SOOP CO., LTD. just released its preliminary Q3 2025 earnings report, presenting a complex picture for investors. While the one-person media giant shattered market expectations on revenue and operating profit, a surprising dip in net income has sparked debate. This in-depth SOOP investment analysis unpacks the critical details behind the numbers, exploring the core growth engines, looming risks, and what this all means for the company’s stock price moving forward.

For those who wish to review the primary data directly, the company’s official filing is publicly available. Official Disclosure: Click to view the DART report.

Unpacking the SOOP CO., LTD. Q3 2025 Earnings Report

Performance vs. Market Expectations: A Mixed Bag

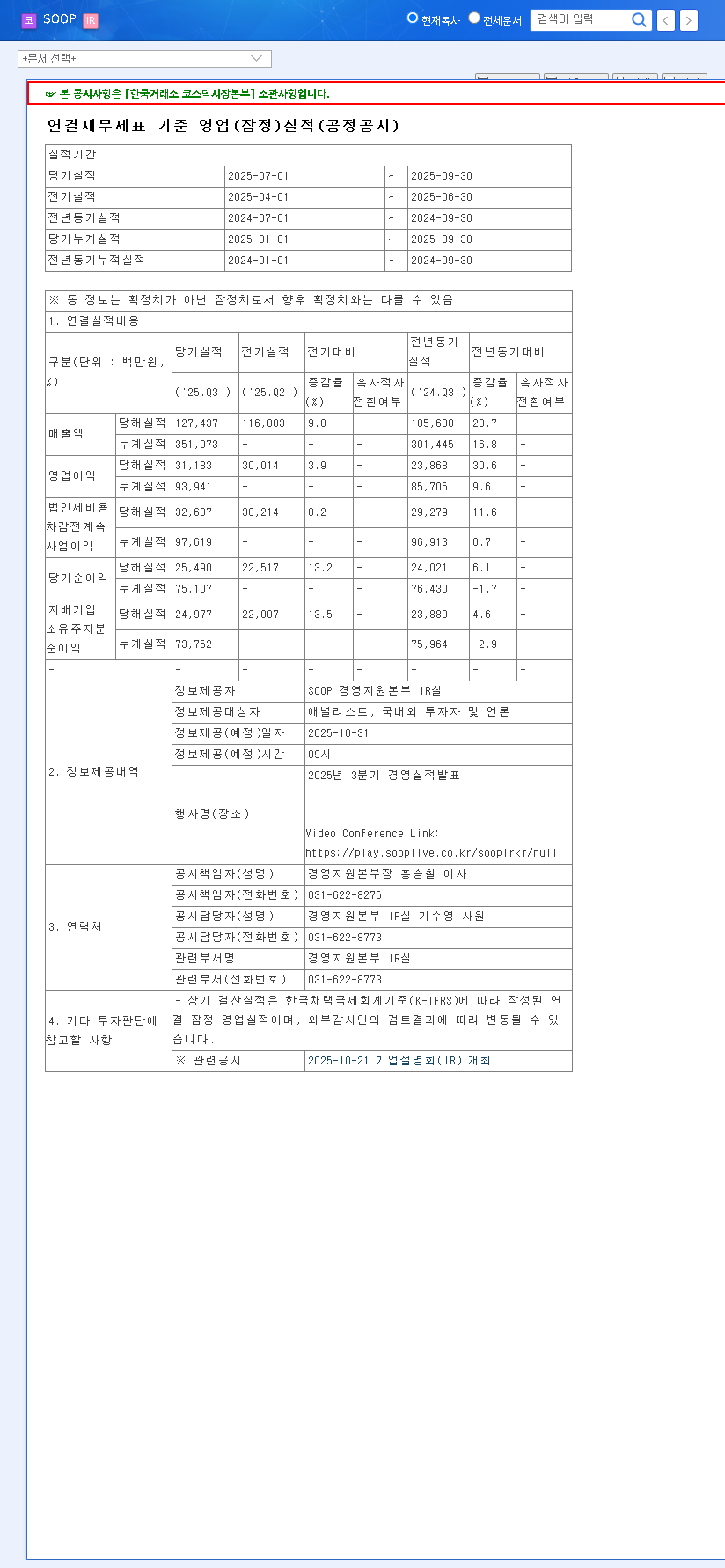

The initial headline from the SOOP CO., LTD. Q3 2025 earnings announcement was one of triumphant top-line growth coupled with a concerning bottom-line miss. Here’s a direct comparison of the preliminary results against consensus market forecasts:

- •Revenue: KRW 127.4 billion, beating expectations of KRW 120.7 billion by a significant +6%.

