On November 5, 2025, the release of the DONGJIN SEMICHEM Q3 2025 earnings report sent ripples through the investment community. The provisional consolidated figures for DONGJIN SEMICHEM CO., LTD. (KRX: 005290) revealed a noticeable dip in key metrics, sparking immediate concerns about the company’s short-term trajectory. Both revenue and operating profit fell short of expectations, raising a critical question: is this a temporary setback or a sign of deeper issues? This comprehensive DONGJIN SEMICHEM analysis aims to look beyond the headline numbers.

We will dissect the factors contributing to the quarterly slump, evaluate the company’s resilient core businesses, and assess the long-term potential of its strategic growth initiatives. By examining the full picture—from macroeconomic pressures to internal cost structures—we provide investors with the context needed to understand the true value proposition of DONGJIN SEMICHEM stock and make more informed decisions.

The Q3 2025 Earnings Report at a Glance

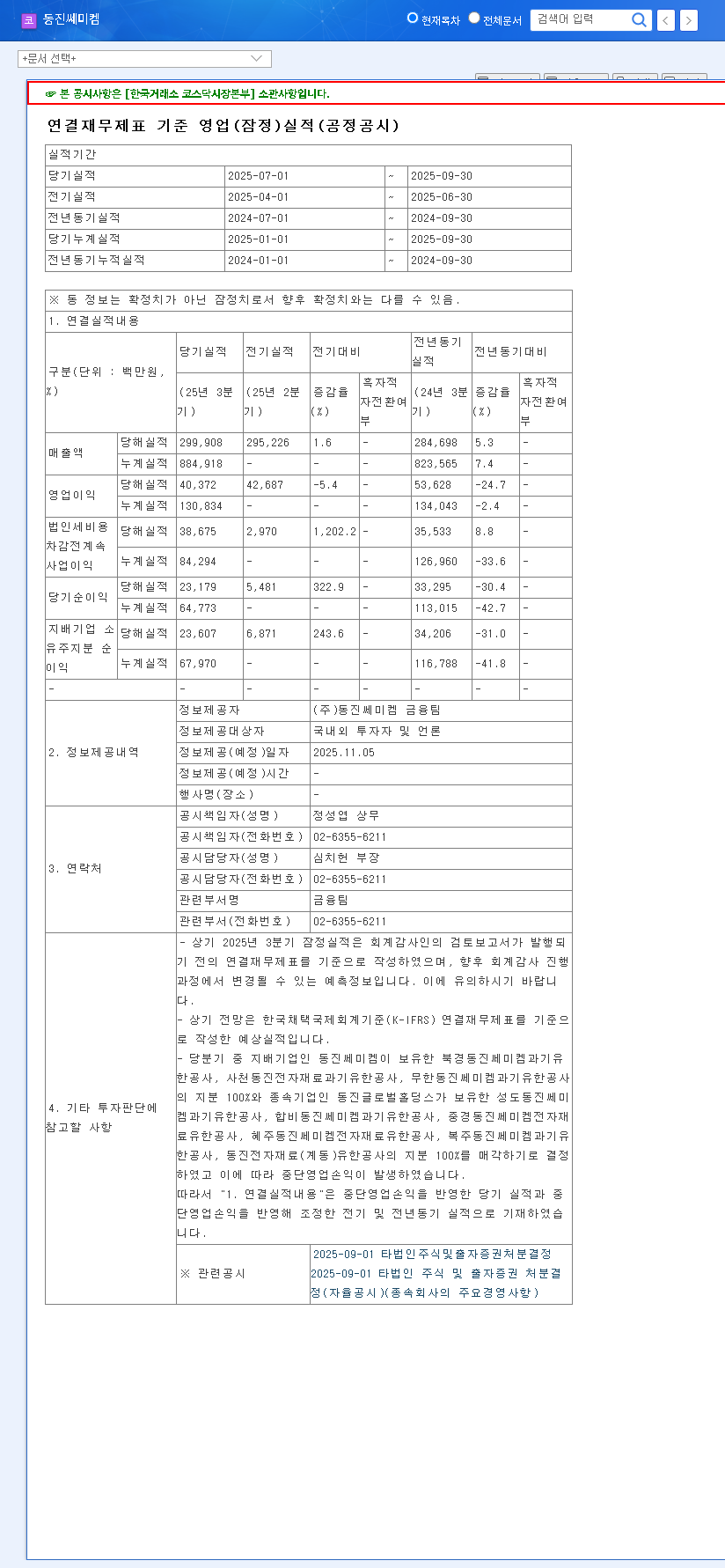

The official disclosure presented a challenging quarter for the company. The numbers, when compared both quarter-on-quarter (QoQ) and year-on-year (YoY), paint a picture of contraction.

