The latest OPTICIS Q3 2025 earnings report has sparked considerable discussion among investors. The preliminary figures indicate a sequential slowdown, raising questions about the company’s robust growth trajectory. Is this a temporary hiccup, a sign of ‘growth pains’ in a volatile market, or the beginning of a more significant trend? This in-depth OPTICIS stock analysis will dissect the preliminary earnings, evaluate the company’s core fundamentals, and provide a strategic outlook for investors.

Dissecting the OPTICIS Q3 2025 Preliminary Earnings Report

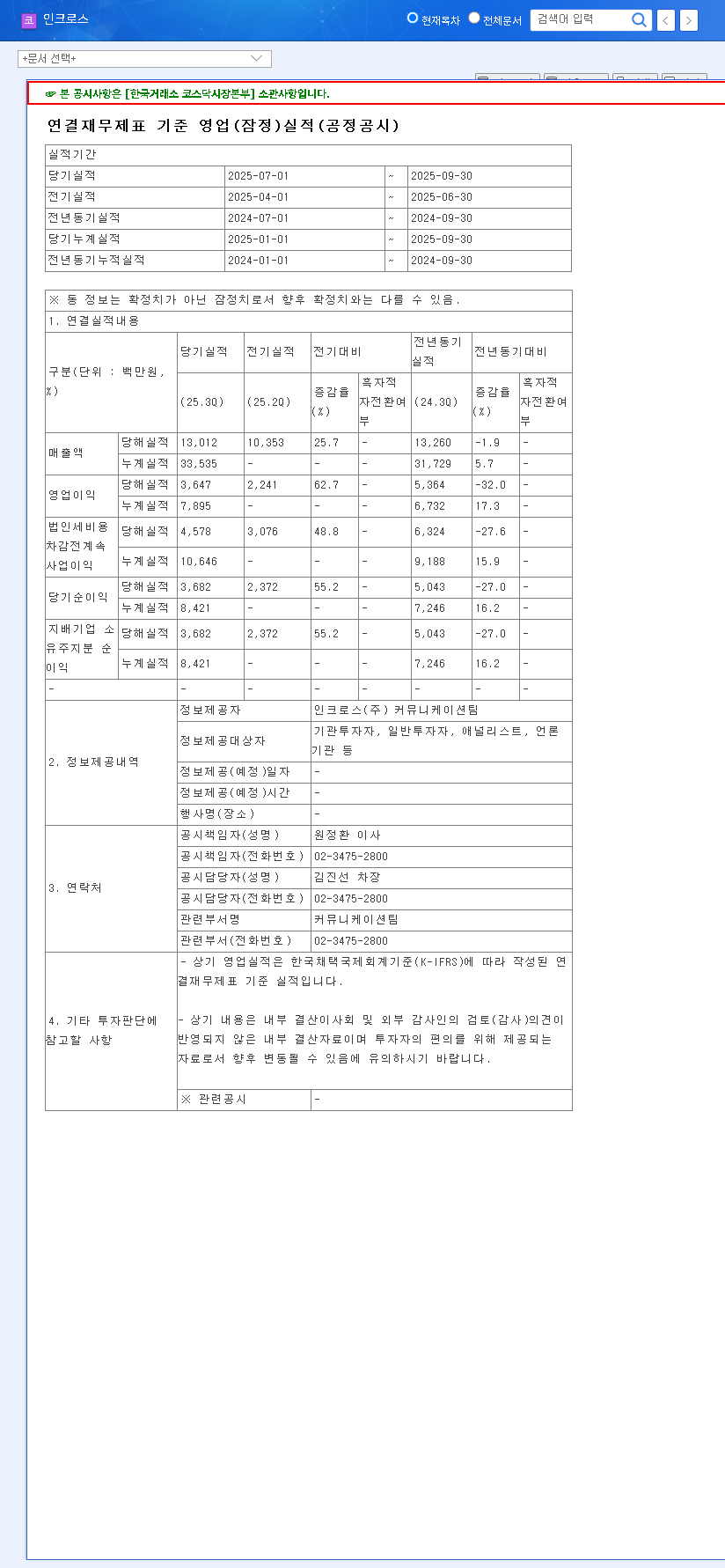

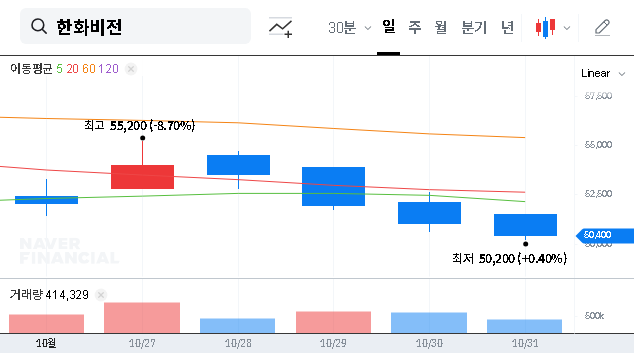

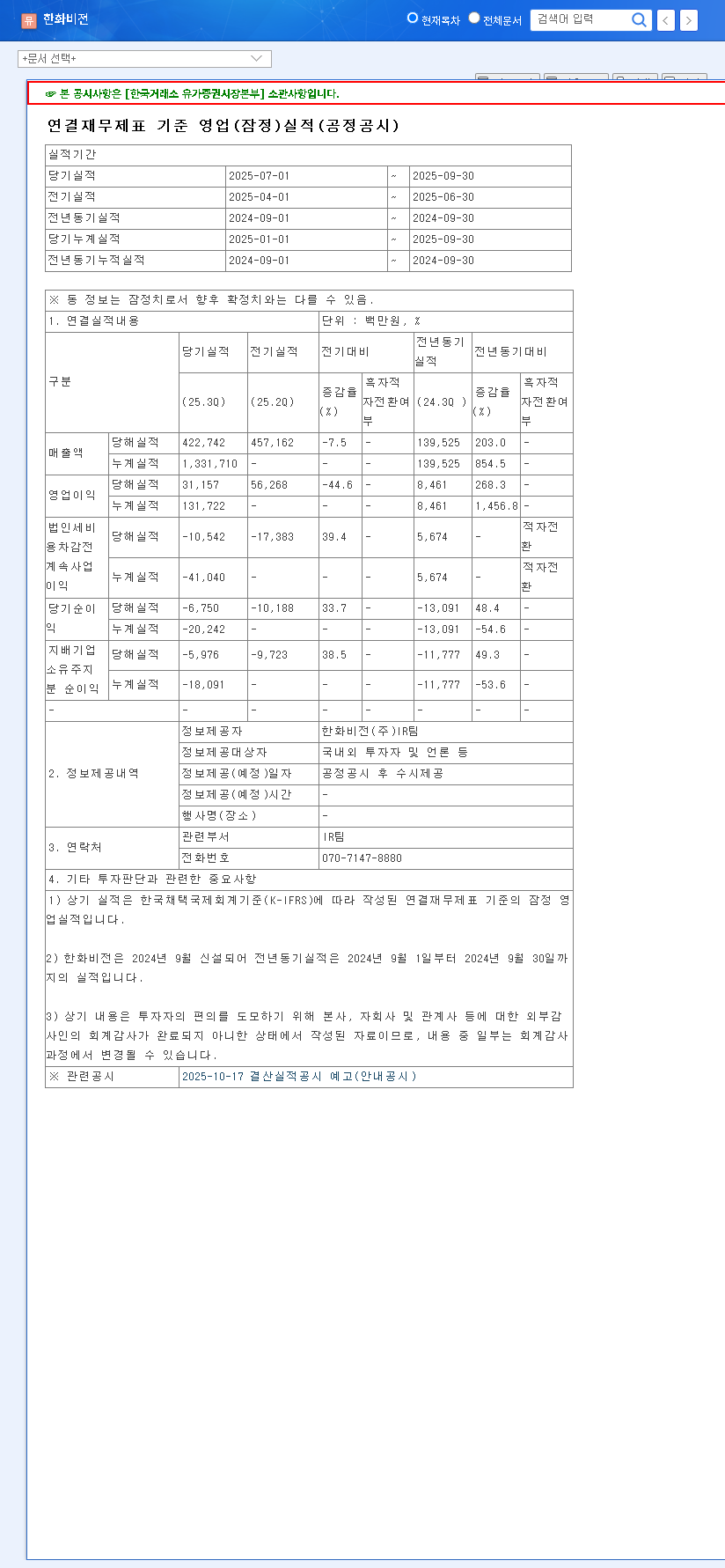

On November 13, 2025, OPTICIS CO., LTD. released its preliminary financial results for the third quarter. The headline numbers, when compared to the strong performance in Q2 2025, show a noticeable contraction. The full details can be reviewed in the company’s Official Disclosure on the DART system.

Key Financial Metrics (Q3 2025)

- •Revenue: KRW 5.1 billion (down from KRW 7.5 billion in Q2 2025)

- •Operating Profit: KRW 0.7 billion (down from KRW 1.6 billion in Q2 2025)

- •Net Income: KRW 1.3 billion (up from KRW 0.8 billion in Q2 2025)

The sharp decrease in both revenue and operating profit is the primary concern for investors. However, the surprising increase in net income suggests that non-operating factors, such as gains from financial assets, played a significant role during the quarter. This divergence warrants a closer look beyond the top-line figures.

