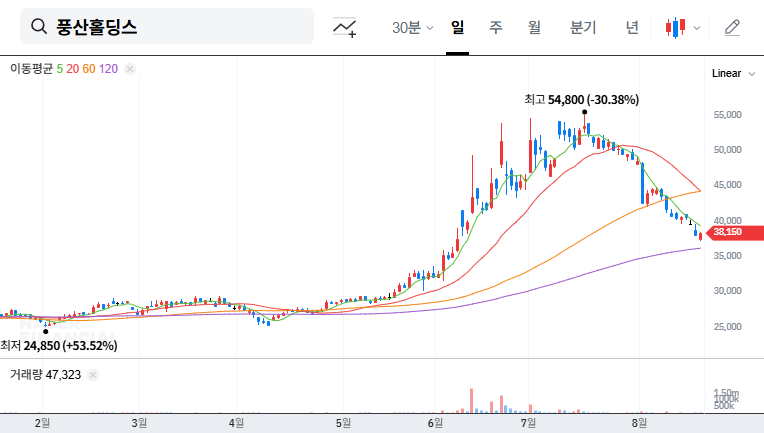

The provisional Q3 2025 earnings report from POONGSAN HOLDINGS CORPORATION (풍산홀딩스) sent a ripple of concern through the investment community. The announced figures fell significantly short of market consensus, raising critical questions: What drove this underperformance? What is the outlook for Poongsan’s stock price, and what strategic adjustments should investors consider now? This in-depth analysis unpacks the latest financial results, explores the underlying fundamentals, and provides a clear roadmap for navigating the path ahead.

