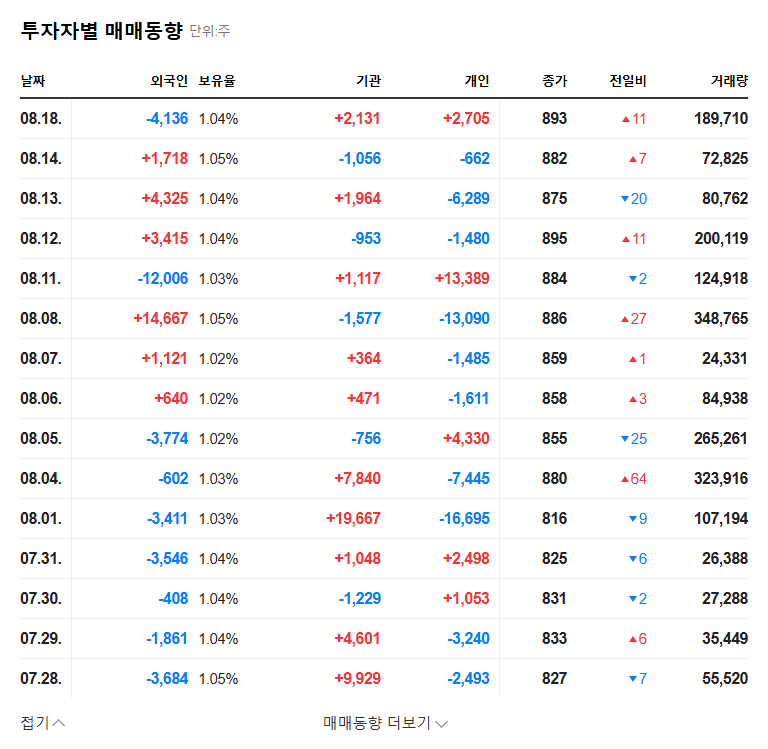

The recent announcement of the HUNEED TECHNOLOGIES Boeing contract has sent ripples through the aerospace and defense investment community. While any partnership with a titan like The Boeing Company is significant, this deal for H-47 avionics equipment requires a nuanced analysis. It represents a potential long-term growth catalyst but arrives amidst concerns over HUNEED’s recent profitability and performance. This comprehensive breakdown will dissect the contract’s details, weigh the strategic advantages against current financial headwinds, and provide a clear outlook for investors considering HUNEED TECHNOLOGIES stock.

Dissecting the H-47 Avionics Deal

On November 14, 2025, HUNEED TECHNOLOGIES formally announced a landmark sales and supply agreement with The Boeing Company. The contract focuses on providing critical avionics equipment for the H-47 Chinook, a world-renowned heavy-lift helicopter. According to the Official Disclosure, the deal is valued at approximately 17.9 billion KRW. The contract is set to span nearly four years, from November 2025 to October 2029.

This figure represents 7.77% of HUNEED’s revenue from the third quarter of 2025, which underscores its importance. While not transformative in the immediate short-term, it provides a stable, long-term revenue stream that strengthens the company’s overseas business division and solidifies its role as a key supplier in the global aerospace supply chain. This move is a clear signal of Boeing’s continued confidence in HUNEED’s technical capabilities.

This contract is more than just a revenue line; it’s a validation of HUNEED’s technology and a cornerstone for future international collaboration and growth in the competitive H-47 avionics market.

Strategic Implications: Why This Boeing Contract Matters

The long-term strategic value of this partnership extends far beyond the initial contract value. For HUNEED TECHNOLOGIES, this is a multi-faceted victory that positions the company for sustained growth and enhanced market credibility.

- •Revenue Stability: The nearly four-year duration ensures a predictable revenue stream, helping to smooth out the cyclical volatility often seen in the defense sector.

- •Enhanced Credibility: Securing a contract for a critical platform like the Boeing H-47 Chinook validates HUNEED’s technological prowess on a global stage, opening doors for future high-value opportunities with other major aerospace players.

- •Portfolio Diversification: This deal complements existing projects like the F-15EX avionics supply, strengthening HUNEED’s aerospace electronics portfolio and reducing reliance on any single project or domestic defense contracts.

- •Improved Investor Sentiment: Large-scale, long-term contracts are powerful signals to the market, capable of attracting investor attention and providing positive momentum for HUNEED stock analysis.

