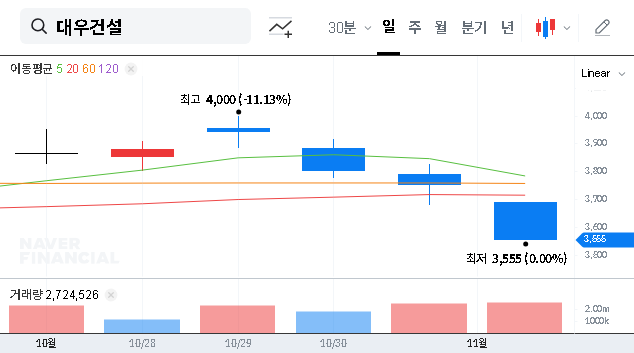

The recent announcement that DAEWOO ENGINEERING & CONSTRUCTION CO.,LTD (047040) has secured the massive DAEWOO E&C Sin-gil 10 urban redevelopment project has generated significant buzz among investors. This ₩322.9 billion contract, representing 3.07% of the company’s recent revenue, is a notable win. But beyond the headline number, what does this deal truly signify for Daewoo E&C’s corporate value and its stock price? Is this a catalyst for growth or simply a drop in the ocean of its existing order backlog?

This comprehensive investment analysis will dissect the Sin-gil 10 Redevelopment Project, exploring its strategic importance, financial implications, and potential risks. We’ll examine the contract in the context of Daewoo E&C’s broader fundamentals and the prevailing macroeconomic factors impacting the construction industry. For current shareholders and prospective investors, this deep dive provides the critical insights needed to navigate this development.

