The potential DOOSAN SK Siltron acquisition represents one of the most significant strategic moves in the South Korean market, signaling a potential pivot for the industrial giant into the heart of the high-tech semiconductor industry. In October 2025, reports surfaced that DOOSAN CO., LTD was actively considering acquiring SK Siltron, a global leader in semiconductor silicon wafers. This monumental deal could redefine DOOSAN’s future, but it comes with a complex web of opportunities and risks. This comprehensive analysis will unpack the strategic rationale, financial implications, and critical factors that investors must monitor as this semiconductor M&A story unfolds.

The Official Stance: What We Know So Far

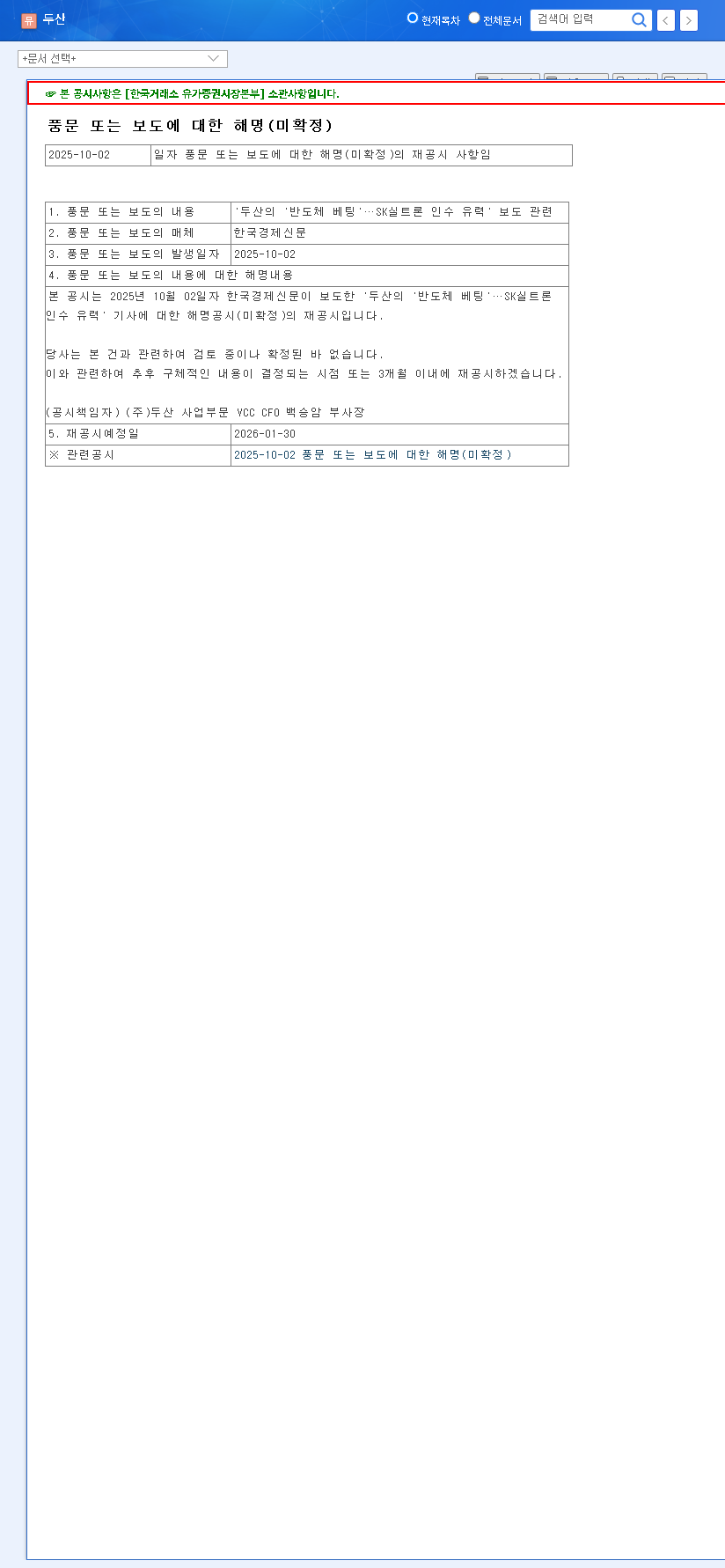

The speculation began in earnest on October 2, 2025, when the Korea Economic Daily reported that a DOOSAN acquisition of SK Siltron was highly probable. The market reacted swiftly, prompting DOOSAN to respond. On October 31, 2025, the company issued a clarifying statement, confirming that the matter was ‘currently under review and not yet confirmed.’ This carefully worded disclosure, which you can view in the Official Disclosure (DART), effectively moved the rumor from speculation to a tangible possibility. DOOSAN has committed to a follow-up announcement within three months, placing this major M&A event squarely on the market’s radar.