A Reality Check: Navigating Current Financial Headwinds

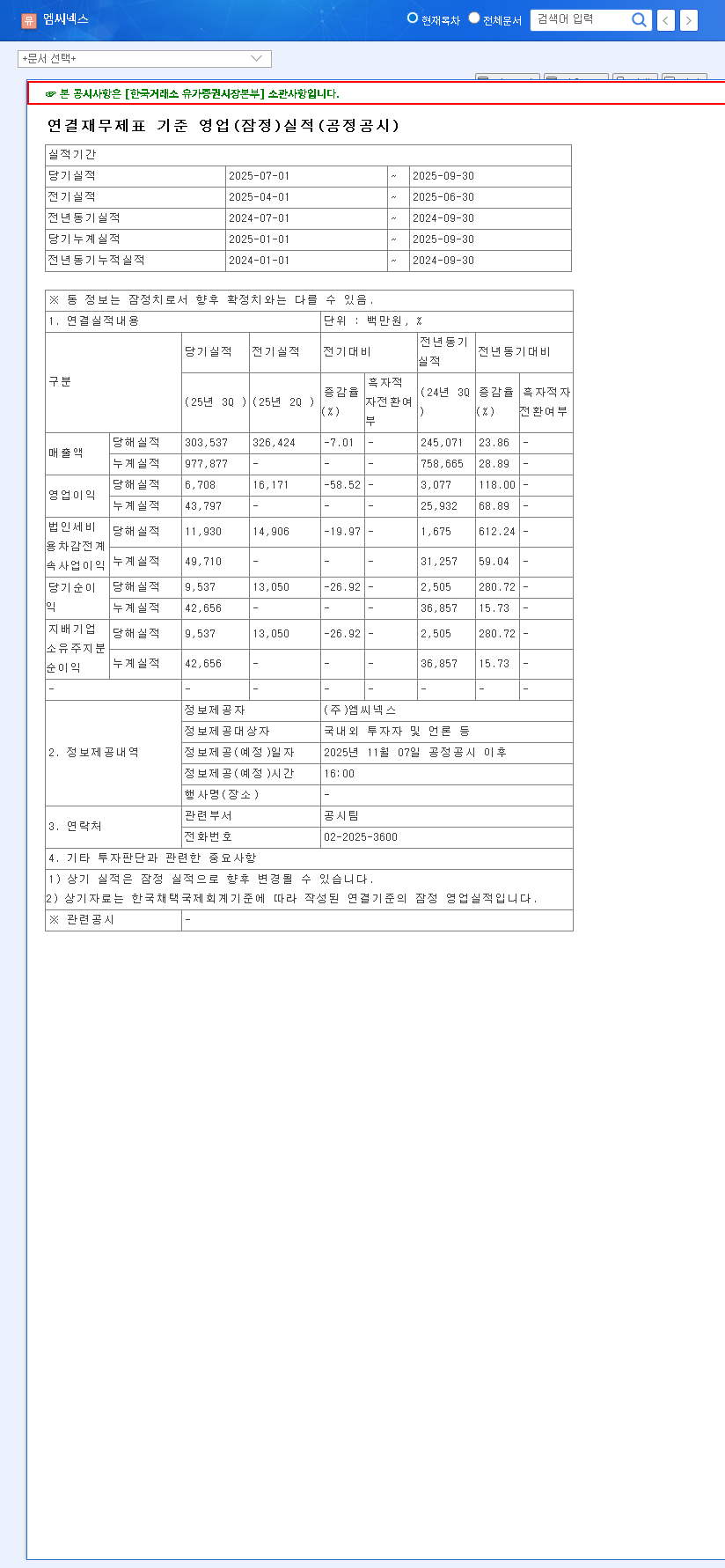

Despite the optimism surrounding the HUNEED TECHNOLOGIES Boeing contract, investors must consider the company’s recent financial performance. The Q3 2025 report painted a challenging picture, revealing a significant deterioration in profitability even as revenues saw a modest increase.

Profitability Under Pressure

Both of HUNEED’s core divisions faced operating losses. The domestic defense business suffered from sluggish sales and increased costs related to new project investments. More concerningly, the overseas business division, where the new Boeing contract resides, also slipped into a deficit. This raises questions about the profitability of the new deal, as its specific terms are undisclosed. Continuous monitoring will be essential to see if this contract can reverse the trend of declining margins.

Financial and Macroeconomic Risks

The company’s balance sheet shows rising long-term debt and weakening operating cash flow, which could constrain future investments. While a high R&D investment ratio (9.54% of revenue) is promising for long-term innovation, it puts additional pressure on short-term profitability. Furthermore, macroeconomic factors like exchange rate volatility and rising interest rates could impact costs and earnings, adding another layer of uncertainty. For a deeper look, consider our comprehensive guide to the aerospace defense sector.

Investor Outlook: A Prudent Path Forward

The HUNEED TECHNOLOGIES Boeing contract is undoubtedly a long-term positive. However, a prudent investment strategy must balance this future potential against present challenges.

For short-term investors, caution is advised. While the announcement may create a temporary stock price bump, the underlying financial weakness and limited immediate revenue impact suggest potential for volatility.

For mid-to-long-term investors, the focus should be on key performance indicators. Watch for tangible signs of profitability improvement in the overseas division in upcoming quarterly reports. The ability to secure additional large-scale orders and translate R&D spending into new revenue-generating products will be the ultimate test of the company’s growth trajectory. This contract is a promising new chapter, but the story of HUNEED’s turnaround is one that will unfold over several quarters, not overnight.