The Q3 2025 Earnings Shock: By the Numbers

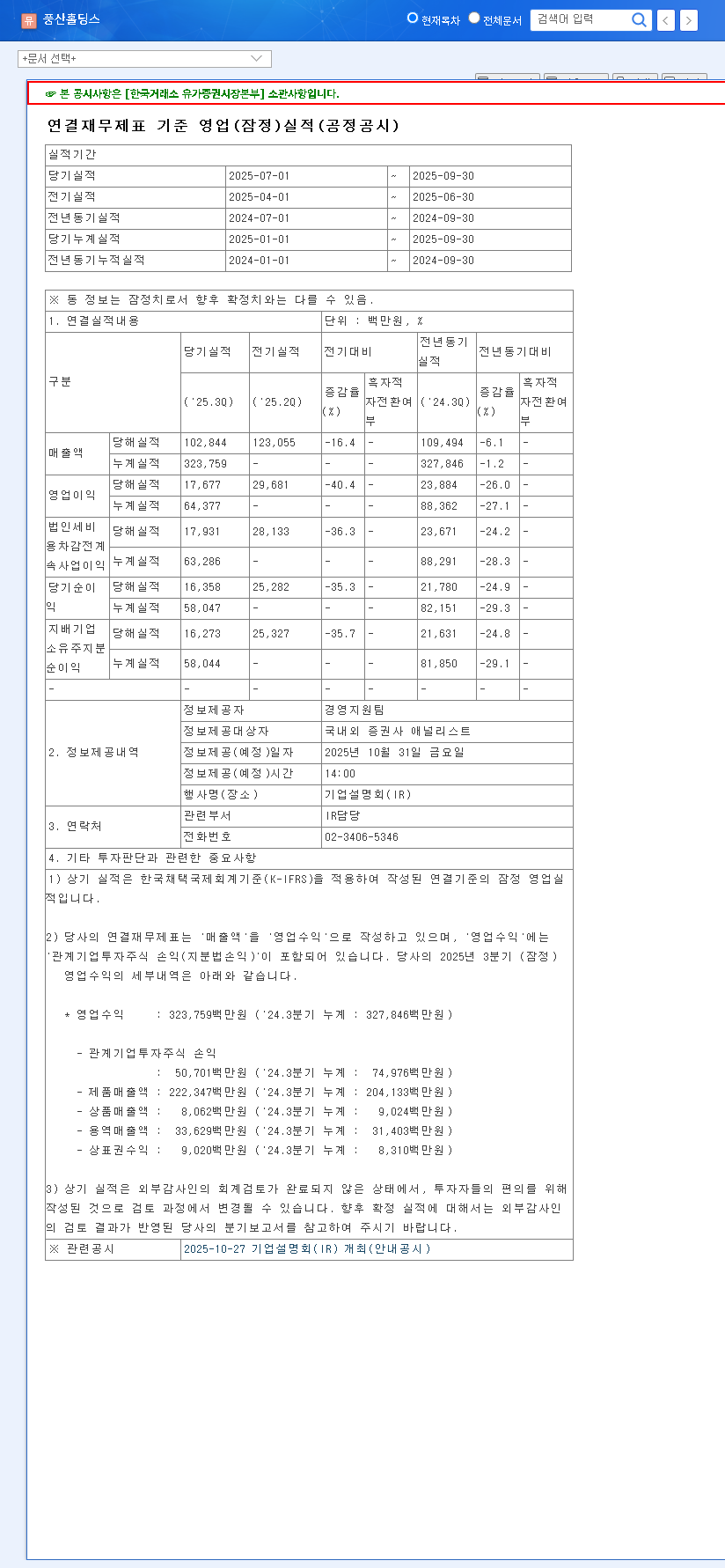

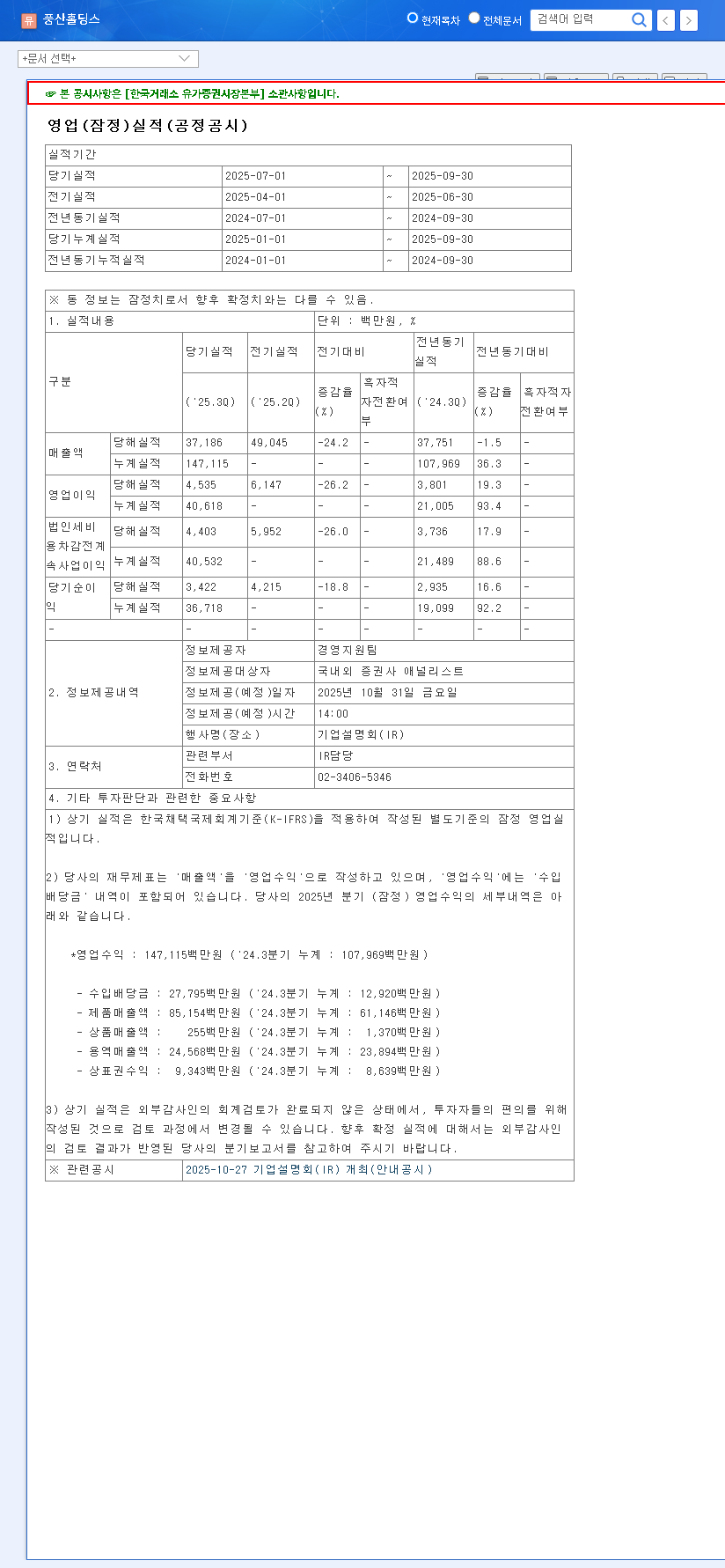

POONGSAN HOLDINGS CORPORATION delivered what can only be described as an earnings shock for the third quarter of 2025. The consolidated results revealed a considerable gap between performance and market expectations, immediately souring investor sentiment. For a complete breakdown, investors can review the Official Disclosure filed with DART.