While the quarter-over-quarter slowdown may cause short-term market apprehension, it’s crucial to weigh this against the company’s formidable financial health and long-term technological advantages.

Core Strengths: Why OPTICIS Remains a Compelling Story

Despite the Q3 dip, the foundational strengths of OPTICIS have not changed. A comprehensive OPTICIS stock analysis must consider these long-term value drivers, which provide a buffer against temporary market headwinds.

Exceptional Financial Stability

Based on its H1 2025 report, OPTICIS maintains a fortress-like balance sheet. A debt-to-equity ratio of just 7.07% and a current ratio exceeding 1,000% demonstrate outstanding financial soundness and liquidity. This stability allows the company to navigate economic downturns and continue investing in R&D without financial strain.

Leading Technology in High-Growth Sectors

OPTICIS is a key player in the high-speed optical transmission market, a critical technology for several expanding industries. With an export ratio of 78%, its global competitiveness is proven. The company’s proprietary technologies, including VCSEL, high-speed optical circuits, and advanced packaging, are protected by 65 intellectual property rights. This technological moat is crucial as demand surges in markets such as:

- •4K/8K Displays: The core market where high-bandwidth video transmission is essential.

- •Medical Imaging: For high-resolution, real-time data transfer in operating rooms and diagnostics.

- •Automotive & Railway: Growing demand for reliable data links in advanced driver-assistance systems (ADAS) and transportation control.

