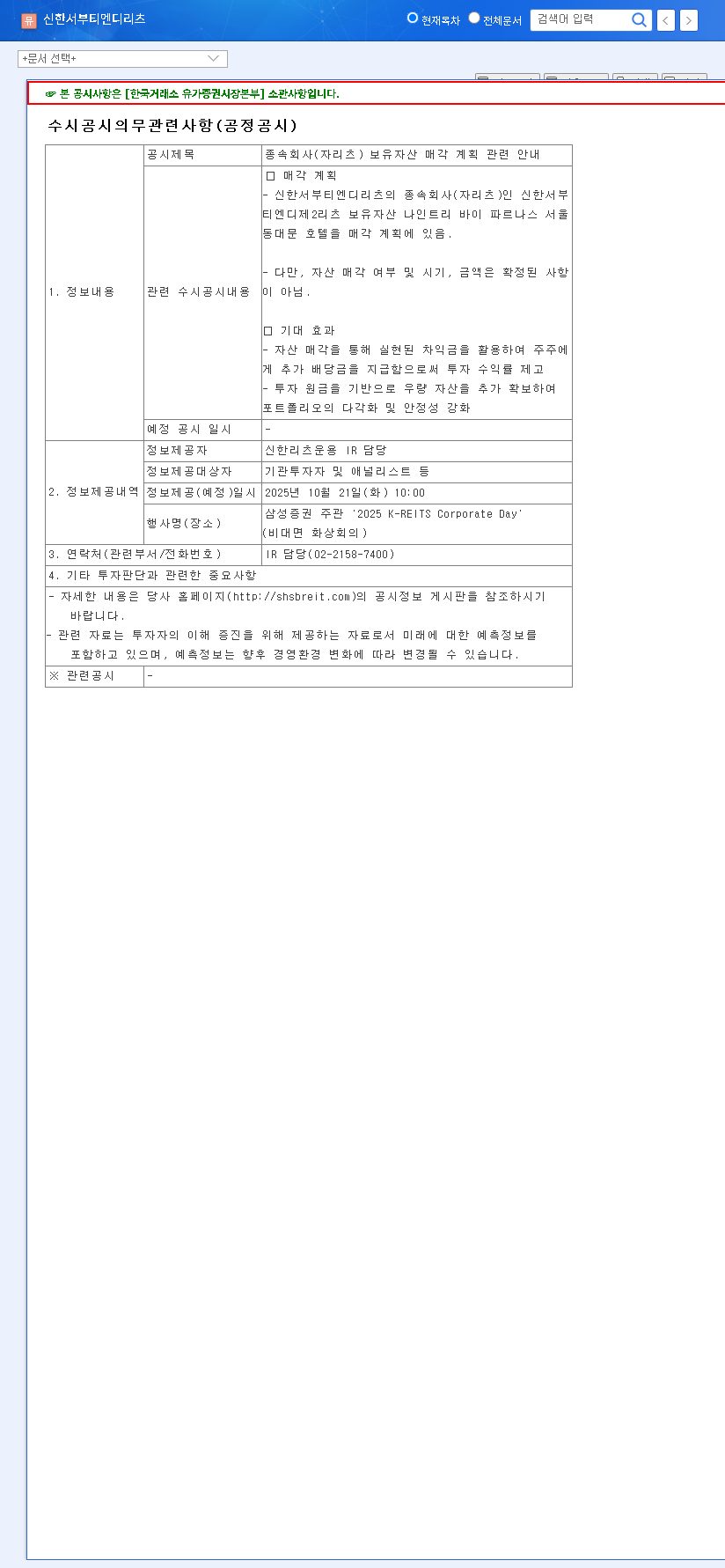

The release of the Shinhan Alpha REIT Q3 2025 report offers investors a critical window into the health and strategic direction of one of South Korea’s premier office REITs. In an investment landscape marked by economic uncertainty, Real Estate Investment Trusts (REITs) represent a compelling option for those seeking stable, income-generating assets. This report is more than a regulatory filing; it’s a detailed roadmap outlining asset growth, profitability trends, and the financial pressures shaping the company’s future. For anyone considering a position, a thorough Shinhan Alpha REIT analysis is essential for making an informed decision.

This deep dive will dissect the key findings from the Q3 report, contextualize them within the broader market, and provide an actionable framework for your REIT investment strategy. We’ll explore the balance between impressive portfolio expansion and the persistent headwinds of rising interest rates and operational costs.

