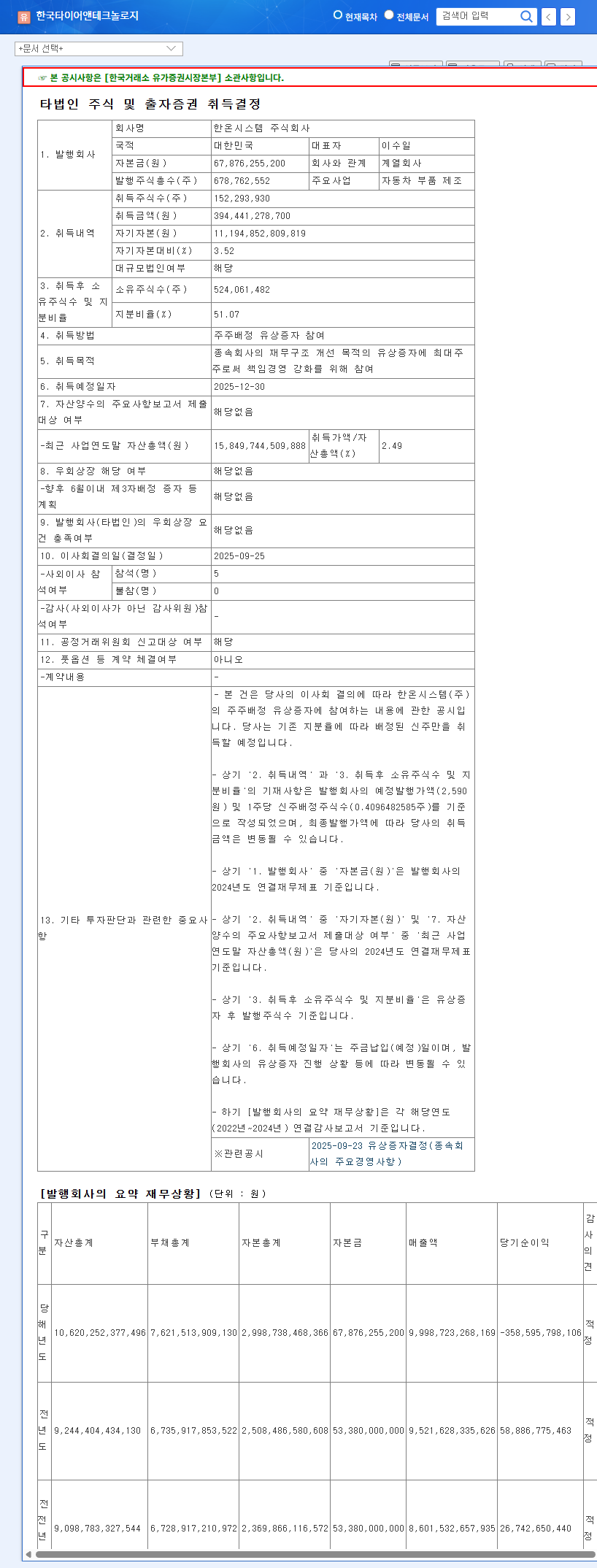

1. What Happened? Hankook Tire’s ₩394.4B Investment in Hanon Systems

Hankook Tire & Technology is participating in a ₩394.4 billion rights offering for its subsidiary, Hanon Systems, to improve its financial structure. This allows Hankook Tire to maintain its 51.07% stake and reinforce its commitment to responsible management as the majority shareholder.

2. Why the Investment? Rescuing Hanon Systems

Hanon Systems has recently faced declining profitability. This rights offering aims to reduce Hanon’s debt ratio and improve its financial health, ultimately contributing to Hankook Tire & Technology’s consolidated earnings improvement.

3. What’s the Impact? Coexistence of Opportunities and Risks

- Positive Impacts: Improved financial structure for Hanon Systems, expected consolidated earnings improvement, potential future synergies

- Potential Risks: Increased financial burden on Hankook Tire & Technology, uncertainty about Hanon Systems’ profitability improvement, influence of macroeconomic variables (exchange rates, interest rates)

4. What Should Investors Do? Dispassionate Analysis and Observation Required

- Monitor Hanon Systems’ quarterly earnings and financial structure improvement trends (operating profit margin, debt ratio)

- Check the synergy creation plan and progress between Hankook Tire & Technology and Hanon Systems

- Pay attention to changes in macroeconomic variables such as exchange rates and interest rates

This investment can be interpreted as a strategic decision to enhance Hankook Tire & Technology’s long-term growth potential. However, careful investment decisions should be made considering the short-term financial burden and execution risks.

Frequently Asked Questions (FAQ)

How will Hankook Tire’s financial status be affected by this rights offering?

In the short term, the investment of ₩394.4 billion could increase the financial burden. However, in the long run, it is expected to have a positive impact on the consolidated financial statements through improvements in Hanon Systems’ financial structure and profitability.

What is the likelihood of Hanon Systems improving its profitability?

Securing financial soundness through the rights offering and creating future business synergies are expected to increase the likelihood of profitability improvement. However, uncertainties remain, considering the volatility of the automotive industry and external factors.

What should investors pay attention to?

Investors should closely monitor Hanon Systems’ future earnings announcements for trends in financial restructuring and profitability, and confirm synergy creation with Hankook Tire & Technology. Furthermore, the impact of macroeconomic variables such as exchange rate and interest rate fluctuations should be considered.