The company’s commitment to innovation is evident in its R&D spending, which accounts for over 9% of revenue. For a deeper look at the underlying technology, see our complete guide to optical transmission solutions.

Investor Action Plan & Future Outlook

The market’s reaction to the OPTICIS Q3 2025 earnings may create short-term price volatility. However, savvy investors should look beyond the immediate numbers and focus on the strategic picture. This report offers a chance to re-evaluate a long-term position.

Key Indicators to Monitor Moving Forward

- •Q4 Guidance and Performance: The most critical question is whether Q3 was an anomaly. Watch closely for management commentary and the Q4 report to see if growth momentum is restored.

- •New Market Penetration: Track announcements and progress related to new contracts or design wins in the medical, automotive, or industrial sectors. These are key drivers for diversification and future growth.

- •Macroeconomic Factors: As a major exporter, OPTICIS is sensitive to currency fluctuations. The current depreciation of the Won could be a tailwind, but global high-interest rates and economic uncertainty remain risks, as noted by global economic analysts.

In conclusion, while the Q3 preliminary earnings were underwhelming, they do not invalidate the long-term investment thesis for OPTICIS. The company’s superior financial health, technological leadership, and exposure to growing markets provide a strong foundation. Prudent investors should use this period to conduct thorough due diligence rather than making reactive decisions.