Dissecting the DAEWOO E&C Sin-gil 10 Contract Details

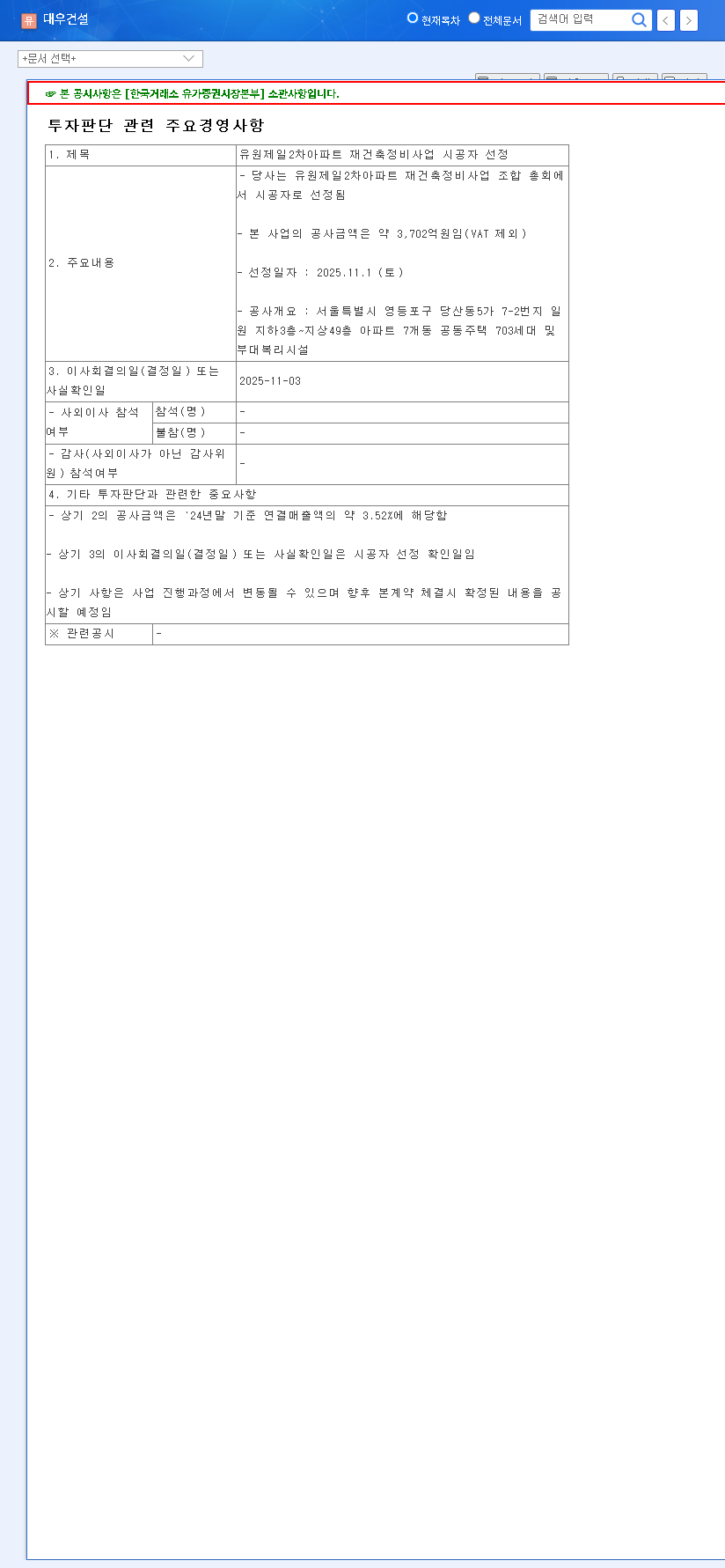

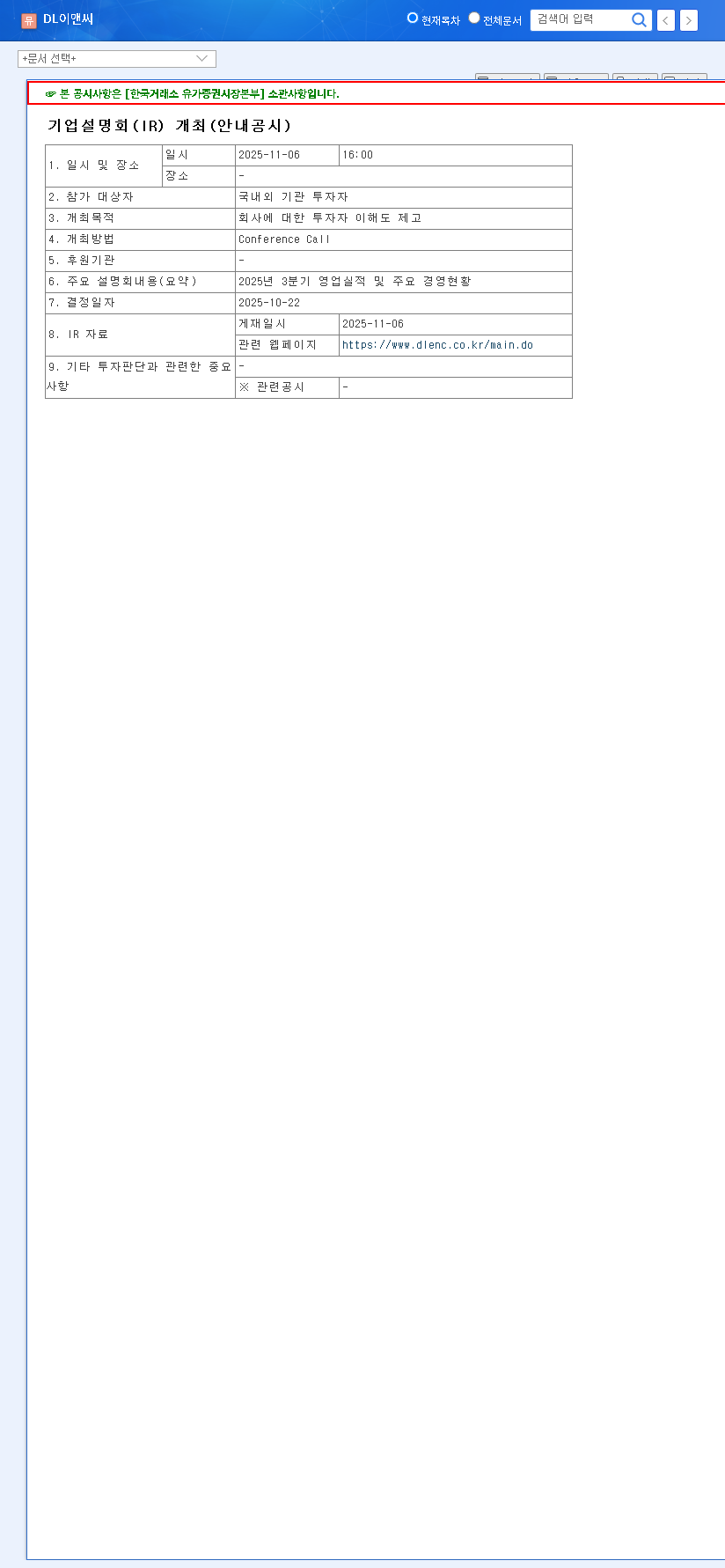

On November 14, 2025, Daewoo E&C officially announced the signing of a single sales and supply contract with Korea Trust Co., Ltd. for the Sin-gil 10 Urban Redevelopment Project. This project is a significant undertaking located in a prime residential area of Seoul, specifically around Sin-gil-dong in Yeongdeungpo-gu. The contract’s total value is confirmed at ₩322.9 billion. For full transparency, you can view the Official Disclosure (DART Report) here. This win reinforces the market’s confidence in Daewoo E&C’s ‘Prugio’ brand and its execution capabilities in the competitive domestic housing sector.

Key Contract Highlights:

- •Project Name: Sin-gil 10 Urban Redevelopment Project

- •Contract Value: ₩322.9 billion

- •Percentage of Revenue: 3.07% (based on recent annual revenue)

- •Counterparty: Korea Trust Co., Ltd.

- •Location: Sin-gil-dong, Yeongdeungpo-gu, Seoul

While this contract is a clear positive, it does not fundamentally alter the company’s overall investment thesis. It adds stability but doesn’t erase existing financial and market-related headwinds. A ‘Neutral’ stance remains prudent.

The Upside: Positive Implications for Daewoo E&C

Securing the DAEWOO E&C Sin-gil 10 contract provides several tangible benefits that investors should appreciate:

- •Enhanced Revenue Stability: Adding over ₩300 billion to the order backlog enhances future revenue visibility. In a cyclical industry like construction, a strong and stable backlog is a key indicator of near-term financial health and business sustainability.

- •Strengthened Market Position: Winning a competitive redevelopment project in Seoul, the heart of the Korean housing market, reinforces Daewoo E&C’s brand power and market leadership. It serves as a powerful testament to their expertise and reputation.

- •Balanced Portfolio Contribution: At 3.07% of revenue, the project is significant enough to be meaningful but not so large as to introduce excessive concentration risk. It diversifies the project pipeline without over-leveraging the company on a single outcome.

The Downside: Potential Risks and Investor Considerations

