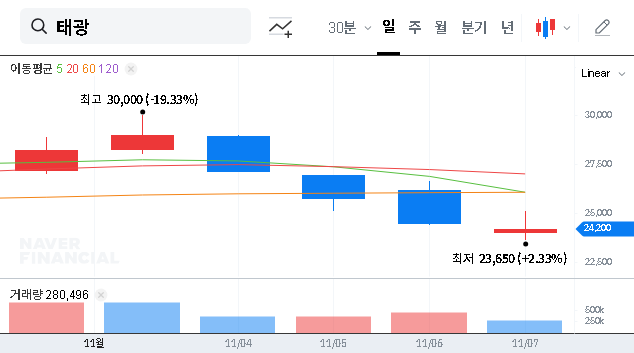

The latest movements in T. K. CORPORATION stock have caught the eye of astute market watchers. A significant development has emerged as Bearing Asset Management, a notable institutional investor, announced it has acquired an additional 1% stake in the leading plant equipment manufacturer. While the official purpose is cited as a ‘simple investment,’ this action prompts a crucial question: Is this merely a passive portfolio adjustment, or does it signal a deeper confidence in the company’s future? This comprehensive T. K. CORPORATION stock analysis will explore the implications of this move, dissect the company’s current financial health, and provide a forward-looking investment outlook.

