This comprehensive ME2ON Q3 2025 earnings analysis unpacks the latest financial data from the dynamic gaming and content company. As ME2ON navigates a pivotal transition from traditional gaming into the burgeoning realms of Web3 gaming and multimedia content, its Q3 2025 report offers a complex picture of progress and challenge. We will dissect the mixed signals of improved operating profit against a concerning drop in net income, evaluate the early performance of its flagship Web3 platform, ACE CASINO, and provide a forward-looking perspective for investors monitoring ME2ON stock.

ME2ON’s Q3 2025 results reveal a company in flux: profitability in core operations is stabilizing, but heavy investments in future growth, particularly in Web3, are impacting short-term net income. This quarter is a crucial test of their long-term diversification strategy.

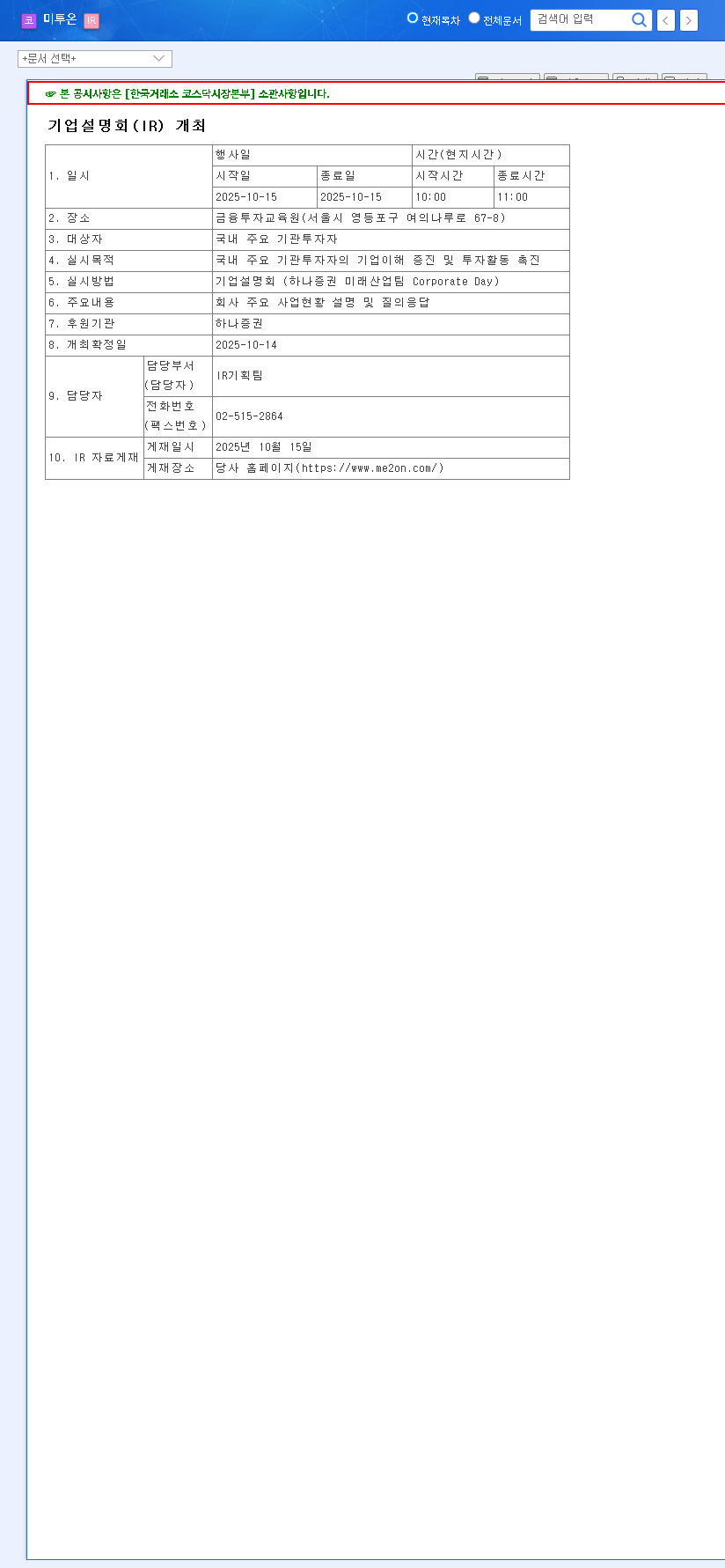

ME2ON’s Q3 2025 Financial Results at a Glance

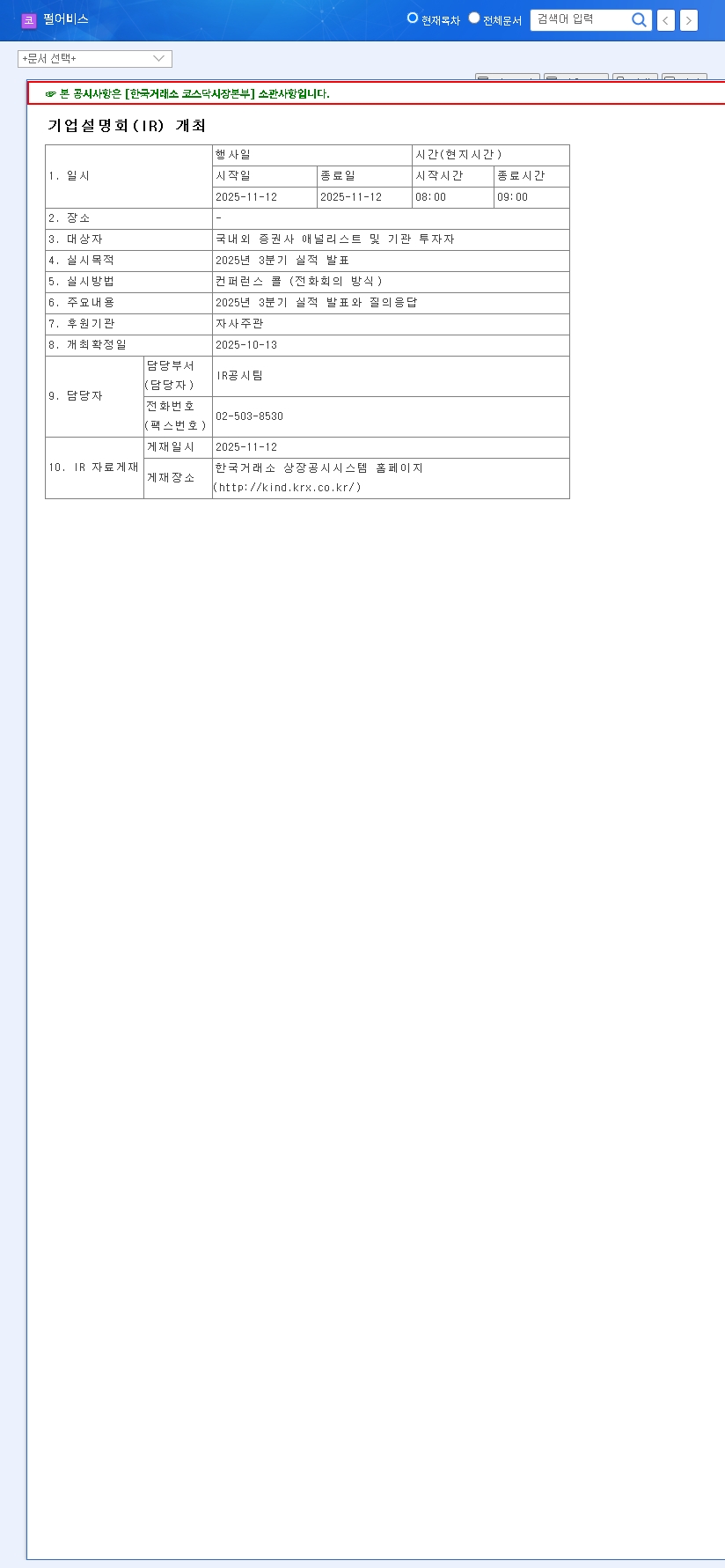

On November 12, 2025, ME2ON released its preliminary consolidated operating results, painting a nuanced picture of its current financial health. The numbers, sourced from their Official Disclosure (DART), require careful interpretation.

