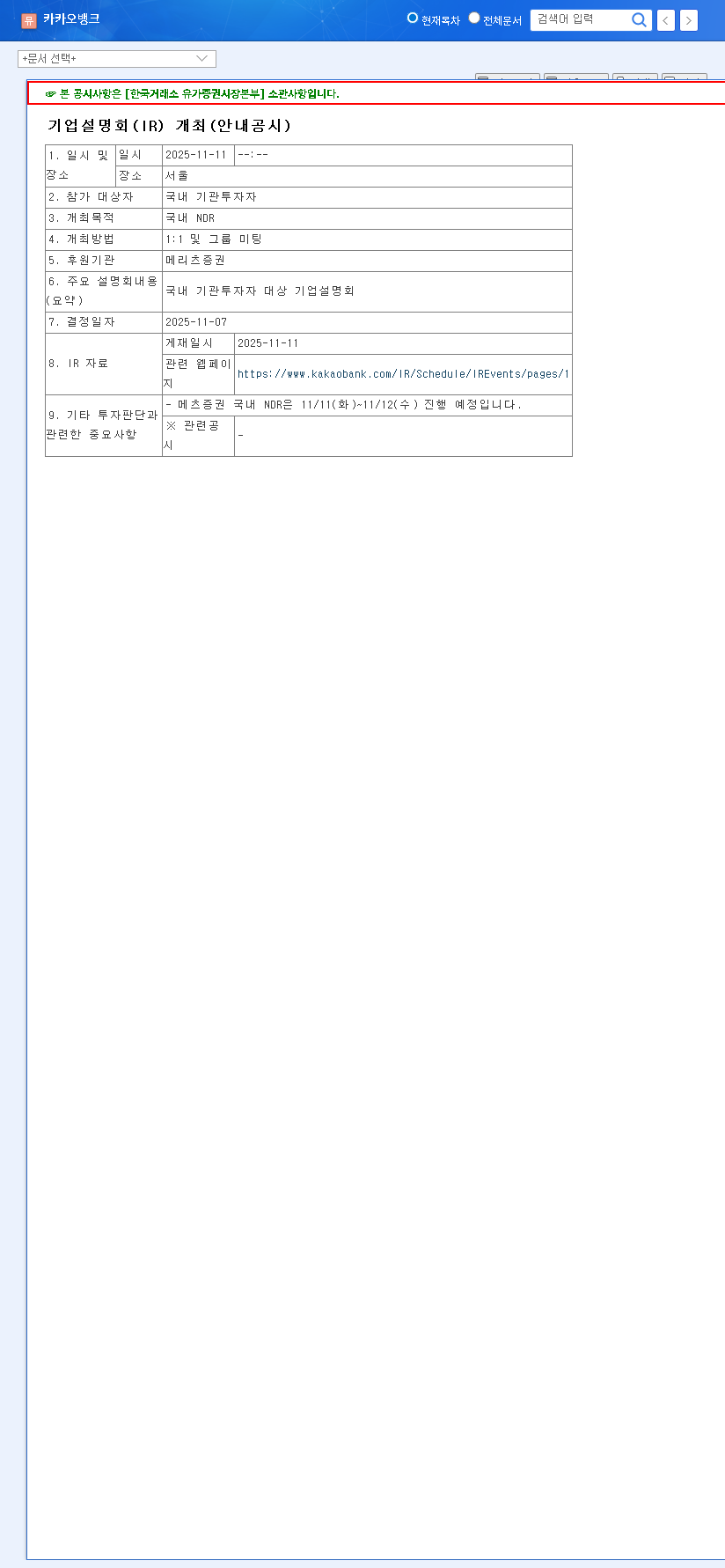

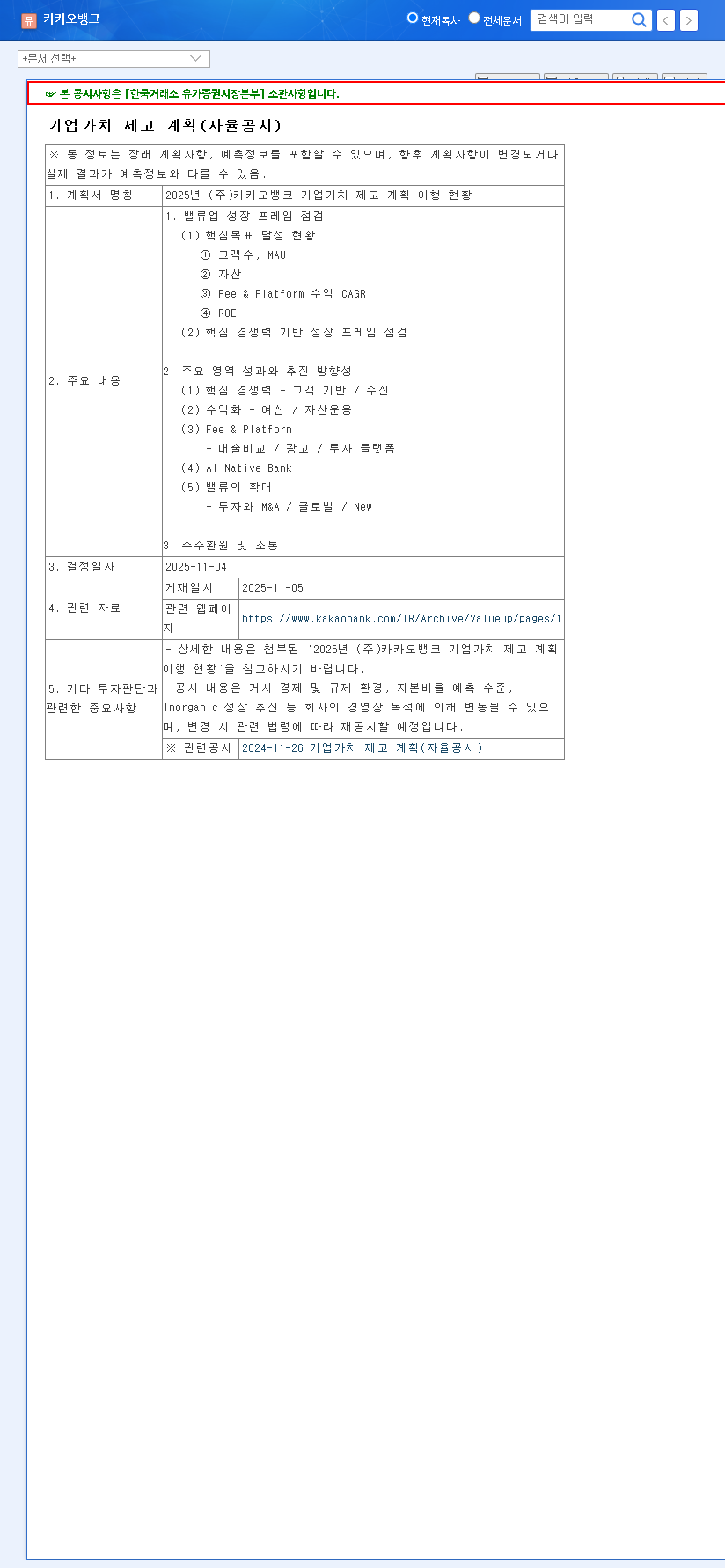

The recent KakaoBank Corp. NDR (Non-Deal Roadshow) for international institutional investors marks a pivotal moment for South Korea’s leading digital finance powerhouse. This strategic event, held on November 17, 2025, is more than a simple presentation; it’s a calculated move to showcase the company’s robust value proposition and ambitious future growth strategy to a global audience. For investors, understanding the nuances of this roadshow is key to unlocking insights into KakaoBank’s stock potential and its long-term trajectory in the competitive fintech landscape. This event was formally announced in an Official Disclosure, underscoring its significance.

