The latest KB STAR REIT investment of ₩19.3 billion has sent ripples through the investor community. While acquiring new assets often signals growth, this move comes at a time when KB STAR REIT’s financial foundations appear alarmingly unstable. This raises a critical question: is this a bold strategic maneuver to engineer a turnaround, or a risky gamble that could push the company over the edge?

This comprehensive analysis dissects the details of the new acquisition, scrutinizes the company’s precarious financial health, and evaluates the turbulent market conditions. We will provide investors with the critical insights needed to navigate this high-stakes situation and understand the true risks and potential rewards tied to the future of this prominent Korean REIT.

The ₩19.3 Billion Acquisition: What’s the Deal?

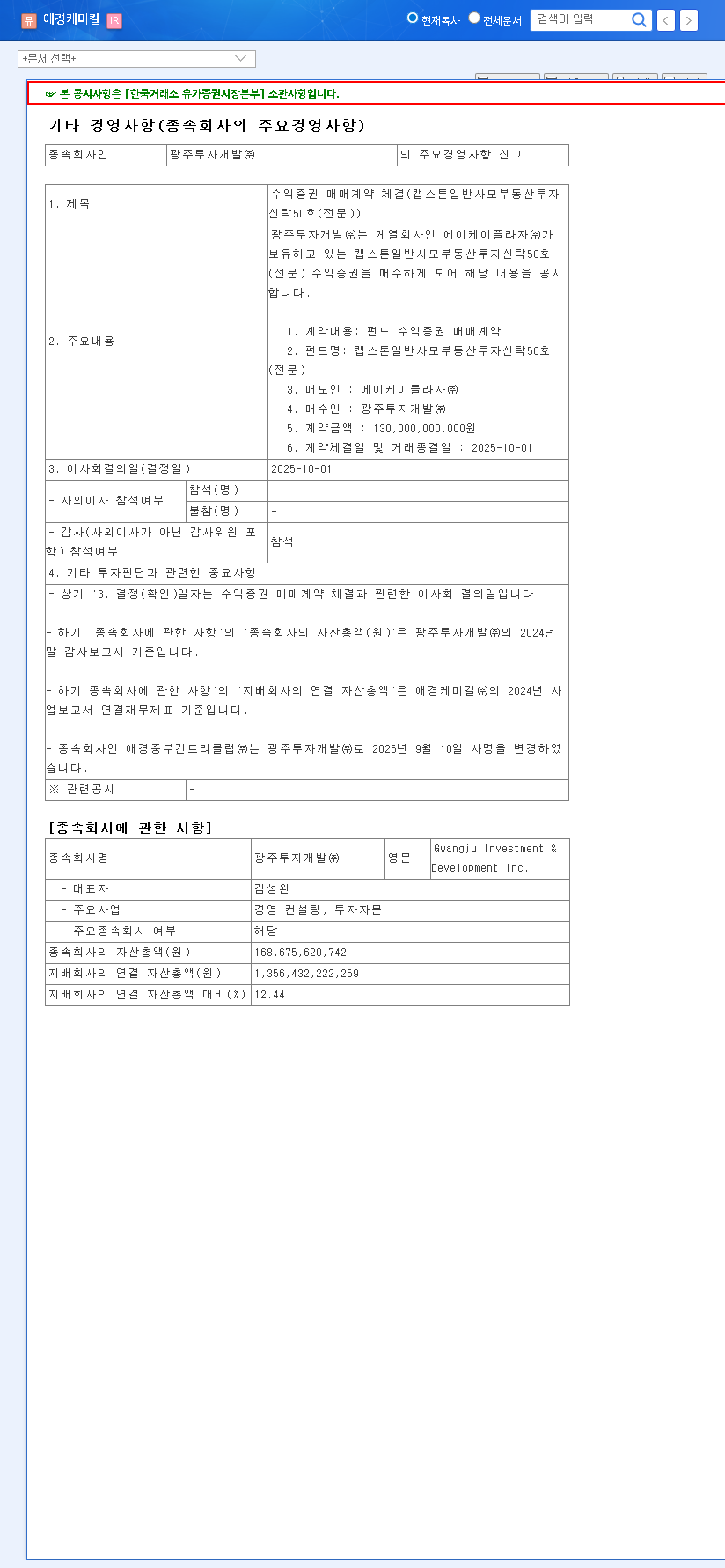

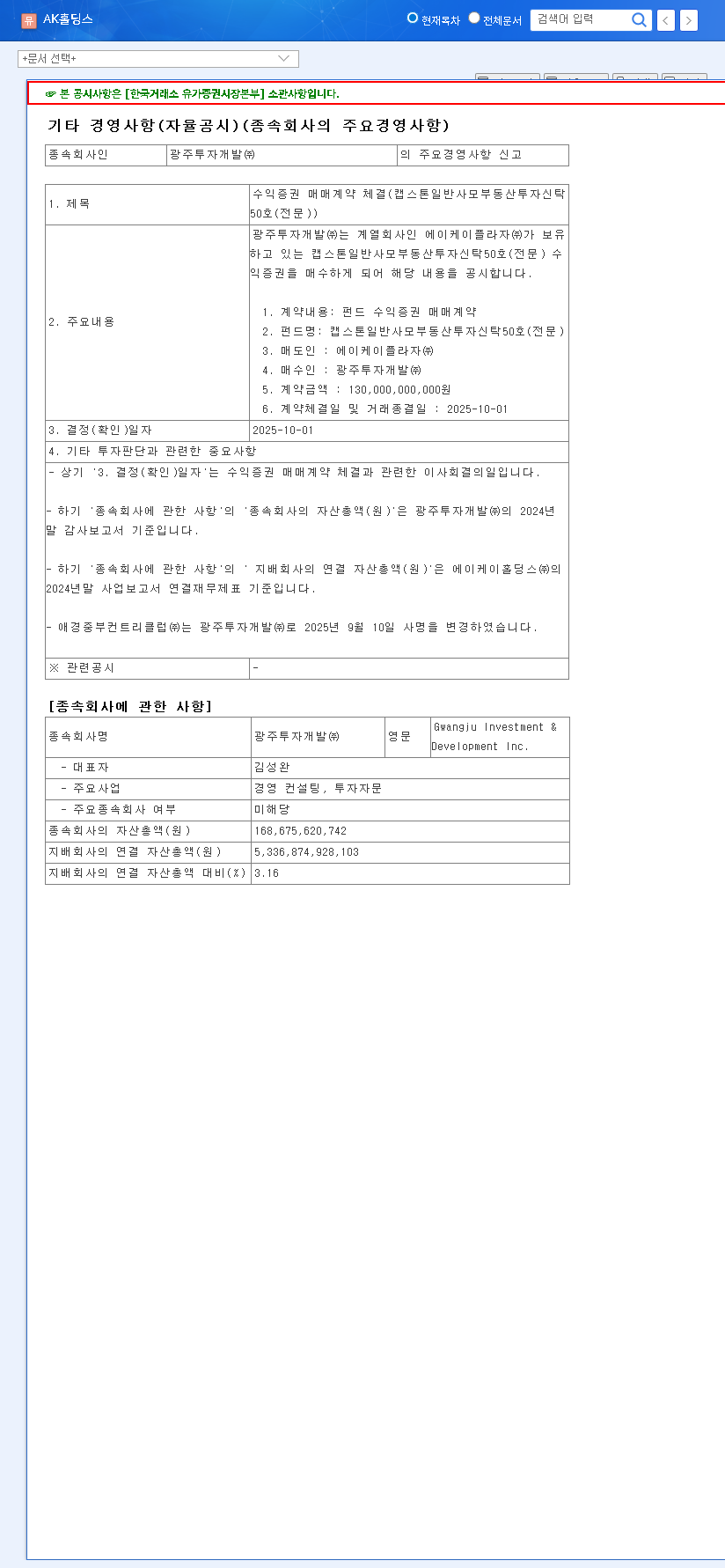

On November 10, 2025, KB STAR REIT officially announced its decision to acquire a 100% stake in KB Star Multi Asset REIT No. 1 Real Estate Investment Trust Co., Ltd. for ₩19.3 billion. This transaction, representing 7.34% of the company’s capital, is more than just a simple purchase. The funds are earmarked to facilitate a capital increase for the target company, which will then acquire beneficiary certificates of two Aegis General Private Real Estate Investment Trusts.