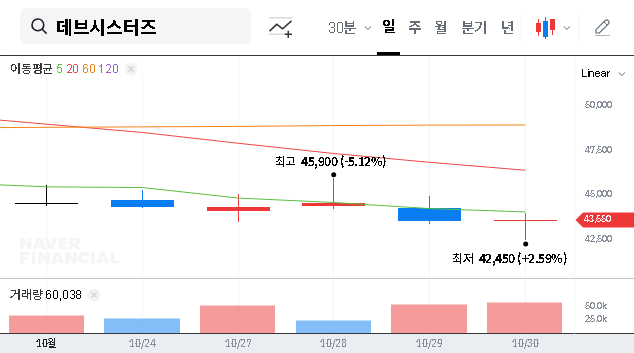

- •Revenue: KRW 22.7 billion (a marginal increase from Q2’s KRW 22.3 billion).

- •Operating Profit: KRW 3.3 billion (a healthy improvement from Q2’s KRW 2.9 billion).

- •Net Income: KRW 0.9 billion (a sharp decline from Q2’s KRW 2.3 billion).

While the growth in operating profit suggests a strengthening core business, the significant drop in net income immediately raises flags about rising costs, one-off expenses, or the financial burden of their ambitious expansion plans.

Deep Dive: ME2ON Q3 2025 Earnings Analysis

Operating Profit Recovery: A Glimmer of Hope

The increase in operating profit to KRW 3.3 billion is a key positive takeaway. It signals that ME2ON’s efforts to stabilize its existing social casino game portfolio, particularly after a sluggish period in late 2024, are bearing fruit. This core profitability is essential as it provides the financial foundation needed to fund riskier, high-growth ventures in the Web3 and content sectors. It indicates operational efficiency and resilience in their primary market.

