The latest development surrounding HYUNDAI BIOSCIENCE CP-PCA07, a novel prostate cancer drug, has captured significant attention from the investment community. The recent approval for an amendment to its Phase 1 clinical trial plan is a critical milestone, offering valuable insights into the company’s R&D capabilities and signaling a potentially powerful new growth engine. This in-depth analysis will break down the specifics of the trial, evaluate the company’s strategic position, and provide a clear outlook for investors monitoring this promising biotech venture.

Understanding the Milestone: CP-PCA07 Phase 1 Approval

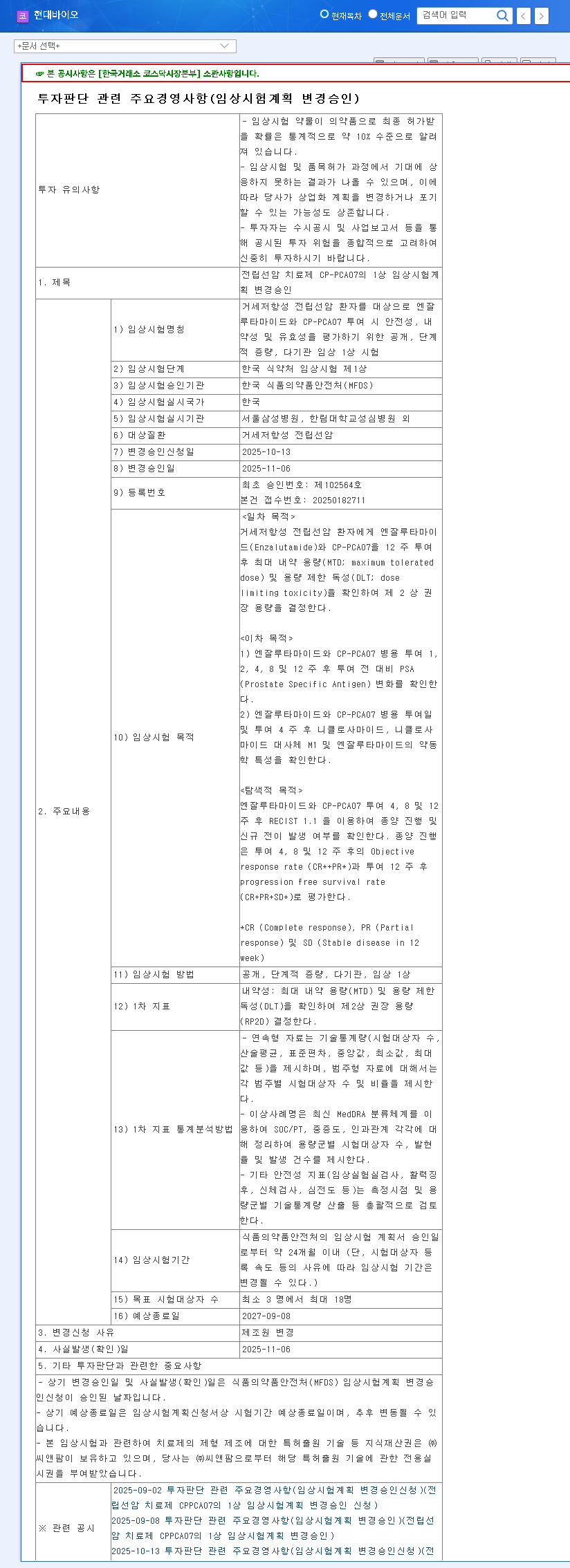

On November 7, 2025, HYUNDAI BIOSCIENCE announced it had received regulatory approval for an amended Phase 1 clinical trial plan for its prostate cancer drug, CP-PCA07. This crucial study focuses on patients with castration-resistant prostate cancer (CRPC), a form of the disease that continues to progress despite hormone therapy. According to the Official Disclosure, the trial employs a combination therapy approach, pairing CP-PCA07 with Enzalutamide, a standard-of-care anti-androgen medication.

