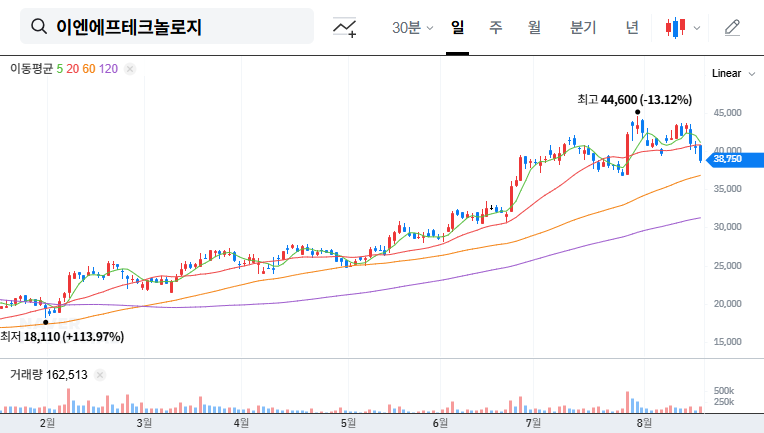

The release of the ENF Technology Q3 2025 earnings report on November 12, 2025, has sent ripples through the investor community, offering a critical look into the health and trajectory of this key player in the semiconductor materials sector. For investors tracking ENF Technology stock (이엔에프테크놀로지), this announcement is more than just numbers; it’s a barometer for industry trends and a roadmap for future growth potential. This deep-dive analysis will dissect the core financial highlights, evaluate the potential impact on the stock price, and outline a strategic approach for current and prospective investors.

ENF Technology’s impressive profitability and strengthened financial position in Q3 signal robust operational efficiency and a solid foundation for capitalizing on the recovering semiconductor market.

Core Financial Highlights from the ENF Technology Q3 2025 Earnings Report

The official Q3 2025 management performance announcement IR, available via the Official Disclosure (DART), paints a picture of a company on a strong upward trajectory. Let’s break down the key fundamentals that are capturing investor attention.

Exceptional Profitability and Revenue Growth

ENF Technology reported cumulative revenue of KRW 494.1 billion and a substantial operating profit of KRW 66.9 billion. The standout metric, however, is the remarkable 53.0% year-on-year increase in net profit. This significant jump in profitability suggests not only strong sales but also enhanced operational efficiency and effective cost management, which are crucial indicators of a well-managed semiconductor materials company.

Fortified Financial Stability

A company’s ability to weather economic storms and fund future growth is reflected in its balance sheet. ENF Technology has significantly strengthened its financial health:

- •Reduced Debt: The debt-to-equity ratio improved to 64.7%, indicating lower financial risk and greater leverage for strategic initiatives.

- •Increased Liquidity: Cash and cash equivalents surged by 67.2%, providing ample capital for R&D, potential acquisitions, and operational flexibility.

Growth Catalysts and Market Position

Beyond the numbers, the true potential of an ENF Technology investment lies in its strategic positioning and technological edge. The company is poised to benefit from several powerful market tailwinds.

Dominance in Critical Materials

ENF Technology’s core competency is in high-growth raw materials for photoresists—a critical component in the semiconductor and display manufacturing process. As chip designs become more complex and display technology like OLED becomes more widespread, the demand for these specialized chemicals is set to soar. Continuous R&D investment ensures the company maintains its technological leadership in this niche but vital segment. For more on market trends, see this analysis of the global semiconductor industry.

Favorable Macro-Economic Environment

Several market forces are converging to create a positive environment for the company. The ongoing recovery of the global semiconductor industry, coupled with the expansion of the OLED market, provides a strong demand foundation. Furthermore, the strategic trend towards domestic material localization in key manufacturing hubs strengthens ENF Technology’s market position against foreign competitors.

Investment Analysis: Opportunities vs. Risks

A prudent ENF Technology investment strategy requires a balanced view of both the potential upside and the inherent risks. The strong Q3 2025 earnings provide a bullish case, but savvy investors must also weigh the potential headwinds.

The Bull Case (Potential Positives)

- •Strong Investor Sentiment: Stellar performance and high net profit growth can significantly boost market confidence, potentially driving stock price appreciation.

- •Future Growth Narrative: Clear articulation of growth plans in next-generation displays and battery materials could lead to a positive re-evaluation of the company’s long-term potential. Learn more about evaluating growth stocks in our guide.

- •Shareholder-Friendly Policies: Any announcements regarding dividends or share buybacks could act as a further catalyst for the stock.

The Bear Case (Potential Risks)

- •Macroeconomic Volatility: The Q3 report noted an increase in financial costs to KRW 11.2 billion, highlighting sensitivity to interest rate changes. Exchange rate fluctuations can also impact raw material import costs.

- •Industry Cyclicality: The company’s fortunes are closely tied to the cyclical semiconductor and display industries. A downturn in these sectors would inevitably impact performance.

- •Competitive Pressures: The special chemicals market is highly competitive. ENF must continuously innovate to maintain its technological and price advantages.

Conclusion: A Compelling but Cautious Outlook

The ENF Technology Q3 2025 earnings report undeniably confirms the company’s positive fundamentals and robust financial health. The impressive profit growth and strong market positioning present a compelling investment case. However, investors should proceed with a strategic mindset, closely monitoring management’s plans for risk mitigation and diversification into new growth areas. The key will be whether the company can translate its current success into a sustainable long-term growth story amidst a dynamic and competitive global market.

Disclaimer: This analysis is for informational purposes only and is based on publicly available information. It does not constitute financial advice. The ultimate responsibility for investment decisions rests with the individual investor.