The Net Income Conundrum

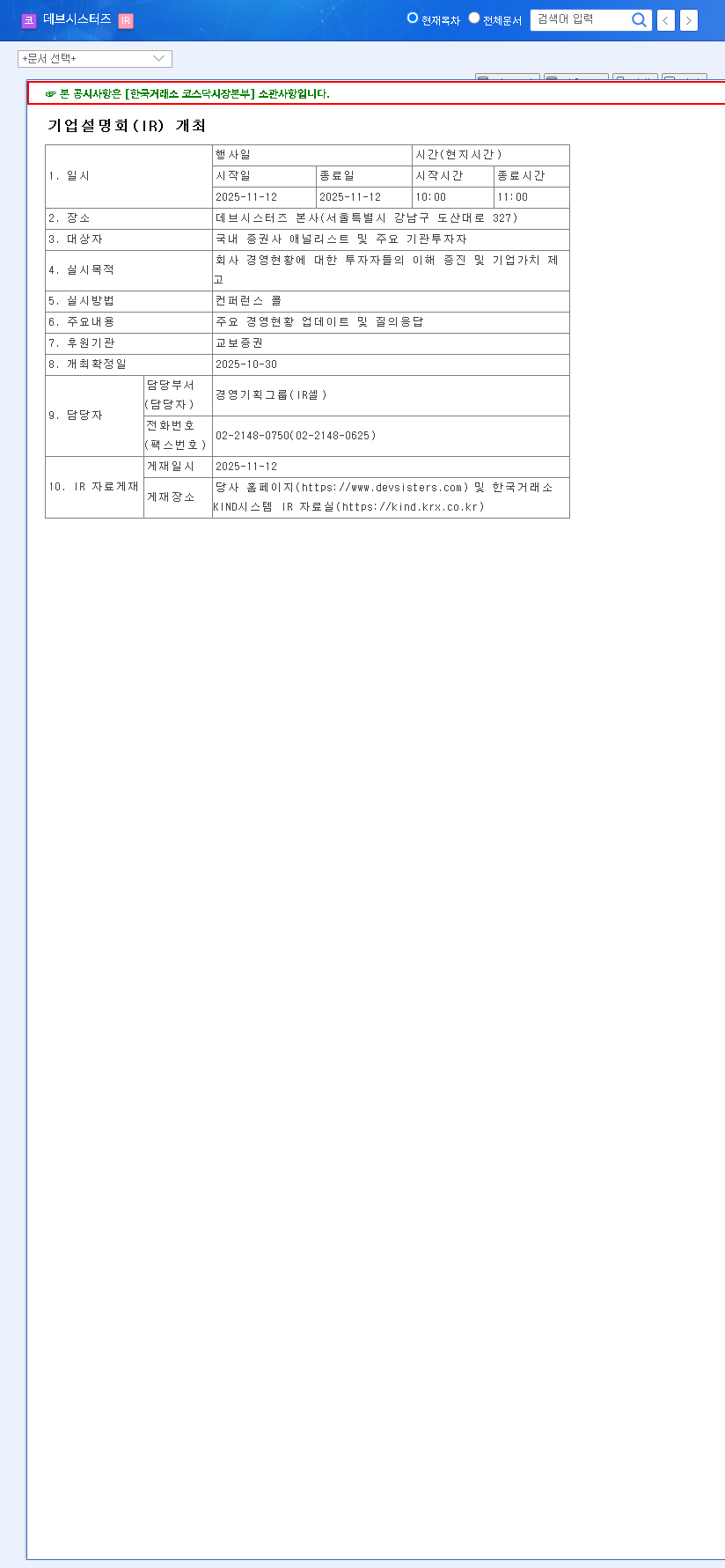

The stark drop in net income to KRW 0.9 billion is the report’s most significant concern. This is often attributed to factors below the operating line, such as non-operating expenses, higher taxes, or, most likely in this case, substantial initial investment costs for new projects. The global launch of the ACE CASINO platform and the scaling of their content production arm are capital-intensive. Investors will be keenly awaiting the full financial report to determine if these are temporary strategic expenditures or signs of deeper financial strain.

Strategic Pivot: Beyond Gaming to Web3 and Content

ME2ON’s future is inextricably linked to its diversification strategy. The company is betting heavily on two key pillars to drive its next phase of growth, moving beyond its traditional social casino comfort zone.

The ‘ACE CASINO’ Web3 Gamble

Launched in June 2025, ACE CASINO is ME2ON’s flagship entry into the Web3 gaming ecosystem. As a stablecoin-based online casino, it aims to attract a global audience familiar with cryptocurrency and blockchain technology. The success of this platform is paramount. It represents not just a new revenue stream but a fundamental shift in the company’s technological focus. For more on the underlying technology, you can read our guide on What is Web3 Gaming? The initial user adoption rates and monetization metrics for ACE CASINO in the coming quarters will be the most critical indicators of whether this high-stakes bet will pay off.

Content is King: IP Diversification

Recognizing the power of intellectual property (IP), ME2ON is expanding into webtoon, web novel, and drama production. This strategy aims to create a synergistic ecosystem where compelling stories and characters can be cross-pollinated into games, and vice-versa. Owning the IP provides long-term value and multiple avenues for monetization, reducing reliance on the volatile gaming market. This move aligns with a broader industry trend where media giants are converging content and interactive entertainment, as noted by industry analysts at major financial news outlets.

Investor Outlook: Key Factors for ME2ON Stock

For those evaluating ME2ON stock, the Q3 2025 earnings report provides several key points to monitor moving forward. A balanced view is essential, weighing the short-term pressures against the long-term potential.

- •New Venture ROI: The single most important metric will be the tangible revenue and profit contribution from ACE CASINO and the new content division. Watch for specific numbers in future reports.

- •Cost Management: Scrutinize future financial statements for signs that the costs associated with new ventures are being controlled and are leading to a clear return on investment.

- •Core Business Stability: Ensure the traditional social casino business remains a stable and profitable foundation. Any significant decline here could jeopardize the funding for diversification.

- •Macroeconomic Headwinds: With a large portion of its business overseas, ME2ON’s performance will be influenced by currency exchange rates (KRW/USD) and the overall health of the global gaming market.

In conclusion, ME2ON is a company at a crossroads. The Q3 2025 results highlight the inherent tension between maintaining current profitability and investing aggressively for a decentralized, content-rich future. Investors should proceed with cautious optimism, focusing on the execution and tangible results of the company’s bold new strategy in the quarters to come.