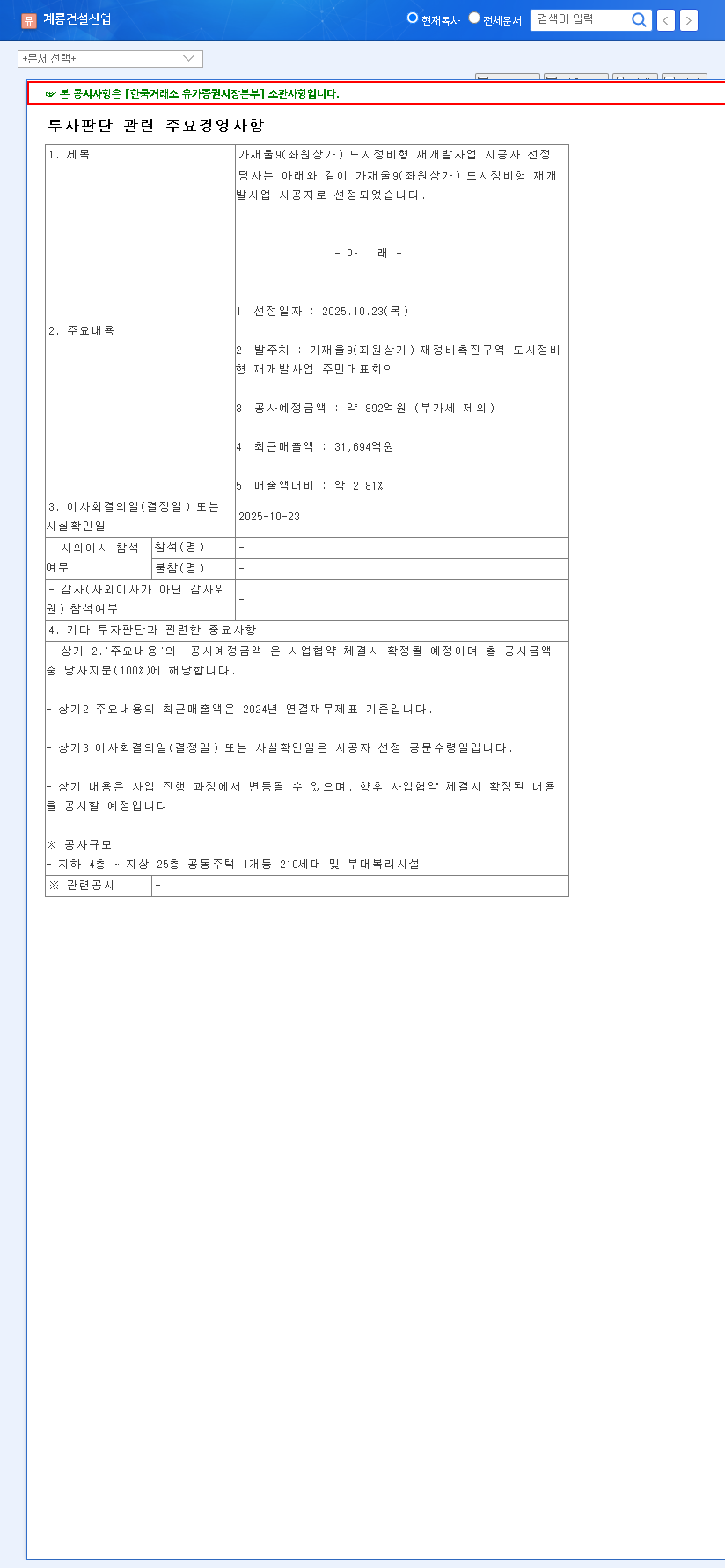

The recent announcement that HANSHIN CONSTRUCTION CO.,LTD (004960) has won the contract for the Sihung 1-dong 859 Redevelopment Project has stirred significant interest among investors. Valued at approximately ₩76.7 billion, this project represents a notable 5.1% of the company’s recent sales revenue. While any major contract win is positive news, savvy investors are asking the critical question: Is this a true catalyst for growth, or just a temporary headline? This detailed HANSHIN CONSTRUCTION stock analysis will dissect the project’s impact, evaluate the company’s precarious financial health, and provide a comprehensive outlook for potential investors.

We will explore whether this achievement can pave the way for a turnaround, considering the broader challenges in the construction market and the company’s fundamental weaknesses. If you’re looking to make an informed decision about HANSHIN CONSTRUCTION CO.,LTD (004960), this analysis provides the essential data and context you need.

