This comprehensive HYUNGKUK F&B earnings analysis for Q3 2025 provides a deep dive into the company’s latest financial performance (KRX: 189980). Following the recent announcement, the market has shown a mixed response. While top-line figures like revenue and operating profit showed resilience, a noticeable dip in net income has raised important questions for investors. We will dissect the key growth drivers, analyze the pressing macroeconomic headwinds, and outline a strategic outlook for potential and current shareholders, balancing the company’s ambitious diversification with its current financial vulnerabilities.

Breaking Down the Q3 2025 Earnings Report

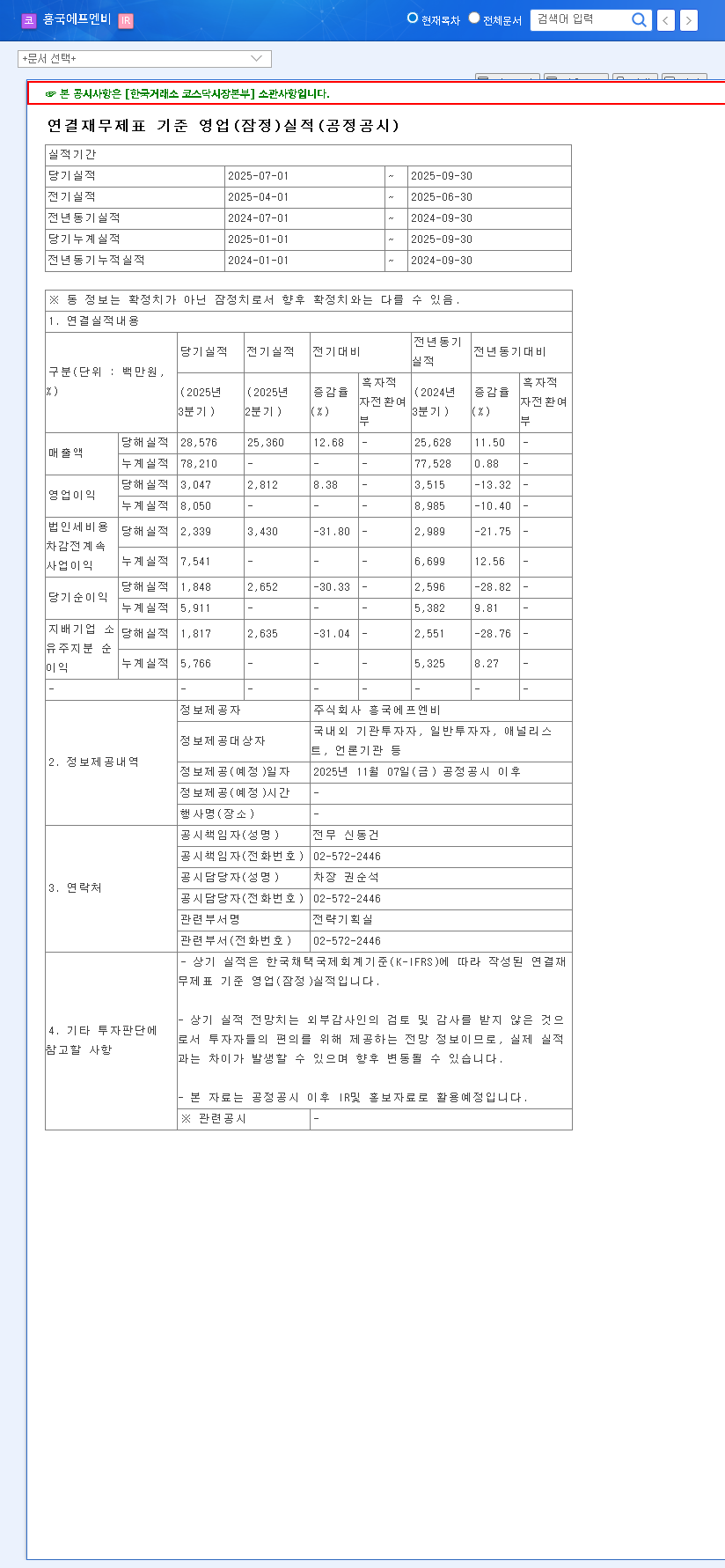

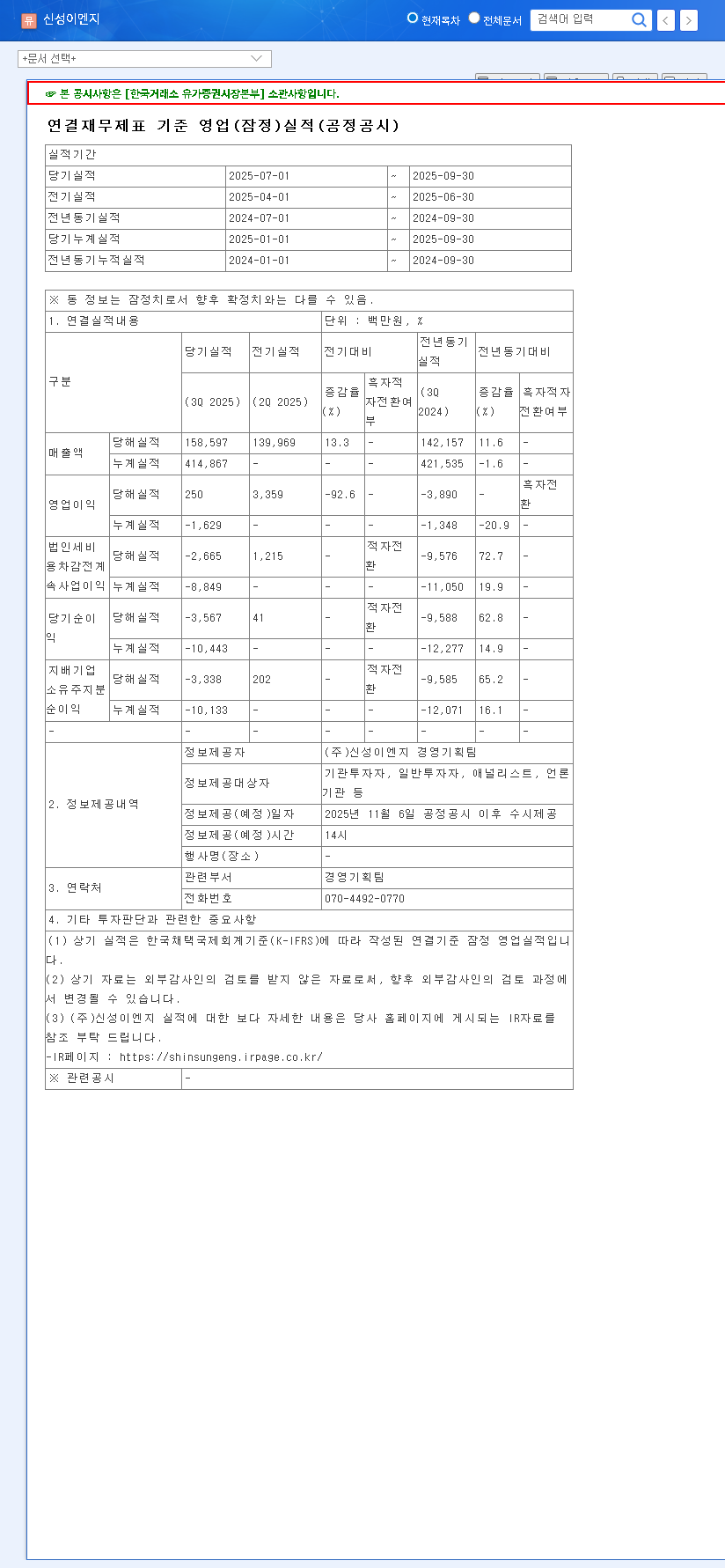

On November 7, 2025, HYUNGKUK F&B released its provisional third-quarter results, providing a crucial snapshot of its operational health. The figures, sourced from the company’s Official Disclosure on DART, are as follows:

- •Revenue: KRW 28.6 billion

- •Operating Profit: KRW 3.0 billion

- •Net Income: KRW 1.8 billion

While revenue and operating profit posted a modest sequential increase over Q2 2025, the decline in net income has become the central point of discussion. This divergence suggests that while the core business operations remain stable, non-operating factors such as rising costs, investment expenditures, or increased financial burdens are beginning to weigh on the bottom line. Understanding these underlying pressures is critical for any accurate HYUNGKUK F&B stock analysis.

Fundamental Analysis: Diversification vs. Financial Strain

Core Growth Drivers & Strategic Initiatives

HYUNGKUK F&B is not standing still. The company is actively pursuing a strategy of business diversification to build long-term, sustainable growth. Key initiatives include expanding into alcoholic beverages, developing new prune-based health products, and strengthening its coffee division. A major technological advantage is the expansion of its High-Pressure Processing (HPP) facilities. This technology allows for the creation of premium, preservative-free beverages with a longer shelf life, a significant differentiator in the competitive F&B market. This, combined with a robust B2B distribution network, forms the foundation of its future growth potential.

The success of HYUNGKUK F&B’s long-term vision hinges on its ability to successfully launch and scale these new ventures while navigating near-term financial and macroeconomic challenges.

Potential Risks and Company Headwinds

Despite the promising growth strategy, the latest HYUNGKUK F&B earnings report highlights several short-term risks. The primary concern is earnings volatility, evidenced by the declining net income. Furthermore, the company’s balance sheet shows increasing financial burdens, characterized by a high debt ratio and a significant rise in short-term borrowings. In an environment of rising interest rates, this debt structure poses a considerable risk to profitability, as financing costs are set to increase.

The Macroeconomic Gauntlet: External Pressures

No company operates in a vacuum. The current global macroeconomic climate presents significant challenges that could directly impact HYUNGKUK F&B’s performance.

- •Adverse Exchange Rates: With the KRW weakening against both the USD and EUR, the cost of importing essential raw materials like coffee beans, fruit concentrates, and packaging is rising sharply. This directly squeezes profit margins.

- •High Interest Rate Environment: With central banks in the US and Korea maintaining high benchmark rates, borrowing has become more expensive. This is particularly concerning for HYUNGKUK F&B given its reliance on short-term debt to finance operations and expansion.

- •Rising Commodity Prices: Volatility in international oil prices affects logistics and transportation costs, adding another layer of cost pressure on the company’s supply chain.

Investor Action Plan & Future Outlook

Given the complex picture painted by the Q3 results, investors should adopt a nuanced approach. A prudent strategy requires balancing short-term caution with a long-term perspective focused on the company’s strategic execution.

Key Watch Points for Investors

Moving forward, monitoring the following areas will be crucial for making informed decisions:

- •New Business Performance: Closely track the market reception and initial revenue from the new alcoholic beverage and prune product lines.

- •Financial Health Improvements: Look for concrete steps taken by management to improve the debt ratio and manage short-term liabilities. You can learn more about how to analyze corporate debt here.

- •Margin Management: Pay attention to gross and operating margins in the upcoming HYUNGKUK F&B earnings reports to see if the company is successfully managing rising input costs.

- •Macroeconomic Trend Impact: Keep an eye on authoritative sources like The Economist for shifts in currency and interest rate forecasts that could affect the company.

In conclusion, while the short-term outlook for HYUNGKUK F&B (KRX: 189980) is clouded by macroeconomic pressures and internal financial constraints, its long-term growth strategy centered on diversification and technological advantage holds promise. Prudent investors will weigh these factors carefully, demanding clear evidence of successful execution and financial discipline in the quarters to come.