Decoding Bearing Asset Management’s Strategic Move

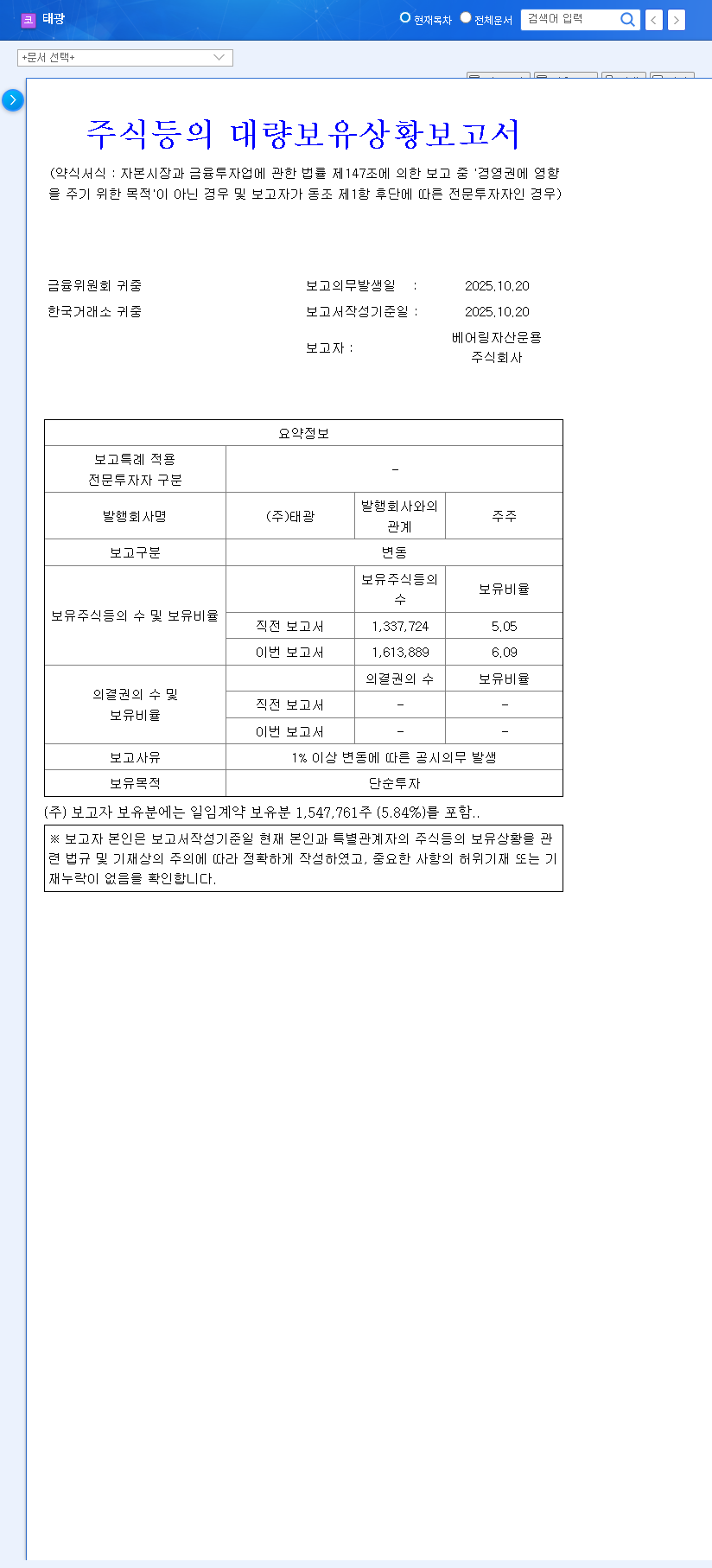

According to a report filed on November 7, 2025, Bearing Asset Management acquired 1,496 shares of T. K. CORPORATION between October 16 and October 20. This purchase increased its total holdings from 5.05% to a more substantial 6.09%. The move was officially reported in a disclosure to financial authorities (Official Disclosure). While labeled a ‘simple investment,’ such an increase from an institutional player often carries more weight. It typically indicates a strong belief in the company’s long-term intrinsic value and growth potential, separate from any intent to influence management decisions.

“When an institution like Bearing Asset Management significantly increases its stake, the market interprets it as a vote of confidence. It suggests their deep analysis points to an undervalued asset with a solid foundation, which can be a powerful catalyst for positive investor sentiment.”

This increase in institutional ownership often serves as a stabilizing force and a positive signal to the broader market. It can enhance investor confidence, attract further investment, and potentially put upward pressure on the T. K. CORPORATION stock price as retail investors follow the lead of what they perceive as ‘smart money’.

A Fundamental Deep Dive: T. K. CORPORATION Stock Analysis

To understand why Bearing Asset Management is bullish, we must look beyond the headlines and into the company’s core fundamentals as of its latest semi-annual report.