Project Deep Dive: The Sihung 1-dong Contract

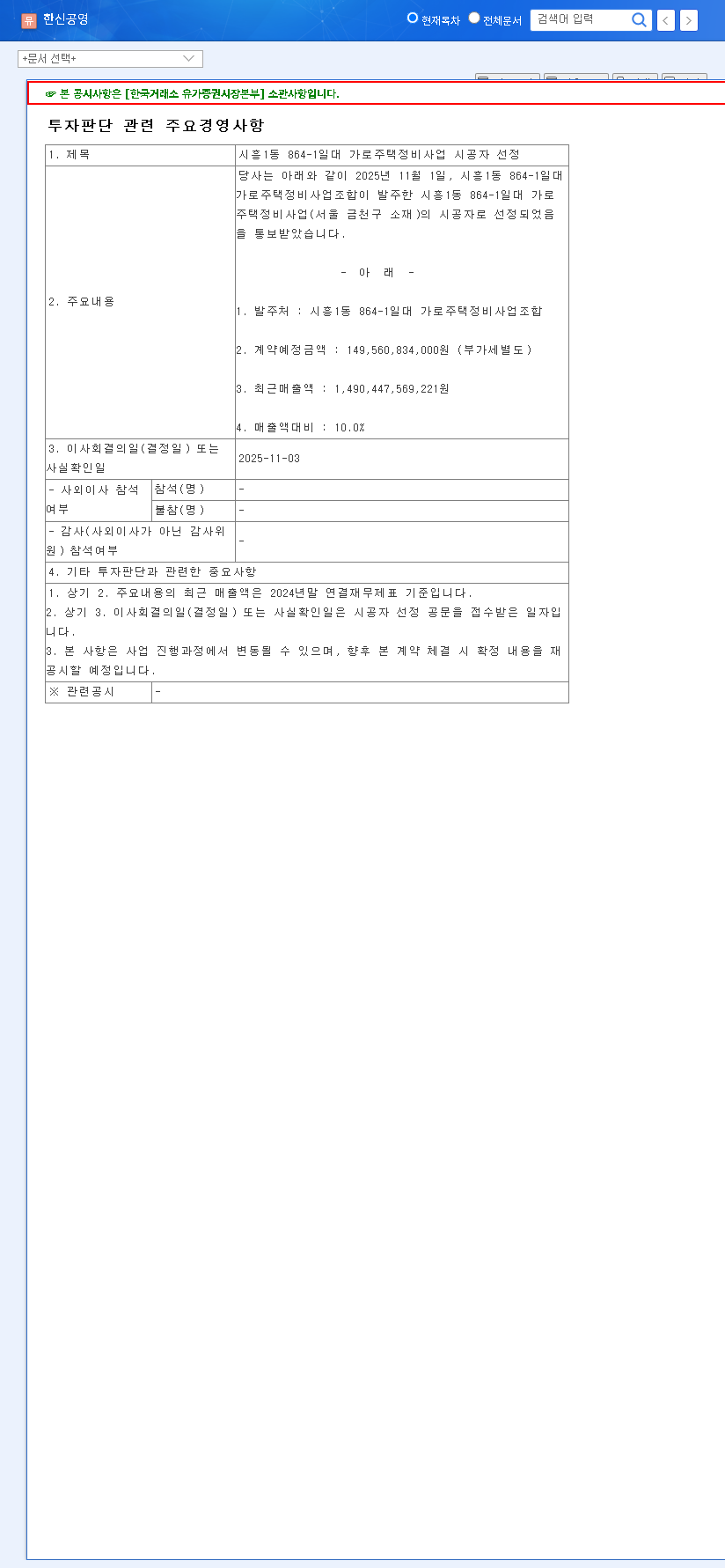

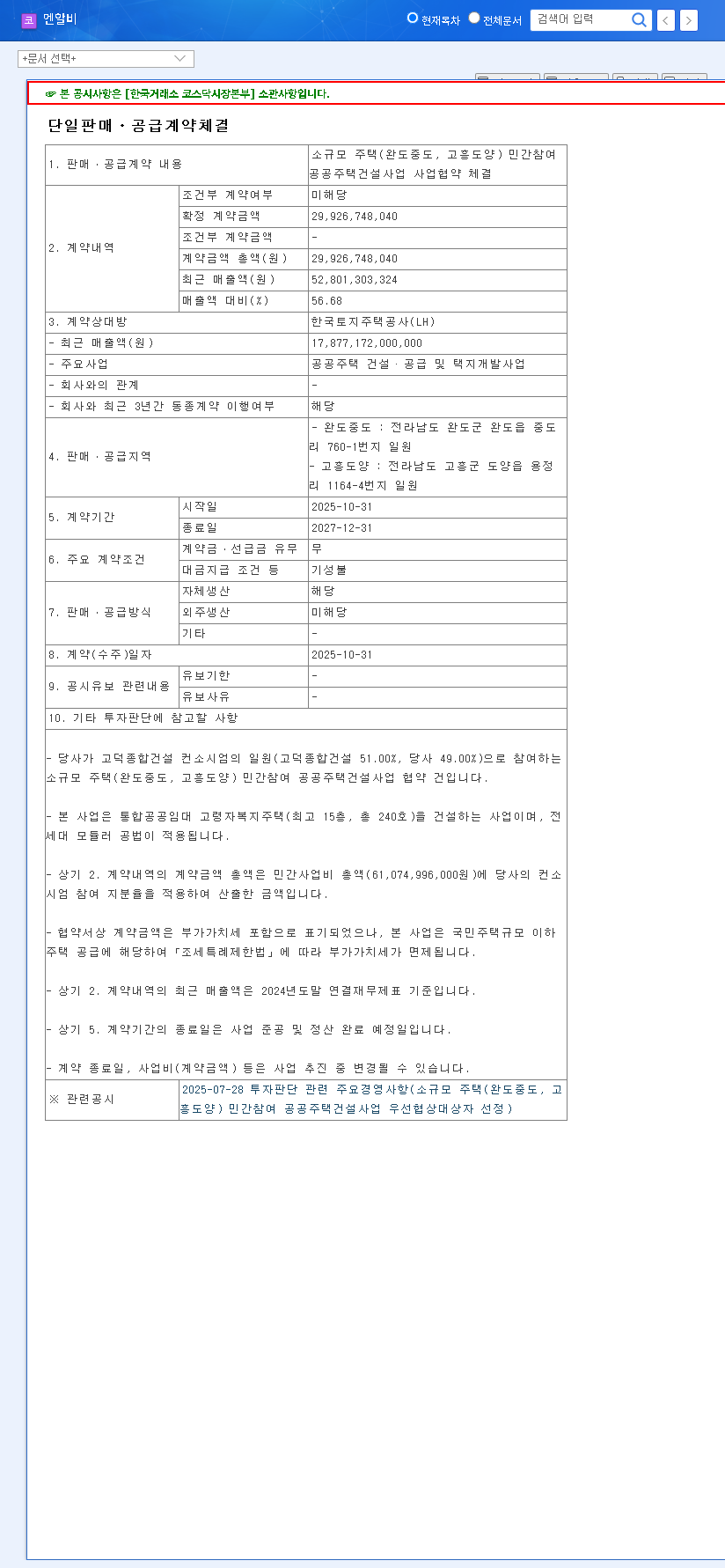

On November 1, 2025, HANSHIN CONSTRUCTION officially secured its role as the primary contractor for the Sihung 1-dong project. According to the Official Disclosure on DART, the contract is valued at ₩76.7 billion. While this figure is significant, its true importance lies in its strategic implications.

Strategic Significance Beyond the Numbers

This isn’t just another entry in the order book. Winning a competitive redevelopment bid in the Seoul metropolitan area, near Geumcheon-gu, offers several key advantages:

- •Enhanced Competitiveness: A successful project in a high-profile urban area serves as a powerful reference, boosting the company’s reputation and improving its chances of winning similar, lucrative contracts in the future.

- •Stable Revenue Stream: In a volatile market, this multi-year project provides a predictable revenue stream, contributing to top-line growth and helping to offset the company’s currently low order backlog.

- •Improved Investor Confidence: The recent business report amendment, which clarified contract details, coupled with this win, enhances transparency and may help rebuild trust with investors who have been wary of the company’s financial state.

Financial Health: A Cautious Outlook for HANSHIN CONSTRUCTION

Despite the positive news, a thorough HANSHIN CONSTRUCTION stock analysis must confront the company’s challenging financial situation. The ₩76.7 billion contract, while helpful, is not a magic bullet for the underlying issues. The company’s fundamentals reveal several red flags that require careful consideration.

The contract’s immediate impact on the overall financial structure is limited. Given the company’s low profitability and high debt ratio, meticulous management of this project’s profitability is absolutely critical to its long-term success.

