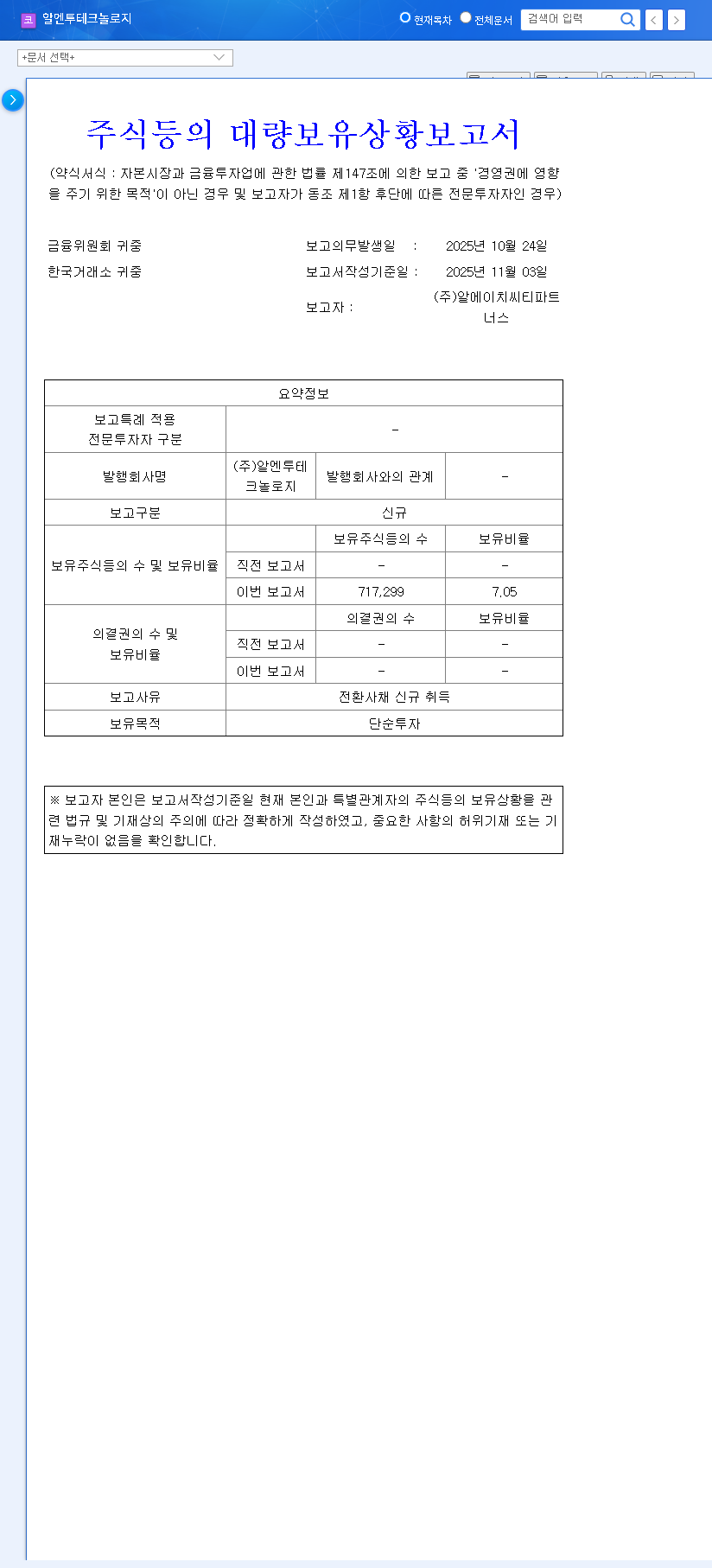

The recent RN2 Technologies capital increase has sent ripples through the investment community. The company recently announced a substantial KRW 11 billion fundraising initiative, positioning itself at a critical juncture. For investors, this raises a pivotal question: is this a strategic masterstroke to fuel next-generation growth, or will the resulting share dilution exert downward pressure on the stock? This comprehensive RN2 Technologies analysis will dissect the implications of this financial move, exploring its impact on the company’s ventures into secondary batteries, 6G communication, and power semiconductors to provide you with the insights needed for an informed decision.

The Anatomy of the Capital Injection

On November 10, 2025, RN2 Technologies formalized its plan for a third-party allotment capital increase, securing significant funding for its future endeavors. The full details of this financial event were disclosed in an official filing (Official Disclosure). Here are the essential details:

- •Total Funding: Approximately KRW 11 billion.

- •Shares Issued: 1,797,385 new common shares.