The Strategic Prize: Why Acquiring SK Siltron is a Game-Changer

The market’s intense focus on this deal is for good reason. SK Siltron is not just any company; it is a premier manufacturer of silicon wafers, the foundational material upon which virtually all semiconductors are built. In an era defined by the global race for chip supremacy, controlling a key part of the supply chain is a massive strategic advantage. For a deeper understanding of the market dynamics, you can review industry analysis from sources like leading technology market reports.

This isn’t just a diversification play; it’s a bid for relevance in the Fourth Industrial Revolution. Acquiring SK Siltron would transform DOOSAN from an industrial powerhouse into a critical player in the global technology ecosystem.

A Pivot to High-Tech Growth Engines

If the DOOSAN SK Siltron acquisition proceeds, it would mark a historic shift. It would allow DOOSAN to:

- •Secure Future Growth: Break away from the cyclical nature of heavy industries and tap into the sustained, high-growth trajectory of the semiconductor market.

- •Internalize Core Technology: Gain control over a critical component in the tech supply chain, ensuring stability and strengthening its overall technological competitiveness. For more information, you might be interested in our article on Understanding the Semiconductor Supply Chain.

- •Expand Global Influence: Elevate DOOSAN’s brand and market position from a regional industrial leader to a global technology materials supplier.

In-Depth Analysis: Weighing the Opportunities and Risks

While the strategic upside is clear, the path is fraught with significant challenges. A balanced investor analysis requires a sober look at both sides of the coin.

The Upside: Potential for Massive Growth and Synergy

A successful acquisition would bring substantial benefits. SK Siltron is a highly profitable company with a stable revenue stream. Integrating it into the DOOSAN portfolio would immediately boost profitability and improve the conglomerate’s overall financial structure. Furthermore, potential synergies exist with other DOOSAN affiliates in areas like advanced materials, energy solutions for fabrication plants, and precision engineering, which could enhance long-term growth prospects. The company’s recent share buyback program also signals a commitment to shareholder value, which could complement this growth-oriented M&A.

The Downside: Significant Financial and Integration Hurdles

The risks associated with this semiconductor M&A are considerable and must not be underestimated.

- •High Acquisition Cost: Acquiring a prize asset like SK Siltron will command a premium price, potentially straining DOOSAN’s balance sheet, increasing its debt-to-equity ratio, and leading to higher interest expenses.

- •Post-Merger Integration (PMI) Risks: The corporate cultures of a traditional heavy-industry conglomerate and a fast-paced technology materials company are vastly different. A failed or inefficient integration could destroy value and prevent synergies from materializing.

- •Market Volatility: The semiconductor industry is famously cyclical and hyper-competitive. DOOSAN would be entering a market with rapid technological shifts and entrenched global players, requiring continuous and substantial R&D investment.

- •Macroeconomic Headwinds: High interest rates and currency volatility (won/dollar) create an unfavorable environment for large-scale, debt-financed acquisitions, potentially increasing the final cost and financial burden.

Investor Playbook: Key Factors to Watch

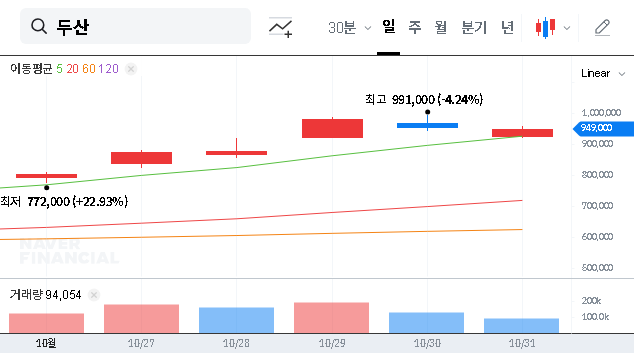

For investors tracking the DOOSAN SK Siltron acquisition, a wait-and-see approach is prudent. Hasty decisions are ill-advised. Instead, focus on the concrete details that will emerge in DOOSAN’s upcoming disclosures. The stock price is likely to remain volatile, reacting to every new piece of information.

Your Monitoring Checklist:

- •Deal Structure: Will DOOSAN acquire alone or via a consortium? How will the deal be financed (cash, debt, equity)?

- •Valuation: What is the final acquisition price and how does it compare to SK Siltron’s valuation metrics?

- •Financial Impact: What is the pro-forma impact on DOOSAN’s debt levels, credit rating, and earnings per share?

- •Synergy & PMI Plan: Does management present a credible and detailed plan for integration and synergy realization?

This potential deal is a defining moment for DOOSAN. A successful execution could unlock immense value, while a misstep could prove costly for years to come. Diligent monitoring of the facts is the best course of action for any serious investor.