On November 7, 2025, KOREA DISTRICT HEATING CORPORATION (KDHC, KRX: 071320) delivered a landmark ‘earnings surprise’ that shattered market forecasts and sent a clear signal to investors. With operating profits soaring an astonishing 627.6% above estimates, the critical question for anyone evaluating KOREA DISTRICT HEATING CORPORATION stock is whether this is a fleeting moment of success or the dawn of a sustained growth period. This comprehensive analysis will dissect the Q3 2025 results, explore the underlying fundamentals, and provide a strategic outlook for potential investors.

We will delve into the strengths powering this performance, the significant risks that still loom, and the macroeconomic factors that could shape the future of KDHC. Join us for an in-depth look at the company’s trajectory and what it means for your investment portfolio.

KDHC’s Stunning Q3 2025 Earnings by the Numbers

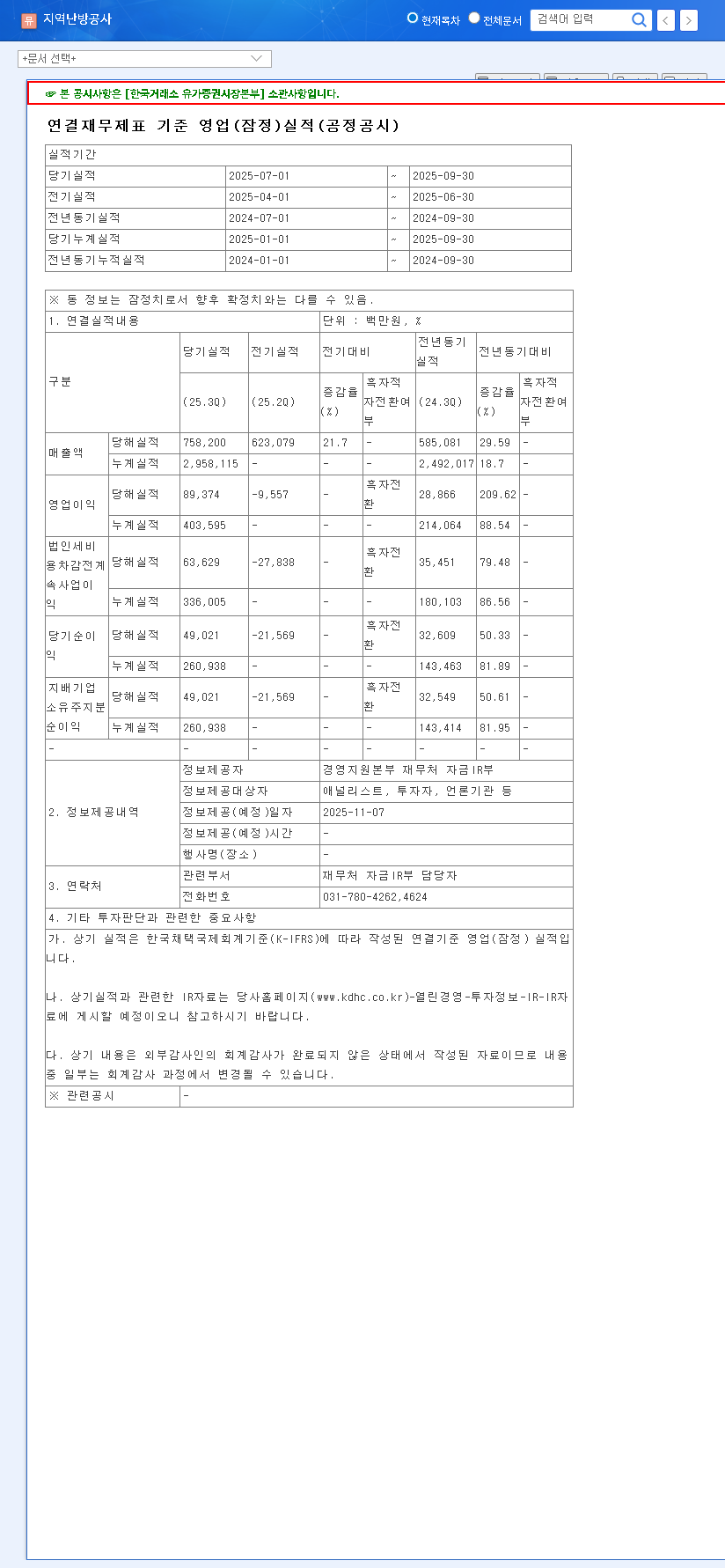

The provisional earnings announced by KDHC for the third quarter of 2025, based on consolidated financial statements, were nothing short of spectacular. The company didn’t just beat expectations; it left them in the dust, showcasing robust top-line growth and explosive profitability. The full details can be found in the Official Disclosure on DART, but the key highlights are:

- •Revenue: KRW 758.2 billion, a 38.1% increase over the estimate of KRW 549.1 billion.