- •Issue Price: KRW 6,120 per share.

- •Primary Investor: Newjin No. 1 Fund.

- •Key Dates: Payment is scheduled for November 26, 2025, with the new shares expected to be listed on December 12, 2025.

This move is designed to inject vital capital directly into the company, bypassing public offerings to partner with a strategic investor. The participation of ‘Newjin No. 1 Fund’ can be seen as a vote of confidence in the company’s long-term vision and growth trajectory.

Deep Dive: The Impact of the RN2 Technologies Capital Increase

A Company at a Crossroads: Growth vs. Profitability

RN2 Technologies’ recent performance paints a picture of a company in transition. While sales grew an impressive 36.4% year-on-year to KRW 9.168 billion in the first half of 2025, the company recorded an operating deficit of KRW 1.046 billion. This loss is not from a lack of demand but rather a strategic decision to heavily invest in R&D and new business initiatives, coupled with a temporary slowdown in the 5G market. This capital increase is therefore a proactive measure to fortify its financial foundation and aggressively pursue its high-growth ambitions without being constrained by short-term profitability pressures.

The core challenge for RN2 is balancing the short-term stock dilution against the long-term, transformative potential of its investments in next-generation technologies.

Fueling the Future: Where is the Money Going?

The KRW 11 billion is earmarked for what the company believes are its key future growth drivers. These sectors are not just promising; they are set to redefine global industry:

- •Secondary Batteries & E-Mobility: The company is targeting critical components like electrolyte materials for all-solid-state batteries—a holy grail for creating safer, more energy-dense power sources for electric vehicles. Success here could position RN2 as a key supplier in the booming EV market. For more on market trends, see our guide to investing in emerging technologies.

- •6G Communication Technology: Building on its 5G expertise, RN2 is investing in the infrastructure for 6G. This next wave of connectivity promises to enable the Internet of Things (IoT), autonomous vehicles, and artificial intelligence on an unprecedented scale, a market valued in the trillions.

- •Power Semiconductor Substrates: These components are vital for managing power efficiently in EVs and data centers. As the world electrifies, the demand for advanced heat-dissipating substrates is soaring, as noted by industry analysts at firms like Gartner.

Investor Strategy: Navigating the Road Ahead

The RN2 Technologies capital increase presents both opportunities and risks. A prudent investment strategy requires a clear understanding of both sides of the coin.

The Short-Term View: Caution Advised

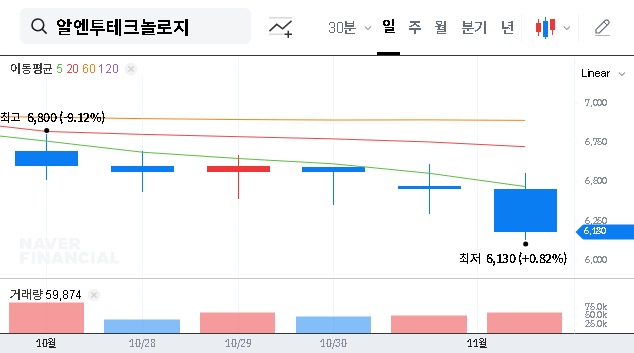

The issuance of nearly 1.8 million new shares represents a dilution of approximately 19% for existing shareholders. This increase in supply can create short-term downward pressure on the RN2 Technologies stock price, especially around the listing date of December 12, 2025. Traders should monitor price action and volume closely during this period for signs of absorption or further selling.

The Long-Term View: A Bet on Execution

For long-term investors, the focus should be on the company’s ability to execute its strategic vision. The capital provides the necessary runway. The key will be translating these funds into tangible results: securing patents, signing pilot projects, or landing supply agreements in their target sectors. The success of the RN2 Technologies stock over the next 2-3 years will depend almost entirely on the progress made in these new ventures.

Frequently Asked Questions

What is the size of the capital increase?

RN2 Technologies is raising approximately KRW 11 billion by issuing 1,797,385 new common shares.

What are RN2 Technologies’ new business areas?

The company is focusing on high-growth sectors: secondary battery materials (all-solid-state electrolytes), 6G communication technology, and power semiconductor heat dissipation substrates.

What is the short-term risk for the stock price?

The primary short-term risk is share dilution. The new shares increase the total outstanding amount by about 19%, which could lead to downward price pressure as the market absorbs the new supply.

In conclusion, this capital increase is a bold, forward-looking move for RN2 Technologies. It’s an investment in a potentially transformative future. While investors must navigate the immediate challenges of stock dilution, the long-term prize is significant if the company can successfully innovate and capture market share in these next-generation industries.