Q3 2025 Provisional Consolidated Results:

• Revenue: KRW 299.9 billion (down 20.4% QoQ, down 16.3% YoY)

• Operating Profit: KRW 40.4 billion (down 24.9% QoQ, down 34.9% YoY)

• Net Income: KRW 23.6 billion

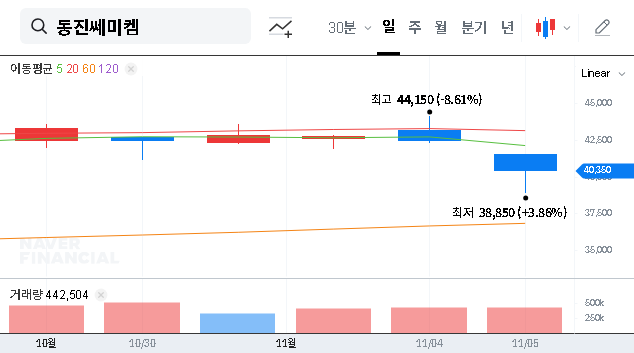

These figures clearly missed market expectations and triggered immediate downward pressure on the DONGJIN SEMICHEM stock price. The official financial data can be reviewed in the Official Disclosure filed on DART.

Why the Slump? A Multi-Factor Analysis

The underperformance in the 005290 earnings report wasn’t caused by a single issue, but rather a confluence of industry-specific headwinds and broader economic factors.

1. Headwinds in the Display Materials Segment

While the semiconductor materials business remained a robust pillar, accounting for a significant portion of the company’s revenue, the display segment faced considerable challenges. Intensifying competition, particularly from Chinese manufacturers, has led to pricing pressures. Furthermore, fluctuating capital expenditure plans from major display panel clients created demand uncertainty, directly constraining revenue growth in Q3.

2. Persistent Cost Burdens and Macroeconomic Pressures

External economic forces played a significant role. The elevated USD/KRW exchange rate (around KRW 1,315) increased the cost of imported raw materials, squeezing profit margins. Although oil prices showed a downtrend, which could offer future relief, the impact of prior cost increases and volatile raw material prices continued to weigh on Q3 profitability. This is a common challenge for global manufacturers, and a deeper dive into managing supply chain risk is crucial for long-term stability.

3. Strategic Investments Impacting Short-Term Profit

DONGJIN SEMICHEM is not standing still. The company is actively investing in future growth engines, including materials for secondary batteries (for electric vehicles) and fuel cells. These crucial R&D and facility investment costs, while essential for long-term value creation, directly impacted short-term profitability in Q3. This reflects a classic trade-off between current earnings and future growth.

Beyond the Quarter: Long-Term Growth Drivers Remain Intact

Despite the disappointing DONGJIN SEMICHEM Q3 2025 earnings, the company’s fundamental strengths and long-term outlook offer a more optimistic perspective.

- •Semiconductor Leadership: The company holds a formidable position in semiconductor electronic materials, especially advanced photoresists (e.g., EUV, ArF) critical for next-generation chip manufacturing. As the global semiconductor industry, analyzed by institutions like Gartner, continues its push towards miniaturization and complexity, demand for DONGJIN’s core products is set to grow.

- •New Growth Engines: The investments in secondary battery and fuel cell materials position DONGJIN to capitalize on the global shifts towards electric mobility and clean energy. Successful commercialization in these areas could unlock significant new revenue streams and drive substantial long-term corporate value.

- •Stable Financials: With over KRW 1 trillion in total equity, the company maintains a stable capital structure. Its debt-to-equity ratio is improving, providing a solid foundation to navigate short-term volatility and fund future growth initiatives.

Investor’s Action Plan: Key Monitorables for DONGJIN SEMICHEM

For those conducting a thorough DONGJIN SEMICHEM analysis, the focus must now shift to the future. Here are the critical points to monitor moving forward:

- •Q4 Rebound & Annual Guidance: Can the company recover in the fourth quarter? Close attention should be paid to the Q4 results and the company’s official forecast for the full year 2025 and outlook for 2026.

- •New Business Milestones: Look for concrete announcements regarding the commercialization timelines, customer acquisitions, or technological breakthroughs in the secondary battery and fuel cell segments.

- •Cost Management Execution: Monitor the company’s strategies for mitigating the impact of foreign exchange rates and raw material costs. Improved operational efficiency will be key to restoring profitability.

- •Global Market Strategy: Assess how DONGJIN adapts to the evolving dynamics in the Chinese display market and the global semiconductor landscape.

In conclusion, while the DONGJIN SEMICHEM Q3 2025 earnings were undoubtedly a disappointment, they reflect short-term pressures rather than a collapse of the company’s long-term investment thesis. The core semiconductor business remains strong, and strategic bets on future technologies are promising. Cautious observation and a focus on the key milestones listed above will be essential for investors navigating the current uncertainty.