Core Business: The Plant Equipment Powerhouse

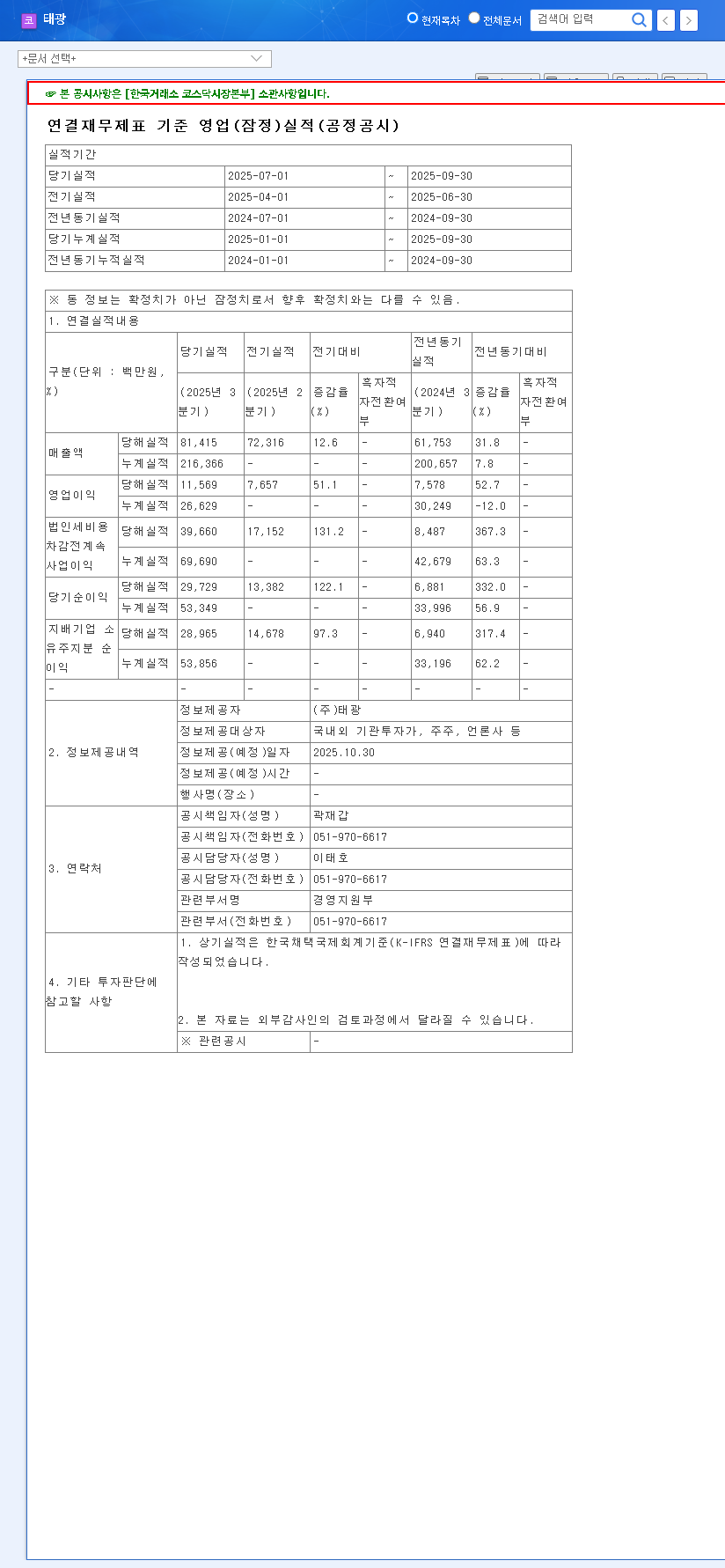

The primary revenue driver for T. K. CORPORATION is its plant equipment division. In Q2 2025, this segment posted revenues of KRW 121.3 billion. However, this represented a decrease from the prior year, highlighting the segment’s sensitivity to global investment cycles in the plant and shipbuilding industries. With a high export ratio of nearly 90%, the business is heavily influenced by exchange rate fluctuations. While this can be a risk, a weaker Korean Won against the Euro or US Dollar can also significantly boost profitability, making it a key factor to watch. The company has demonstrated an ability to maintain price competitiveness despite volatility in raw material costs.

Growth Engine or Drag? The Secondary Battery Subsidiary

The company’s foray into secondary battery equipment via a subsidiary has faced headwinds. Q2 2025 revenue was KRW 12.7 billion with an operating loss, a notable decline from the previous year. This is largely due to intense competition in the global secondary battery market and order fluctuations from major clients. For this segment to become a true growth engine, it must secure long-term contracts and differentiate its technology, a key area for investors to monitor for progress.

Fortress Balance Sheet: Financial Stability and Shareholder Value

One of T. K. CORPORATION’s most compelling attributes is its outstanding financial health. With a consolidated debt ratio of a mere 9.07%, the company operates with minimal leverage, giving it immense resilience against economic downturns and the flexibility to invest in new opportunities. It holds a healthy KRW 29.6 billion in cash and equivalents. Furthermore, T. K. CORPORATION has demonstrated a commitment to shareholder returns through a consistent dividend policy, a highly attractive feature for long-term, value-oriented investors.

Strategic Outlook for Investors: What’s Next?

While the vote of confidence from Bearing Asset Management is a significant positive, a prudent investment strategy requires a neutral and watchful approach. The long-term performance of T. K. CORPORATION stock will depend on fundamental improvements, not just market sentiment. Investors should closely monitor the following key areas before making a decision. For further context, you can review our comprehensive guide to analyzing industrial stocks.

- •Core Business Recovery: Keep a close eye on order trends and performance metrics in the plant equipment division. A rebound here is critical for overall corporate health.

- •Secondary Battery Turnaround: Look for signs of profitability improvement, new client acquisitions, or technological advancements in the battery equipment subsidiary.

- •Macroeconomic Indicators: Monitor exchange rates, raw material prices, and global interest rate policies. As an export-heavy company, these factors, detailed in authoritative reports from sources like Reuters, will have a direct impact on performance.

- •New Venture Progress: Track the development of new business initiatives like solar power and food manufacturing to see if they can evolve into meaningful, long-term revenue streams.

In conclusion, Bearing Asset Management’s increased stake is a compelling endorsement of T. K. CORPORATION’s underlying value. The company’s stellar financial health provides a strong safety net, but investors must weigh this against the current performance challenges in its primary and secondary business segments. A cautious, well-researched approach focused on tangible business improvements will be the key to capitalizing on this potential opportunity.