In essence, this is a multi-layered strategic investment aimed at portfolio diversification and the pursuit of new revenue streams. The full details of this transaction were made public in the company’s disclosure. (Official Disclosure: DART Report). Unfortunately, the market has been quiet, with a distinct lack of brokerage reports or analyst ratings, leaving investors to perform their own due diligence on this pivotal move.

Financial Health Under a Microscope: A House of Cards?

A detailed KB STAR REIT analysis reveals a company under immense financial pressure, making this large cash outlay particularly concerning. The numbers paint a grim picture of deteriorating fundamentals.

Alarming Financial Indicators

Historical data shows a catastrophic drop in operating profit from ₩23 billion in 2022 to just ₩6.5 billion in 2024. The latest business report from July 2025 is even more troubling, citing an operating loss of ₩72.4 billion and a staggering net loss of ₩99.4 billion. This was driven by significant impairment losses on investment properties.

The company’s total equity has shrunk to ₩262.8 billion, causing the debt-to-equity ratio to surge to an unsustainable 249.41%. This indicates that the company has far more debt than equity, signaling a high risk for investors and creditors.

Furthermore, the current ratio—a key measure of short-term liquidity—has plummeted from 73.12% to 37.91%. A ratio below 100% suggests a company may struggle to meet its short-term obligations, and a figure this low is a major red flag for liquidity risk.

Macroeconomic Headwinds: A Perfect Storm?

External market forces are compounding the company’s internal struggles. A deep dive into the REIT financial health cannot ignore these factors:

- •Exchange Rate Volatility: With significant Euro-denominated borrowings, the rising EUR/KRW exchange rate poses a massive threat. A mere 10% change could impact pre-tax net profit by an estimated ₩54.5 billion.

- •Sustained High Interest Rates: While central banks globally are navigating a complex landscape, borrowing costs remain elevated. As reported by sources like Bloomberg, high treasury yields in the US and Korea translate directly into higher financing costs for companies like KB STAR REIT, squeezing already thin margins.

- •Rising Operational Costs: Increasing commodity prices and freight indices hint at higher overall logistics and maintenance costs for real estate assets, further pressuring profitability.

Investor Playbook: Navigating the Uncertainty

Given the severe financial distress and opaque nature of the new assets, this KB STAR REIT investment demands extreme caution. The potential upside of portfolio expansion is heavily outweighed by the immediate and substantial risks.

For current and prospective investors, a clear-headed, proactive approach is essential. Simply hoping for the best is not a strategy. Consider the following actionable steps:

- •Demand Transparency: Urge the company to provide detailed information on the underlying assets of the new investment, including expected returns, vacancy rates, and risk assessments.

- •Scrutinize Liquidity Plans: Monitor company announcements for concrete plans on how they will manage the cash outflow and address the critical liquidity shortfall indicated by the current ratio.

- •Evaluate Hedging Strategies: Assess the company’s strategies for mitigating the severe risks posed by currency fluctuations and interest rate hikes. Are they adequately hedged?

- •Look for a Turnaround Blueprint: A new investment is not enough. The company must present a clear, credible, and comprehensive plan for improving its overall financial health. Without this, the new assets could just be dragging down an already sinking ship.

Ultimately, until KB STAR REIT can provide convincing evidence that this investment is part of a viable recovery strategy, investors should view it with significant skepticism. For more foundational knowledge, consider reviewing our guide on how to analyze a Real Estate Investment Trust.