Provisional Q3 2025 Consolidated Results:

• Revenue: 102.8 billion KRW (approx. 10% below estimates of 114.2 billion KRW)

• Operating Profit: 17.7 billion KRW (approx. 17% below estimates of 21.2 billion KRW)

• Net Profit: 16.3 billion KRW

These figures not only represent a significant miss on analyst projections but also show a sharp decline from the preceding quarter (Q2 2025), which saw revenues of 123.1 billion KRW and an operating profit of 29.7 billion KRW. This signals a potential reversal of momentum that requires careful examination.

Dissecting the Disappointment: Key Factors Behind the Miss

Subsidiary Struggles & Raw Material Headwinds

A core reason for the consolidated underperformance stems from specific subsidiaries. Poongsan Special Metal Co., Ltd. faced significant challenges, negatively impacting overall profitability. This was compounded by revenue declines at other overseas subsidiaries, including PMX Industries, Inc. and Siam Poongsan Metal Co., Ltd. Furthermore, volatility in key raw material prices, particularly the declining outlook for nickel, has squeezed margins and created an unpredictable operating environment. These internal challenges were exacerbated by a notable rise in the consolidated debt-to-equity ratio to 5.94%, raising flags about financial health management.

Mounting Macroeconomic Pressures

The performance of POONGSAN HOLDINGS CORPORATION cannot be viewed in a vacuum. The broader global economic landscape is fraught with challenges that directly impact its business. These external headwinds include:

- •Global Economic Slowdown: Persistent inflation and monetary tightening policies across the globe are dampening industrial demand. For more on this trend, see analysis from authoritative sources like Reuters Economic Outlook.

- •Rising Interest Rates: Higher borrowing costs increase the financial burden on the company, potentially limiting future capital expenditures and pressuring the bottom line.

- •Currency and Freight Volatility: Fluctuations in exchange rates and shipping costs, such as the China Containerized Freight Index, create uncertainty in both revenue from overseas sales and costs for imported raw materials.

The Silver Lining: Strengths and Rebound Potential

Despite the concerning Q3 results, a comprehensive Poongsan stock analysis reveals significant underlying strengths that provide a pathway for a future rebound.

The Powerhouse Defense Sector

The brightest spot in the portfolio is the subsidiary Poongsan Co., Ltd., particularly its defense division. This segment continues to exhibit robust year-over-year revenue growth. Fueled by rising geopolitical tensions and the impressive global expansion of K-defense exports, this division acts as a powerful and reliable growth engine for the entire holding company. Continued investment in its defense production facilities solidifies this long-term positive momentum.

Strategic Investments and Financial Stability

While the debt ratio has risen, the company maintains a substantial capital base, with consolidated total equity of 1,118.319 billion KRW. This provides a stable foundation from which to navigate the current turbulence. Ongoing investments into the core copper alloy (Shin-dong) and defense sectors are designed to secure future profitability and market share. For a deeper dive into market dynamics, you can read our guide on understanding the copper market’s impact on industrial stocks.

A Prudent Investor’s Guide for POONGSAN HOLDINGS CORPORATION

Given the short-term headwinds and long-term potential, a cautious and informed approach is essential. The disappointing Poongsan Holdings earnings will inevitably lead to short-term stock price volatility. However, savvy investors should focus on the following key areas:

- •Monitor the Defense Sector: Keep a close eye on the performance and order backlog of Poongsan Co., Ltd.’s defense business. Its sustained growth is the primary catalyst for a stock price recovery.

- •Analyze Company Guidance: Scrutinize future communications from the company to understand if the Q3 issues are transient or indicative of a deeper, structural problem.

- •Assess Financial Health Initiatives: Watch for management’s strategies to address the rising debt-to-equity ratio and improve the financial stability of the consolidated entity.

- •Evaluate Risk Management: Consider how effectively the company is hedging against raw material price swings and currency fluctuations.

Conclusion: ‘Neutral’ Stance with Cautious Optimism

In conclusion, the POONGSAN HOLDINGS CORPORATION Q3 2025 earnings report was undeniably a setback. The combination of underperforming subsidiaries and a challenging macroeconomic environment creates clear short-term risks and downward pressure on the stock. However, this is balanced by the significant, long-term growth potential of its subsidiary’s defense sector, which remains a powerful engine for value creation.

Therefore, a ‘Neutral’ investment opinion is warranted. Investors should brace for immediate market negativity but keep a close watch on the key positive drivers and the company’s strategic responses. The ability of management to navigate these headwinds while capitalizing on the strength of its defense business will determine the trajectory for a mid-to-long-term recovery.