This comprehensive analysis of the DB Inc. Q3 2025 earnings report provides investors with a detailed look into the company’s remarkable turnaround. Following the provisional earnings announcement, DB Inc. has captured significant market attention with impressive growth in sales, operating profit, and net income. But what are the underlying factors driving this performance, and what does this mean for the DB Inc. stock outlook?

In this report, we will dissect the key financial figures, explore the fundamental drivers of this growth, identify potential risks, and outline a strategic investment approach for current and prospective shareholders. Let’s explore the data behind DB Inc.’s promising quarter.

Decoding the DB Inc. Q3 2025 Earnings Report

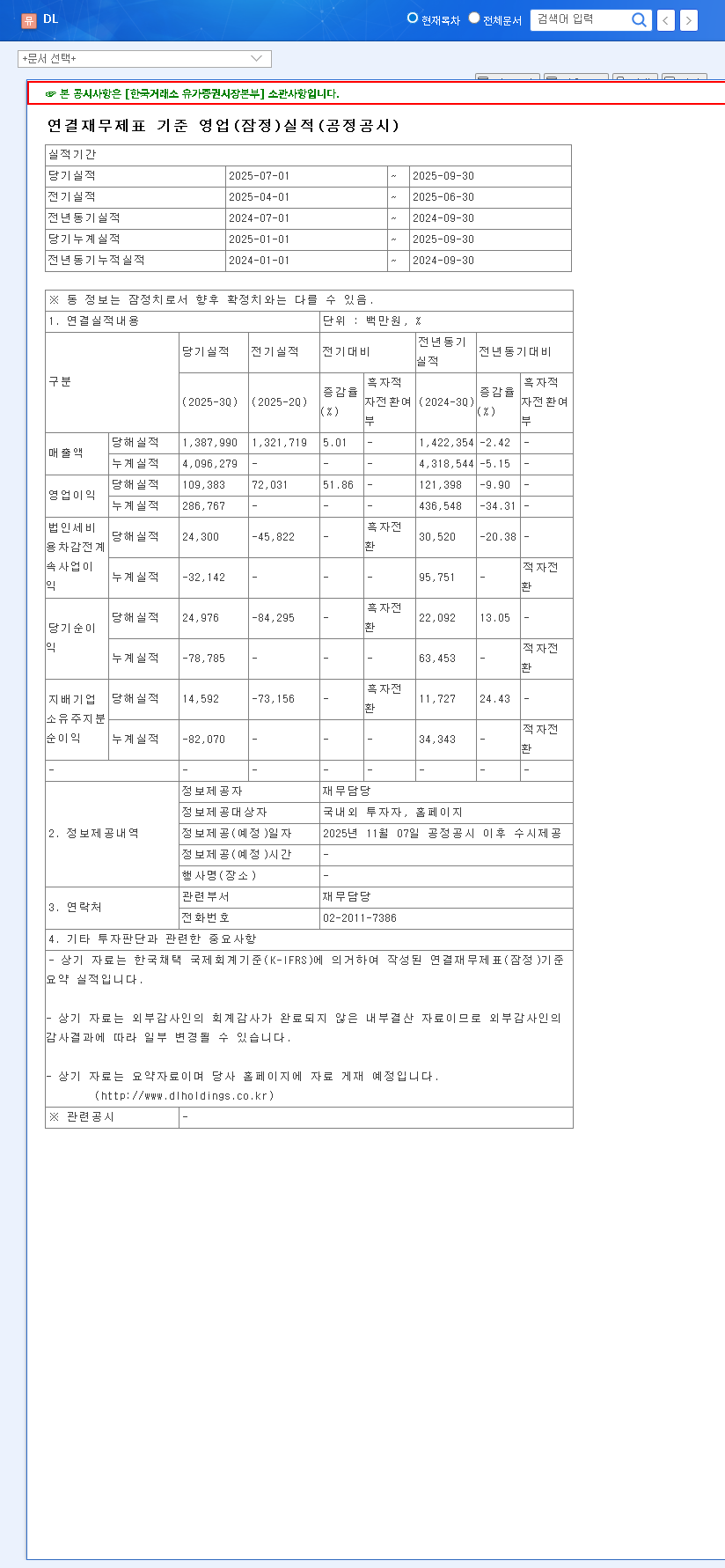

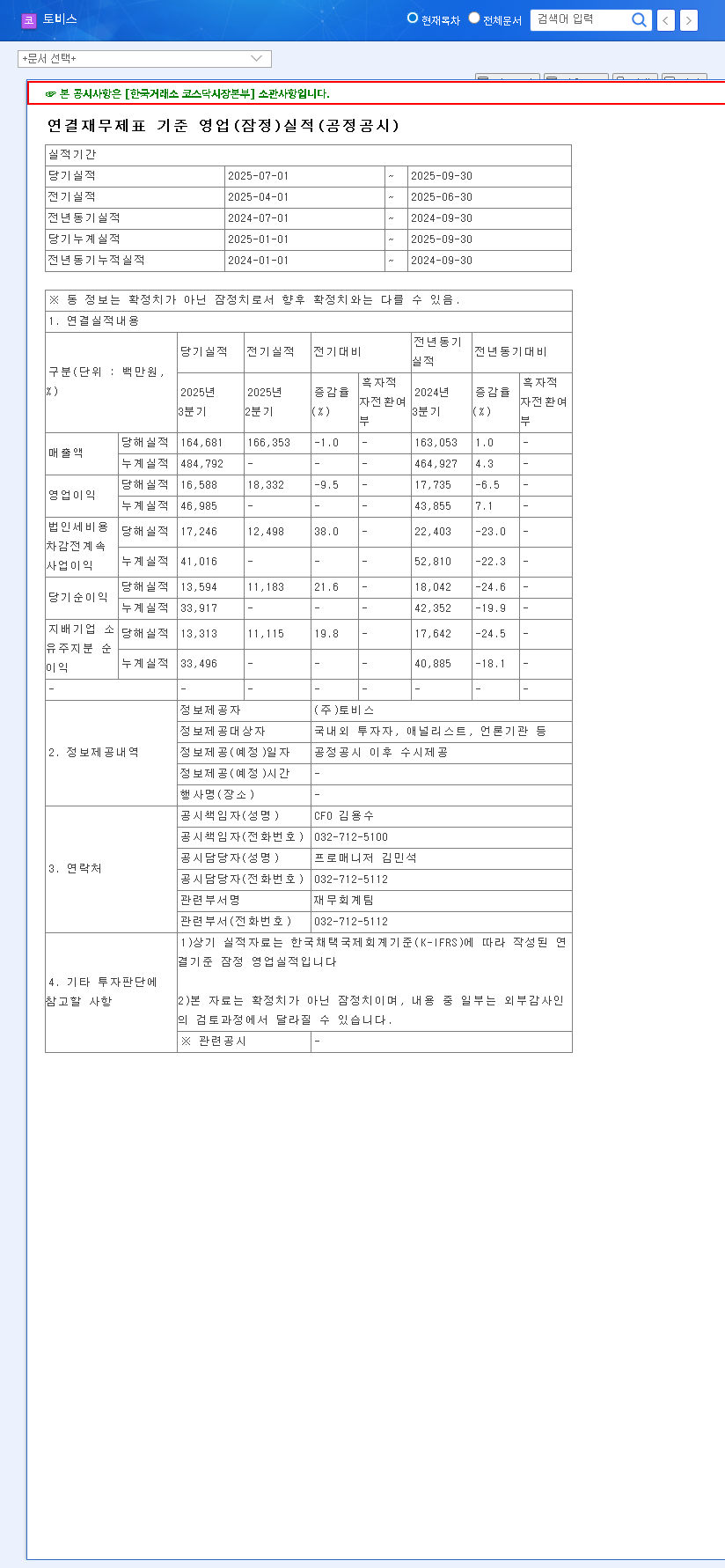

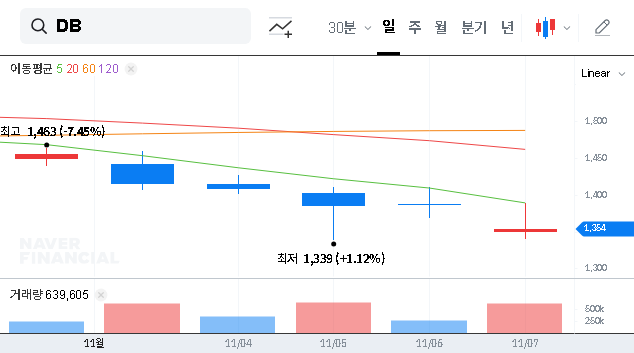

On November 7, 2025, DB Inc. released its provisional earnings, revealing a significant performance improvement compared to the previous quarter. The numbers paint a picture of strong recovery and operational efficiency. These figures are based on the company’s official filing, which can be viewed in the Official Disclosure on DART.

Key Financial Highlights (Quarter-on-Quarter)

- •Revenue: KRW 159.3 billion, a healthy increase of 6.1%.

- •Operating Profit: KRW 13 billion, a remarkable surge of 46.1%.

- •Net Income: KRW 26.6 billion, an impressive leap of 78.5%.

