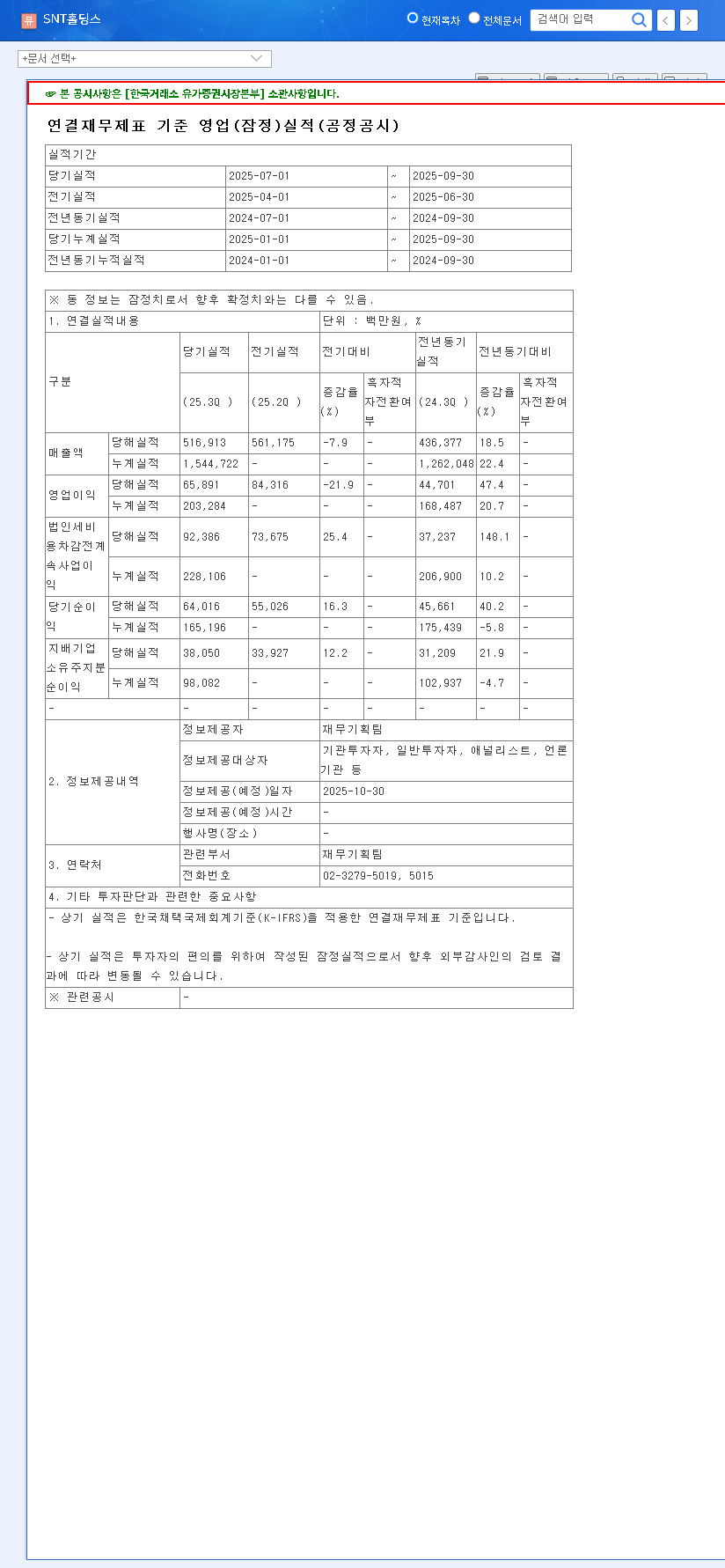

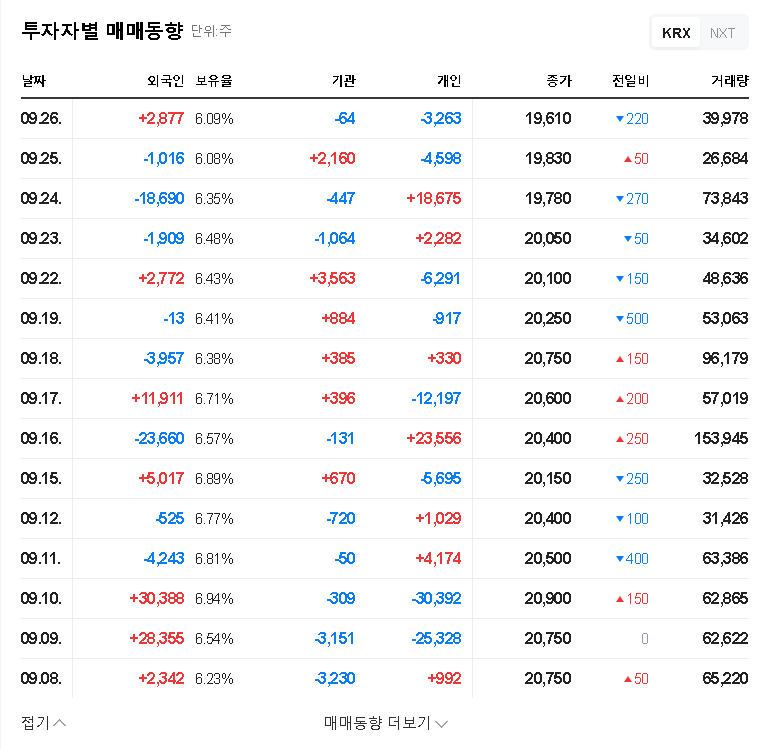

The latest provisional Doosan Bobcat Q3 results have created a complex narrative for investors. While the company celebrated a modest revenue beat, a significant shortfall in profitability has raised serious questions about its operational health and future stock performance. According to the Official Disclosure, the divergence between sales and earnings points to mounting pressures from both a slowing global economy and rising operational costs.