- •Operating Profit: KRW 89.4 billion, a massive 627.6% surge compared to the KRW 12.3 billion estimate.

- •Net Profit: KRW 49.0 billion, an incredible 581.1% higher than the KRW 7.2 billion forecast.

This ‘earnings surprise’ significantly boosts investor confidence and provides powerful short-term momentum for the KOREA DISTRICT HEATING CORPORATION stock. The remarkable growth in operating and net profit suggests improved operational efficiency and favorable market conditions during the quarter.

Fundamental Analysis: The Bull Case vs. The Bear Case

To truly understand the investment thesis, we must look beyond a single quarter. KDHC possesses foundational strengths but also faces considerable structural challenges that any prudent investor must weigh.

Strengths: Why KDHC Could Thrive

- •Dominant Market Position: As a key player in the district heating business, KDHC enjoys a stable, utility-like business model supplying essential energy, which provides a reliable revenue floor.

- •Future Growth Drivers: The company is not standing still. It is actively investing in high-potential areas like renewable energy and the innovative use of waste heat for powering data centers, tapping into modern industrial needs.

- •Stellar Creditworthiness: With ratings like AA3 from Moody’s and AAA domestically, KDHC can secure financing at favorable rates, a crucial advantage for a capital-intensive business.

- •ESG Commitment: A strong focus on ESG (Environmental, Social, and Governance) management is increasingly important for attracting institutional capital and enhancing long-term corporate value. You can learn more in our guide to ESG investing.

The core dilemma for KDHC investors is balancing this quarter’s spectacular performance against persistent structural risks like high debt and commodity price exposure. The future value hinges on management’s ability to navigate these challenges.

Risks: What Could Derail Growth

- •High Debt-to-Equity Ratio: A debt ratio of 236.5% is a significant concern. This high leverage makes the company vulnerable to interest rate hikes and increases financial expenses, which stood at KRW 56.9 billion.

- •Raw Material Volatility: The company’s profitability is highly sensitive to fluctuations in raw material prices, particularly Liquefied Natural Gas (LNG). With LNG accounting for over 80% of purchases, global energy market shifts, as tracked by sources like Reuters Energy, can drastically impact margins.

- •Investment Burden: While necessary for growth, large-scale investments in facility upgrades and new businesses (totaling KRW 262.2 billion) can strain financial resources in the short to medium term.

- •Regulatory and Legal Risks: Navigating carbon neutrality goals and climate change regulations could lead to increased compliance costs. Furthermore, ongoing litigation presents a potential financial risk depending on the outcomes.

Outlook & Investment Strategy for KDHC Stock

The powerful KDHC earnings report for Q3 is expected to act as a significant catalyst. In the short term, the positive news flow and improved sentiment will likely attract buying interest from institutional and foreign investors, potentially driving the stock price higher. Analyst ratings and price targets will almost certainly see upward revisions.

However, the long-term re-evaluation of KOREA DISTRICT HEATING CORPORATION stock depends entirely on the company’s ability to prove this performance is sustainable. Investors should monitor subsequent quarters for continued momentum while keeping a close eye on management’s strategies for debt reduction and margin protection against commodity swings.

Final Verdict & Action Plan

Given the exceptional results and the immediate positive momentum, we are issuing a ‘Positive’ investment opinion at this time. However, this comes with a strong recommendation for active monitoring.

- •For Short-Term Traders: Consider leveraging the positive sentiment following the earnings release. A phased buying approach on any pullbacks could be a viable strategy to capture the upward momentum.

- •For Long-Term Investors: Look for tangible progress in de-risking the balance sheet. Key metrics to watch in future reports include the debt-to-equity ratio, operating margins in both the heat and electricity segments, and concrete returns from new business ventures.

- •Monitor Macro Indicators: Keep a close watch on LNG prices, the KRW/USD exchange rate, and national energy policy shifts, as these external factors will continue to have a profound impact on KDHC’s profitability.

This analysis is based on publicly available information. All investment decisions should be made based on your own research and risk tolerance.