The substantial increases in operating profit and net income are the standout figures, signaling strong profitability and effective cost management. While market consensus data is limited for a direct comparison, these numbers inherently suggest a performance that has likely exceeded expectations, fueling positive investor sentiment.

“The surge in DB Inc.’s profitability isn’t just a number; it’s a testament to the resilience of its core business model and a strategic pivot towards higher-margin services. This quarter could be a pivotal moment for the company’s valuation.”

Fundamental Analysis: The Engines of Growth

To understand the sustainability of this growth, a deeper DB Inc. financial analysis is necessary. The company’s stability is rooted in its two primary divisions: IT services and trading. The latest results highlight the strength and evolving strategy within these core areas.

Positive Catalysts for DB Inc. Stock

- •Core Business Strength: The IT division is successfully expanding its external client base, leveraging its deep expertise from the financial sector. This, coupled with a strategic shift towards recurring revenue models like SaaS and IaaS, is enhancing profitability.

- •Operational Leverage: The jump in operating profit suggests excellent operational leverage. As revenues increased, fixed costs were spread over a larger base, and efficient cost controls likely amplified the bottom-line results.

- •Improved Financial Health: Data from the first half of 2025 already pointed towards a strengthening balance sheet, with an improved net debt-to-equity ratio and robust operating cash flow. The Q3 results build on this positive financial momentum. For more on industry trends, see our complete IT services market overview.

Potential Risks and Headwinds to Consider

A balanced DB Inc. investment strategy requires acknowledging potential risks. Investors should remain vigilant about the following factors:

- •Nascent New Ventures: While new initiatives in blockchain, insurance SaaS, and advertising are promising for long-term growth, they have yet to contribute meaningfully to the bottom line. Tangible results are needed to justify further investment.

- •Derivative Volatility: Past reports have shown sensitivity to derivative valuation losses. Fluctuations in currency exchange rates could introduce volatility to future earnings reports.

- •Macroeconomic Pressures: Global economic uncertainty and persistent high-interest rates, as reported by sources like Bloomberg, could dampen demand in the trading division and slow the progress of new business ventures.

Future Outlook & DB Inc. Investment Strategy

The positive momentum from the DB Inc. Q3 2025 earnings provides a strong foundation, but a forward-looking, cautious approach is prudent. Investors should focus their attention on several key areas to navigate the path ahead.

Key Monitoring Points for Investors:

- •Execution on New Businesses: Look for concrete updates on market entry, client acquisition, and revenue generation from the new ventures in upcoming quarterly reports.