This in-depth Doosan Bobcat analysis will dissect the Q3 performance, explore the root causes of the profitability decline, and provide a clear outlook for investors navigating this uncertain period. We will examine the challenges facing the construction equipment market and what it means for Doosan Bobcat stock.

Doosan Bobcat Q3 Results: A Closer Look at the Numbers

At first glance, the top-line figures seem encouraging. However, the story quickly changes as we move down the income statement, revealing significant challenges to Doosan Bobcat profitability.

- •Revenue: KRW 2,115.2 billion, which is a 3.4% beat over market consensus. This suggests continued demand and effective sales execution.

- •Operating Profit: KRW 133.6 billion, a significant 18.0% miss compared to expectations. This is the first major red flag, indicating that the cost of generating revenue is escalating.

- •Net Profit: KRW 81.9 billion, a staggering 36.2% below forecasts. This dramatic shortfall highlights the combined impact of operational issues and financial costs.

Analyzing the Profitability Gap: External Pressures & Internal Shifts

The sharp decline in profitability wasn’t caused by a single factor but a confluence of challenging macroeconomic conditions and internal business dynamics. Understanding these pressures is key to evaluating the company’s future.

Global Headwinds: The Macroeconomic Squeeze

Doosan Bobcat operates in a cyclical industry, making it highly sensitive to global economic trends. Several external factors are currently compressing margins:

- •Construction Market Slowdown: Persistently high interest rates in North America and Europe, driven by central bank policies (as detailed by institutions like the Federal Reserve), have cooled the construction boom. This directly impacts sales of heavy equipment.

- •Elevated Costs: A surge in raw material prices, particularly steel, and volatile logistics costs tied to global shipping indexes have directly increased the cost of goods sold.

- •Currency and Rate Volatility: While a strong USD can boost translated revenue, it also creates hedging challenges. More importantly, rising interest rates increase the company’s financing costs, directly eating into net profit.

Internal Strategy: Diversification vs. Core Business Weakness

Internally, Doosan Bobcat is making strategic moves to build long-term resilience. The acquisition of Motrol Co., Ltd. introduced a hydraulic equipment business, a smart diversification that has already shown impressive growth of over 120%. This new segment is a bright spot, contributing positively to the top line.

However, this positive step was overshadowed by a significant slump in the core Construction Equipment (CE) division. Sales in key markets of North America and Europe fell sharply, causing the segment’s operating profit to plummet by 32.4%. This highlights a vulnerability in the company’s primary revenue stream that the new ventures cannot yet fully offset.

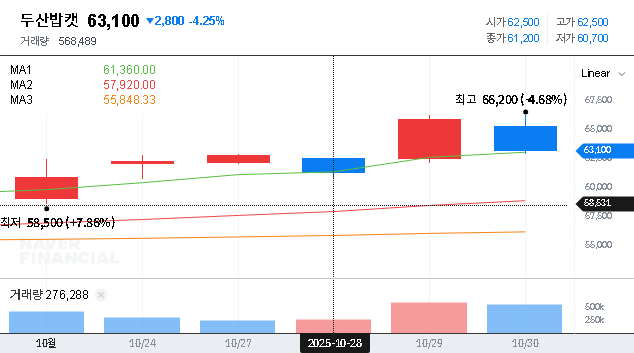

While top-line growth is positive, the market’s focus has decisively shifted to bottom-line execution and margin preservation. The immediate reaction to the Doosan Bobcat Q3 results will be driven by the profit miss.

Doosan Bobcat Stock: Investor Outlook and Key Factors

For current and potential investors, the key question is how this translates to stock performance. The outlook is bifurcated between short-term headwinds and long-term potential.

Short-Term Caution Warranted

In the short term, downward pressure on Doosan Bobcat stock is almost inevitable. The market typically punishes significant earnings misses harshly, as they signal potential underlying issues with cost control or demand forecasting. Investors will likely remain cautious until there is clear evidence of margin stabilization.

Path to Long-Term Value Recovery

Despite the short-term pain, Doosan Bobcat is laying the groundwork for future growth. Investors should monitor the progress of these initiatives, as they will be the primary catalysts for a long-term re-rating of the stock. For more context, you can read our analysis of broader construction sector trends.

Final Verdict & Investor Checklist

The Doosan Bobcat Q3 results signal a period of transition. The company achieved sales growth but failed to protect its bottom line. A conservative, observant approach is recommended. Investors should closely monitor the following points in upcoming quarters:

- •Cost Management: Look for specific commentary and results related to controlling raw material and logistics expenses.

- •Core Business Rebound: Is the decline in the Construction Equipment segment stabilizing or reversing?

- •New Segment Contribution: How is the hydraulic equipment business contributing to overall profitability, not just revenue?

- •Shareholder Returns: Are buybacks and dividends being maintained, signaling management’s confidence?

Ultimately, a sustained improvement in Doosan Bobcat profitability will be the most critical factor in restoring investor confidence and driving the stock price higher.