In this comprehensive analysis, we will deconstruct the core pillars of KakaoBank’s appeal, from its formidable fundamentals and AI-driven innovations to its platform expansion strategies. We’ll also explore the potential impacts of the NDR on corporate value and provide a strategic outlook for prudent investors.

Deconstructing KakaoBank’s Core Strengths

To captivate global investors, KakaoBank is highlighting a trifecta of strengths: a massive user base, technological leadership, and impeccable financial health. These are not just talking points; they are the foundational columns supporting its entire growth narrative.

1. Unparalleled Customer Base & Platform Dominance

KakaoBank’s growth is fundamentally anchored by its vast and highly engaged user base. With over 20 million Monthly Active Users (MAU) and total deposits soaring to KRW 65.7 trillion, the bank has achieved a scale that traditional institutions envy. This success is a direct result of its hyper-focus on a seamless user experience (UX/UI) and innovative product development. The platform’s expansion into brokerage services (7.07 million accounts) and loan comparison platforms further solidifies its ecosystem, creating multiple revenue streams and increasing customer lifetime value. For a deeper look at market trends, see this fintech industry analysis.

2. Pioneering AI in Digital Finance

A key focus of the KakaoBank Corp. NDR is its leadership in Artificial Intelligence. The bank is embedding AI across its services to enhance both security and customer convenience. Innovations like ‘AI Smishing Message Verification’ protect users from fraud, while ‘AI Search’ and ‘AI Financial Calculators’ provide personalized and intuitive experiences. This commitment to technology is not just about improving existing services; it’s about building a future-proof banking platform that can adapt and lead in the fast-evolving world of digital finance.

“The future of banking isn’t in physical branches; it’s in the palm of your hand, powered by intelligent, data-driven platforms that anticipate your needs. This is the competitive edge that tech-first institutions like KakaoBank are building.”

3. A Fortress of Financial Stability

Despite its rapid growth, KakaoBank maintains exceptional financial health. Its BIS total capital ratio of 23.85% significantly exceeds regulatory requirements, signaling a stable and well-managed financial position. Furthermore, its ability to attract low-cost demand deposits (83.96% of total) provides a substantial competitive advantage, lowering its cost of funding and boosting profitability. This financial prudence is a critical message for risk-averse international investors.

Navigating the Headwinds: Risks and Challenges

While the outlook is promising, investors must consider potential risks. The South Korean market is facing intensifying competition, with the potential entry of new internet-only banks and the aggressive expansion of other big tech players. Additionally, macroeconomic uncertainties, including rising household debt and currency volatility, could impact loan quality and overall profitability. Careful management of its corporate loan portfolio will be crucial in navigating these challenges.

Impact of the NDR on KakaoBank Stock

A successful NDR can serve as a powerful catalyst for KakaoBank stock. By clearly communicating its KakaoBank growth strategy and building trust, the company can attract significant foreign investment, leading to positive stock price momentum. However, there are potential downsides. If the presentation fails to meet lofty market expectations, it could trigger a sell-off. As with any investment, a prudent approach is necessary, and further research can be found in our detailed market overview.

Investment Outlook: Key Considerations

For those considering an investment in KakaoBank, the post-NDR period will be critical for observation. We recommend focusing on the following areas:

- •International Investor Reaction: Monitor reports and analyst ratings from global institutions following the KakaoBank Corp. NDR to gauge sentiment.

- •AI Service Monetization: Track the actual revenue contribution and performance metrics of new AI-based financial products.

- •Platform Growth Metrics: Continue to assess the expansion and monetization of its platform businesses, such as brokerage and loan comparisons.

- •Macroeconomic Indicators: Stay informed about changes in interest rates and exchange rates that could impact KakaoBank’s fundamentals.

In conclusion, the KakaoBank Corp. NDR is a crucial step in its journey to become a global fintech leader. By effectively showcasing its strengths and future vision, the company has the potential to unlock significant corporate value and deliver long-term returns for discerning investors.