- •Operating Profit: KRW 31.2 billion, narrowly surpassing the forecast of KRW 30.8 billion by +1%.

- •Net Income: KRW 25.0 billion, falling short of the expected KRW 26.2 billion by -5%.

This dichotomy is key: while the company’s core operations are clearly firing on all cylinders, non-operating factors or rising costs below the operating line are pressuring overall profitability.

Year-Over-Year Financial Momentum

Looking at the year-over-year figures reveals a powerful growth story. The strong performance in SOOP revenue and profit highlights the company’s expanding market position:

- •Revenue Growth: A robust 15.8% increase year-over-year, primarily fueled by the growing user base on its flagship ‘SOOP’ platform and the successful integration of its advertising arm, PlayD Co., Ltd.

- •Operating Profit Surge: An impressive 30.5% jump year-over-year, showcasing excellent operational leverage and effective cost management strategies.

- •Net Income Lag: Despite the strong operational results, net income only grew by a modest 4.2%. This lag is likely attributable to non-operating factors, such as foreign exchange losses, virtual asset valuation changes, or a higher effective tax rate.

Growth Drivers and Potential Headwinds

Core Strengths Fueling SOOP’s Ascent

SOOP’s foundation remains incredibly strong, built on a loyal user base and smart strategic acquisitions. These are the pillars of its current success:

- •Dominant Platform: The core ‘SOOP’ platform, which constitutes over 75% of total revenue, continues to exhibit strong user engagement and monetization.

- •Advertising Synergy: The acquisition of PlayD Co., Ltd. is now paying significant dividends. Advertising and content production revenue soared by an incredible 63.5% YoY, proving the synergy thesis.

- •Strategic Diversification: Investments into niche sports content like esports and billiards, plus the launch of ‘SOOP Global’, demonstrate a clear strategy to build long-term, diversified growth engines beyond its home market.

- •Financial Fortitude: With a low debt-to-equity ratio of just 30% and a healthy Return on Equity (ROE), the company’s balance sheet is rock-solid.

Key Risk Factors Investors Must Monitor

Despite the positive momentum, several risks could impact the SOOP stock price. Prudent investors should keep these factors on their radar:

- •Virtual Asset Volatility: The company’s holdings of USDT expose it to the inherent volatility of the cryptocurrency market. Fluctuations in value can create unpredictable swings in non-operating profit and loss.

- •Subsidiary Dependence: As PlayD Co., Ltd.’s advertising business becomes a larger contributor to growth, SOOP’s overall performance becomes more sensitive to competition and client concentration within the digital ad space.

- •Regulatory Scrutiny (SFC Sanctions): The recent fine and designation of an auditor for three years by the Securities and Futures Commission for accounting violations is a significant reputational risk that could temporarily dampen investor confidence.

Investment Outlook and Strategic Recommendation

Considering the strong operational performance balanced by clear risks and a net income miss, a cautious but optimistic stance is warranted. The growth in media platform earnings is undeniable, but the external pressures cannot be ignored. For context on historical performance, investors can review our Q2 2025 SOOP earnings analysis.

Final Verdict: Maintain ‘Neutral’ with a Positive Bias

We are maintaining a ‘Neutral’ investment opinion on SOOP CO., LTD. at this time. The powerful growth in the core platform and advertising segments is a compelling reason to be bullish, but the combination of the net income shortfall, virtual asset risk, and regulatory overhang necessitates a degree of caution.

Investors should closely monitor the following developments in the coming quarters:

- •Improvement in net income and profit margins.

- •Sustained growth momentum from the PlayD advertising division.

- •Tangible results from the ‘SOOP Global’ expansion, particularly user acquisition and monetization metrics.

- •Any further updates or long-term impacts from the SFC sanctions.

While SOOP’s fundamentals are sound, a patient and watchful approach is the most prudent strategy until there is more clarity on the factors that pressured its Q3 net income. Broader market trends, such as those covered by major financial news sources like Reuters, will also play a role in investor sentiment.