Key Financial Metrics (2022-2023)

- •Profitability Collapse: Revenue and operating profit saw a marked decline from 2022 to 2023. More alarmingly, Return on Equity (ROE) plummeted from 19.11% to just 6.04%, indicating a sharp drop in its ability to generate profit from shareholder equity.

- •High Leverage: The Debt-to-Equity ratio remains stubbornly high at 271% in 2023. While projected to improve, this level of debt poses significant risks, especially if interest rates rise or project cash flows are delayed.

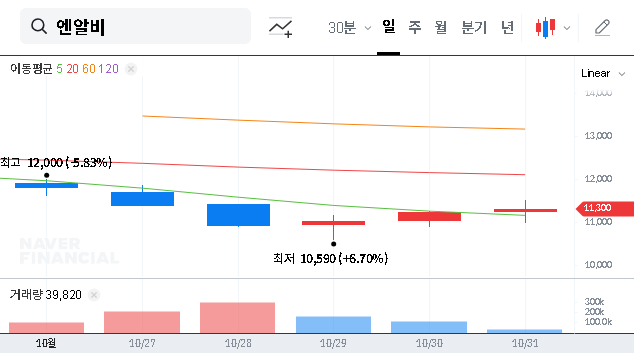

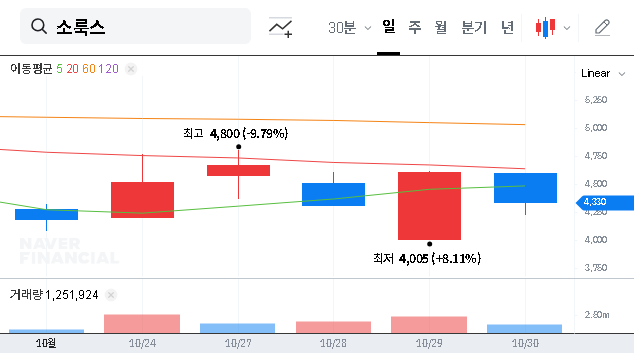

- •Valuation Concerns: While a Price-to-Book (PBR) ratio of 0.75x suggests the stock is undervalued relative to its assets, the Price-to-Earnings (PER) ratio of 39.83x in 2023 is high, reflecting poor earnings. Future PER projections show high volatility, signaling market uncertainty about future profitability.

Market Context and Investor Takeaway

The broader construction stock analysis reveals a tough environment. The South Korean construction market is grappling with high raw material costs and a potential slowdown in the housing sector. For a deeper look at global economic trends affecting this sector, sources like Reuters Business provide excellent macroeconomic data.

While stabilizing interest rates could ease borrowing pressures, HANSHIN’s high debt load remains a primary concern. The company’s future hinges on its ability to execute the Sihung 1-dong project with exceptional efficiency and cost control. Proving they can deliver this project profitably is paramount.

Investor Perspective: Key Points to Watch

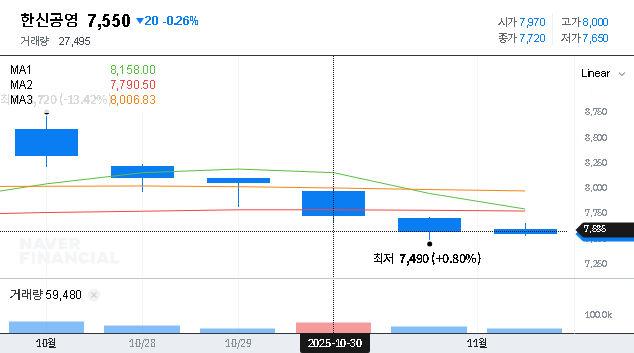

- •Short-Term Outlook: Do not expect a dramatic, immediate surge in the HANSHIN CONSTRUCTION stock price. The market will likely adopt a ‘wait-and-see’ approach, pending tangible results.

- •Mid-to-Long-Term Catalysts: The key drivers for future value will be the successful and profitable execution of the Sihung project, disciplined cost management, and the ability to secure a pipeline of similar new orders.

- •Monitor Profit Margins: Pay close attention to quarterly earnings reports for any improvement in operating and net profit margins. This will be the first concrete sign that the company is turning a corner.

In conclusion, the Sihung 1-dong project is a significant and positive step for HANSHIN CONSTRUCTION CO.,LTD (004960). It provides a much-needed potential boost to revenue and market reputation. However, it is an opportunity, not a guarantee. The company must navigate its weak financial position and a challenging market. For investors, this is a story of potential turnaround that requires patience and close monitoring of execution and profitability.