The latest Hanwha Solutions Q3 earnings report for 2025 has sent a significant ripple through the market. On November 5, 2025, HANWHA SOLUTIONS CORPORATION announced preliminary results that didn’t just meet expectations—they shattered them. After consecutive quarters of operating losses, the company reported figures that brought it tantalizingly close to break-even, sparking intense investor interest. This detailed Hanwha Solutions analysis will explore the drivers behind this impressive turnaround, its impact on the company’s fundamentals, and what it could mean for the future of Hanwha Solutions stock.

The Q3 2025 Earnings Surprise: By the Numbers

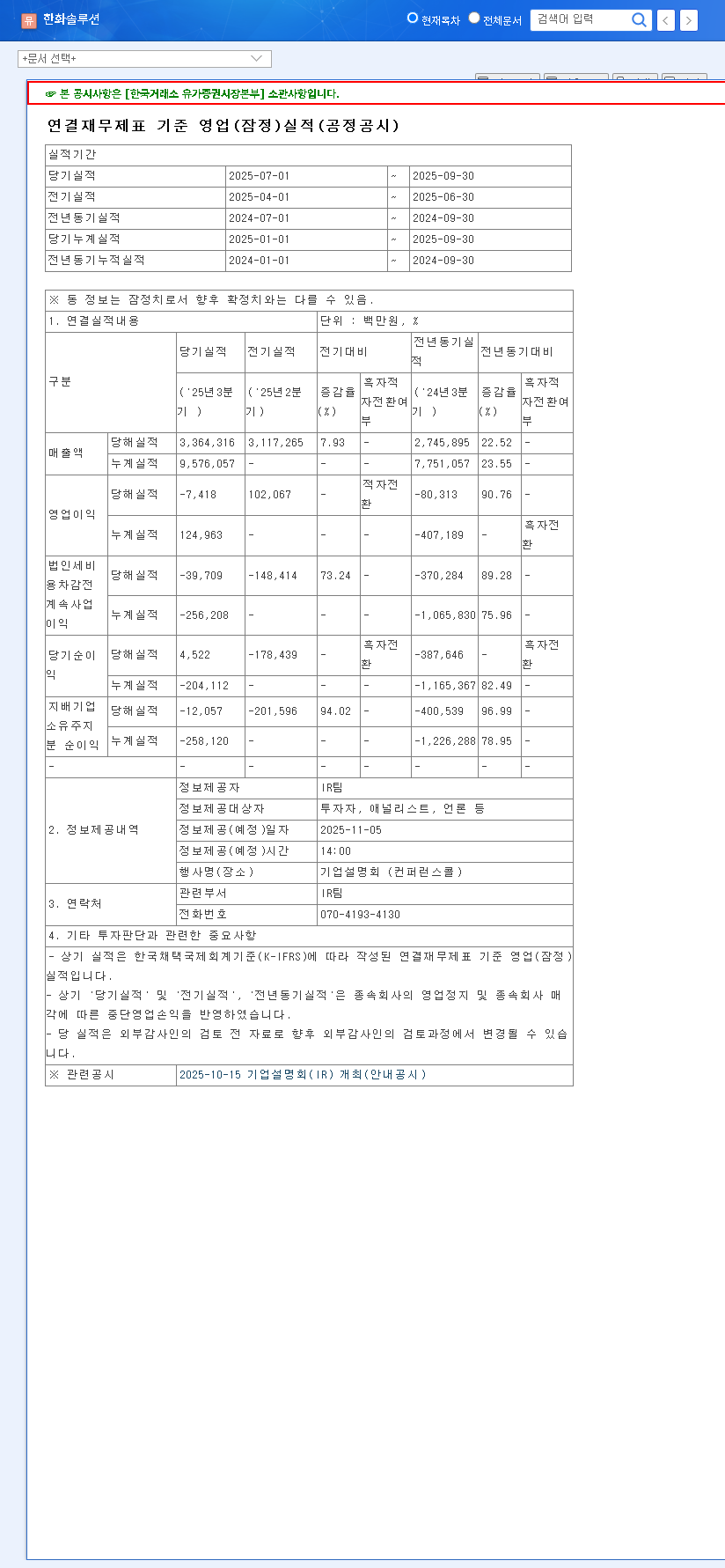

According to the company’s preliminary financial disclosure, the third-quarter performance signals a potential turning point. The figures, which can be verified in the Official Disclosure on DART, reveal a stark contrast to previous periods and market consensus.

