ExicureHytron Contract: Analyzing the ₩1.7B Deal and Its Real Impact

In a move that has caught the attention of investors, ExicureHytron Co., Ltd. has landed a significant public sector deal. But while the headline figure of ₩1.7 billion looks impressive, a deeper look reveals a complex picture of opportunity and risk. This article provides a comprehensive analysis of the new ExicureHytron contract, exploring what it means for the company’s future, its shaky financials, and what investors should be monitoring closely.

While this contract represents a 25.67% boost based on recent sales, ExicureHytron has been navigating severe financial turbulence. The critical question remains: is this a genuine turning point or merely a temporary patch on a much larger problem? Let’s break down the details.

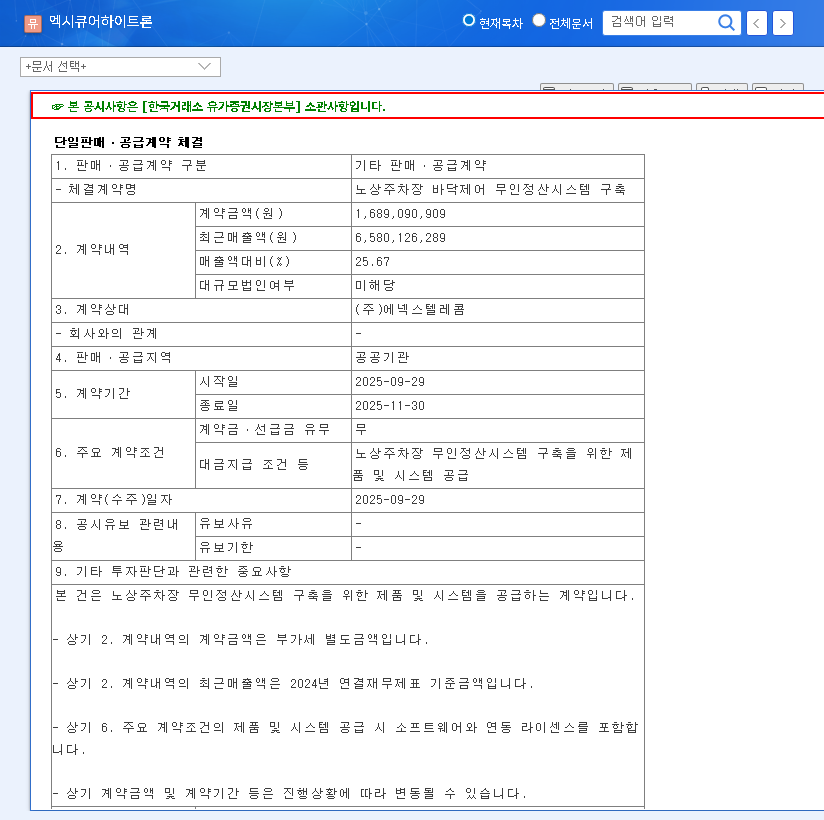

What’s Inside the ₩1.7 Billion ExicureHytron Contract?

On September 29, 2025, ExicureHytron announced the signing of a contract with Enex Telecom Co., Ltd. The project, valued at ₩1.7 billion, is for the “Construction of Roadside Parking Floor Control Unmanned Settlement System” for a public institution. This marks a strategic, albeit temporary, pivot from their core business.

Here’s a quick overview:

- Project Value: ₩1.7 billion (approx. 25.67% of recent revenue).

- Project Scope: Building an automated, unmanned payment system for roadside parking.

- Contract Period: A short two-month window from September 29, 2025, to November 30, 2025.

- Client Type: Public institution, which typically signifies a stable and reliable client.

This venture into IT infrastructure for public transit systems is a notable diversification from ExicureHytron’s primary focus on its AI-based security solution, ‘HASS’. Securing a government-related project can often open doors to more opportunities and lends credibility to a company’s technical capabilities.

A Glimmer of Hope Amidst Financial Turmoil

To understand the importance of this contract, we must look at the company’s recent financial health. The first half of 2025 painted a bleak picture, with operating losses surpassing ₩10 billion and net losses exceeding ₩20 billion. A high debt-to-equity ratio and the burden of convertible bonds have placed immense pressure on the company’s balance sheet.

Against this backdrop, the ExicureHytron contract offers several key advantages:

- Immediate Revenue Injection: The most direct benefit is the short-term revenue boost, which can provide much-needed cash flow.

- Business Diversification: It demonstrates the company’s ability to win contracts outside its core security market, potentially reducing reliance on a single product line.

- Enhanced Credibility: Winning a competitive public tender proves the company’s technical reliability and project management skills, which can be leveraged for future bids.

A Reality Check: Will This Deal Be Enough?

While the positives are clear, it’s crucial for investors to maintain a pragmatic perspective. A single, short-term contract is rarely enough to solve deep-rooted financial issues. According to standard financial reporting principles from major regulators, one-time revenue events can sometimes mask ongoing operational inefficiencies.

Hopes: The Upside Potential

- Portfolio Expansion: Success in this project could establish ExicureHytron as a viable player in the smart city and IT infrastructure space.

- Follow-on Business: A well-executed project might lead to maintenance contracts or further projects with the same public institution.

Hurdles: The Significant Limitations

- Insufficient Scale: A ₩1.7 billion revenue bump is a drop in the bucket compared to the tens of billions in accumulated losses. It does not fundamentally alter the company’s weak financial structure.

- Short-Term Nature: The two-month contract period raises concerns about sustainability. Without a pipeline of similar deals, this will be a one-off event.

- Unknown Profitability: Revenue does not equal profit. The project’s actual profit margin is unknown, and it may not contribute significantly to improving operating income after costs are factored in.

Investor Action Plan: A Call for Cautious Optimism

Given the circumstances, a ‘wait and see’ approach is the most prudent strategy. While the ExicureHytron contract is a positive development, it shouldn’t be the sole basis for an investment decision. Before committing capital, it’s essential to understand the company’s complete technology stack. For more details on their main product, see our previous analysis of the AI-based security solutions market.

Key Monitoring Points for Investors:

- Future Contract Wins: Is the company securing additional business, particularly in this new IT infrastructure sector? Or was this a one-time win?

- Quarterly Financial Reports: Closely monitor the upcoming financial statements for real changes. Look for improved profit margins, a reduction in the debt ratio, and sustained revenue growth beyond this single contract.

- Core Business Performance: Don’t lose sight of the ‘HASS’ AI security solution. Is the core business showing signs of growth, or is the company desperately seeking revenue elsewhere?

- Management Commentary: Pay attention to official company communications regarding their strategy for achieving long-term financial stability.

In conclusion, this deal is a step in the right direction but not a leap. It provides a temporary lifeline and a chance to prove its capabilities in a new market. However, the path to financial recovery for ExicureHytron remains long and uncertain. A ‘Hold’ or ‘Cautious Approach’ rating is advisable until there is clear evidence of a sustainable turnaround.