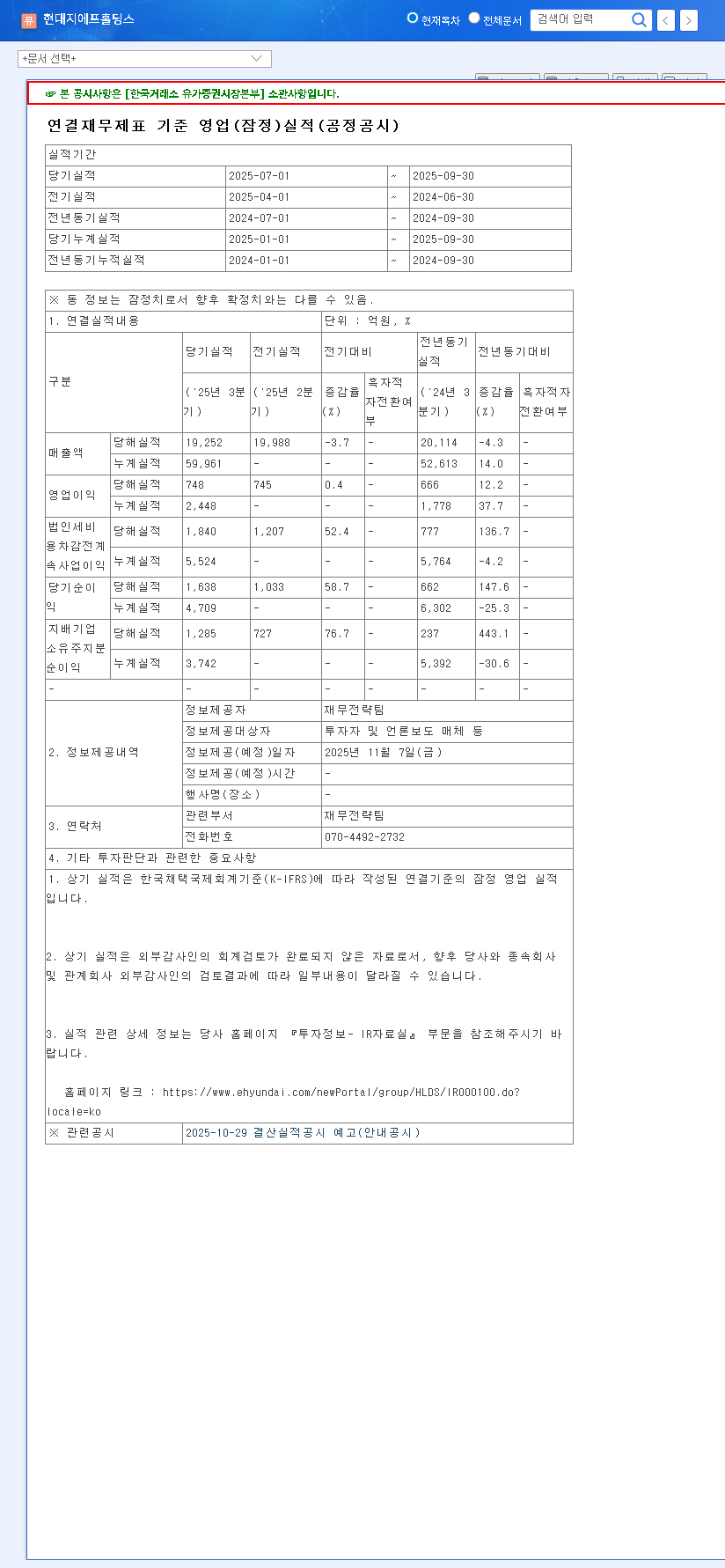

- •Affiliate Company Performance: The value and performance of key affiliates, such as DB Hitek, can have a material impact. Monitor their business results and market conditions.

- •Margin Sustainability: Assess whether the high profitability achieved in Q3 is sustainable. Is it due to one-off projects or a fundamental improvement in the business structure?

- •Competitive Landscape: Keep an eye on the competitive pressures in the IT service market, as this could affect pricing power and margins over the long term.

In conclusion, DB Inc.’s Q3 performance is an undeniably positive signal for the company and its stock. It demonstrates the strength of its core operations and its ability to enhance profitability. However, sustained long-term growth will depend on the successful diversification into new business areas and effective management of external financial and economic risks. A well-rounded investment thesis should balance the current optimism with a watchful eye on these future catalysts and challenges.