Key Highlights from the Q3 2025 Financial Disclosure

On October 29, 2025, Shinhan Alpha REIT Co,. Ltd. published its quarterly performance data, a standard procedure for maintaining transparency with its stakeholders. While not an event that typically generates specific market forecasts, this disclosure provides the factual basis for assessing the company’s fundamental strength. The complete data was made public via the DART system. For those interested in the raw data, you can view the Official Disclosure (Source).

The core tension for investors is balancing Shinhan’s impressive portfolio growth against the rising tide of financial costs in a volatile interest rate environment. The Q3 report puts this dynamic into sharp focus.

Fundamental Analysis: Growth & Headwinds

Our Shinhan Alpha REIT analysis reveals a narrative of strategic expansion coupled with macroeconomic challenges. Here’s a breakdown of the critical areas detailed in the report.

1. Asset Portfolio Expansion and Quality

The REIT’s commitment to growth is evident. The successful integration of assets like the BNK Tower, noted in previous reports, continues to bolster the portfolio’s total value and rental income potential. As a leading Korean office REIT, maintaining a portfolio of prime, well-located properties is crucial.

- •Positive Signal: Steady growth in asset under management (AUM) contributes directly to higher potential operating revenue and long-term capital appreciation. Occupancy rates across core assets remain remarkably high, reflecting the quality of the properties.

- •Key Concern: Each acquisition brings additional debt. Investors must scrutinize the loan-to-value (LTV) ratio and the terms of new financing to ensure growth isn’t coming at the cost of excessive financial risk.

2. Profitability Under Pressure

While top-line revenue from rental income shows a healthy trajectory, the net profit tells a more complex story. The challenge highlighted in the semi-annual report—rising operating and financial costs—appears to persist. This is a critical factor for any dividend-focused REIT investment strategy.

- •Revenue Growth: Increased rental income from new assets and stable occupancy from existing ones are positive drivers.

- •Cost Challenges: The global interest rate environment directly impacts borrowing costs. The Q3 report should be carefully examined for details on interest coverage ratios and the management’s hedging strategies against rate volatility. Any increase in property management fees or other operational expenses will further squeeze margins. For more on this, see our Guide to Analyzing REIT Financials.

3. Financial Health and Debt Management

The balance sheet remains a primary focus. Key metrics from the semi-annual report, such as the debt ratio and retained earnings, serve as a baseline. The Q3 report provides an update on whether the REIT is strengthening its financial position or facing further deterioration. Investors should look for any management commentary on plans for refinancing upcoming debt maturities or potential capital raising initiatives.

Investor Action Plan: What to Do Now

The release of the Shinhan Alpha REIT Q3 2025 report is a call to action for current and prospective investors. A prudent approach involves a comprehensive evaluation of the data.

- •Validate the Thesis: For long-term holders, confirm that the core strengths—high-quality assets and strong occupancy—remain intact. The continued portfolio growth is a significant positive.

- •Monitor the Risks: Pay close attention to the trajectory of financial costs. If net profit continues to decline despite revenue growth, it could impact future dividend payouts, a cornerstone of REIT investing as explained by financial authorities like Investopedia.

- •Assess Market Reaction: Observe how the market digests this information. A muted or negative stock price reaction could indicate that concerns about profitability and debt outweigh the positive news of asset growth.

- •Look Ahead: Scour the report for management’s outlook. Any guidance on future acquisitions, divestments, or financing strategies provides invaluable insight into the company’s forward-looking plans.

Frequently Asked Questions (FAQ)

Q1: What is the main takeaway from the Shinhan Alpha REIT Q3 2025 Report?

The report confirms Shinhan Alpha REIT’s continued strategic growth in assets but also highlights the significant pressure on profitability from rising financial costs. It’s a mixed picture that requires careful analysis by investors.

Q2: Are there immediate red flags for investors in this report?

The primary area of caution is the trend of declining net profit margins. While not a red flag signifying immediate distress, it is a crucial trend to monitor as it could impact the sustainability of dividend growth if not addressed through cost management or improved financing terms.

Q3: How does Shinhan Alpha REIT compare to other Korean office REITs?

Shinhan Alpha REIT is known for its high-quality portfolio of prime office buildings and strong occupancy rates. However, like its peers, it is exposed to the same macroeconomic headwinds. A comparative analysis should focus on differences in debt structure, LTV ratios, and dividend yields.