- •Revenue: KRW 3,364.3 billion, a solid 4% above the market consensus of KRW 3,244.4 billion.

- •Operating Profit: KRW -7.4 billion. While still a loss, this marks a massive 95% improvement over the consensus forecast of a KRW -154.6 billion loss.

- •Net Profit: KRW -12.1 billion, representing a remarkable 96% improvement compared to the market’s expected loss of KRW -281.9 billion.

The key takeaway is not just the numbers themselves, but the velocity of the turnaround. A 95% improvement against consensus signals a potential fundamental shift in operational efficiency and market strategy for HANWHA SOLUTIONS CORPORATION.

What Fueled This Impressive Performance?

Several converging factors likely contributed to this better-than-expected outcome. It wasn’t a single silver bullet but a combination of strategic execution, operational tightening, and favorable market shifts.

1. Strength in the Renewable Energy Division (Hanwha Q Cells)

A significant driver is believed to be the strengthened competitiveness of its renewable energy arm, Hanwha Q Cells. Increased global demand for high-efficiency solar modules, particularly in key markets like the United States and Europe, likely boosted both sales volume and profit margins. This success suggests that the company’s investments in advanced solar technology are paying off, allowing it to capture a larger share of the high-value market segment. To learn more about this sector, you can read our Guide to Investing in Renewable Energy Stocks.

2. Aggressive Cost Reduction and Efficiency Gains

The dramatic reduction in operating loss points directly to successful company-wide initiatives focused on cost-cutting and enhancing production efficiency. This isn’t just about trimming expenses; it reflects a deeper operational discipline, optimizing supply chains, reducing waste, and improving yields in both their chemical and renewable energy manufacturing processes.

3. Resilience in the Basic Materials Segment

While the petrochemical and basic materials sector has faced global headwinds, Hanwha Solutions may have navigated these challenges more effectively than anticipated. Losses in this segment were likely smaller than feared due to stabilizing raw material costs and strategic portfolio management, preventing it from dragging down the consolidated results as heavily as in previous quarters.

Impact on Hanwha Solutions Stock and Investor Outlook

This earnings surprise is a powerful catalyst that could reshape investor sentiment and the valuation of Hanwha Solutions stock. The positive signals extend beyond a single quarter’s performance.

- •Restored Investor Confidence: Drastically outperforming expectations can restore faith in the management’s strategy and execution capabilities, potentially leading to a re-rating of the stock.

- •Improved Financial Health: Nearing break-even improves cash flow, strengthening the balance sheet and enhancing the company’s ability to manage debt and fund future growth investments.

- •Positive Forward Momentum: If this trend continues, it could signal the beginning of a sustained recovery, attracting long-term investors looking for growth and value. Macroeconomic factors, such as stabilizing interest rates as noted by sources like Bloomberg, could provide further tailwinds.

Frequently Asked Questions (FAQ)

What were the key highlights of the Hanwha Solutions Q3 earnings?

The main highlight was the near break-even operating profit of KRW -7.4 billion, which was a 95% improvement over pessimistic market forecasts. Revenue also beat consensus by 4%, showing resilient business activity.

Is this Q3 performance sustainable for HANWHA SOLUTIONS CORPORATION?

Sustainability will depend on continued strength in the Hanwha Q Cells division and the effectiveness of ongoing cost controls. Investors should watch for the detailed segment-by-segment breakdown in the full report to gauge the long-term potential of this recovery.

What should potential investors do now?

While this report is highly encouraging, prudent investors should conduct further due diligence. Key actions include analyzing the final, detailed earnings report, monitoring Q4 guidance from the company, and assessing the macroeconomic landscape. The market consensus will likely be revised upwards, which should also be factored into any investment thesis.

Disclaimer: This analysis is for informational purposes only and is based on preliminary data. Investment decisions should be made based on individual research and discretion.