A thorough DAEWOO E&C investment analysis must also weigh the potential risks and uncertainties associated with this new contract.

Key Risks for the Sin-gil 10 Redevelopment Project:

- •Lack of Timelines: The official disclosure lacks specified start and end dates for the contract. This ambiguity makes it difficult for analysts to accurately forecast revenue recognition and cash flow timing, introducing a degree of uncertainty into financial models.

- •Housing Market Volatility: The Seoul real estate market is notoriously sensitive to government policy shifts, interest rate hikes, and fluctuating consumer sentiment. Unforeseen market downturns could impact project sales rates and profitability.

- •Margin Pressure: Rising costs of raw materials, labor shortages, and high financing costs due to elevated interest rates can squeeze profit margins on long-term projects like this. Effective cost management will be paramount.

Actionable Plan for Investors

While the DAEWOO E&C Sin-gil 10 contract is a positive development, it doesn’t change the broader investment picture overnight. We maintain a ‘Neutral’ outlook. For those invested or considering an investment in 047040 stock, here is a checklist for ongoing monitoring:

- •Monitor Project Updates: Watch for official announcements regarding the project’s timeline, sales commencement, and initial sales rates.

- •Analyze Quarterly Reports: Scrutinize Daewoo E&C’s quarterly earnings for improvements in the civil engineering sector and overall profit margin trends.

- •Track Financial Health: Keep an eye on the company’s debt-to-equity ratio and any strategic efforts to reduce its reliance on borrowings.

- •Follow Macro Trends: Stay informed about changes in interest rates, government housing policies, and raw material prices.

In conclusion, this contract win is a solid piece of execution that bolsters Daewoo E&C’s order book. However, it operates within a larger ecosystem of financial and market challenges that require careful and continuous monitoring. You can learn more by reading our complete analysis of the Korean construction sector.

Disclaimer: This analysis is for informational purposes only and is based on publicly available information. It does not constitute investment advice. All investment decisions should be made based on your own judgment and research.