Primary Objectives of the Phase 1 Clinical Trial

The core goals of this early-stage trial are fundamental to the drug’s future development. Researchers aim to establish safety and dosing parameters, which are essential before advancing to larger, more complex trials. The key objectives include:

- •Maximum Tolerated Dose (MTD): Determining the highest dose of CP-PCA07 that can be administered without causing unacceptable side effects.

- •Dose Limiting Toxicity (DLT): Identifying potential severe side effects that would prevent further dose increases.

- •Recommended Phase 2 Dose (RP2D): Establishing the optimal dose to be used in subsequent Phase 2 efficacy trials.

Success in this phase is not about curing the disease but about proving the drug is safe enough to move forward, a critical hurdle in the long journey of pharmaceutical development. For more information on prostate cancer, authoritative sources like the National Cancer Institute provide extensive resources.

Why This Development Bolsters the HYUNDAI BIOSCIENCE Investment Case

This clinical trial approval doesn’t exist in a vacuum. It arrives amidst several other positive developments that collectively strengthen the company’s fundamentals and long-term potential.

- •Enhanced Credibility: The company recently corrected a past accounting error in its R&D cost reporting, a move that significantly improves the transparency and credibility of its financial information.

- •Improved Financial Health: A recent capital increase secured 85.8 billion KRW, allowing for the full repayment of short-term debt. This financial fortification provides a stable runway for sustained R&D investments.

- •Expanding Drug Pipeline: The progression of HYUNDAI BIOSCIENCE CP-PCA07 adds another high-potential asset to a pipeline that already includes a COVID-19 treatment (CP-COV03) and a pancreatic cancer therapy (POLYTAXEL). Diversification is key to mitigating risk in the biotech sector.

- •Validated Technology: The core formulation technology, patented by partner CNPharm and licensed exclusively to HYUNDAI BIOSCIENCE, serves as an indirect validation of the company’s competitive technological edge.

Investor Outlook: A Balanced Perspective

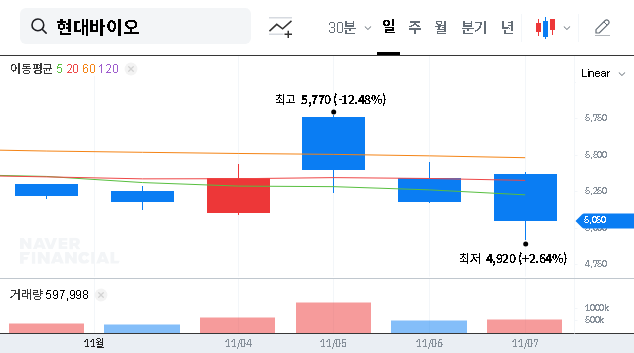

Given the high uncertainty and long timeline of drug development, a long-term perspective is crucial. Focus on clinical progress and tangible outcomes rather than short-term market fluctuations.

Potential Positives

The advancement of the HYUNDAI BIOSCIENCE CP-PCA07 trial is a clear positive. It signals pipeline progression, boosts investor confidence, and, if successful, could unlock a significant revenue stream in the multi-billion dollar prostate cancer treatment market. Each successful step de-risks the asset and adds tangible value to the company.

Risks and Considerations

Investors must remain pragmatic. Drug development is inherently risky, with a high failure rate. This is only a Phase 1 clinical trial, meaning commercialization is still many years and several successful trials away. Furthermore, macroeconomic factors like high interest rates can increase fundraising costs and dampen investor sentiment across the biotech sector. For a deeper understanding of these market forces, you can read our guide on Navigating Biotech Investments.

Frequently Asked Questions

What is the significance of the approved HYUNDAI BIOSCIENCE trial?

HYUNDAI BIOSCIENCE received approval for an amended Phase 1 clinical trial of its prostate cancer drug, CP-PCA07. It’s a safety and dosage study for patients with castration-resistant prostate cancer, a critical first step toward potential commercialization.

How does this approval impact the company’s outlook?

The approval is a positive catalyst. It validates their R&D progress, expands their clinical pipeline, and can improve investor sentiment. Long-term, a successful drug could become a major revenue driver.

What should investors consider before investing?

Investors should adopt a long-term view. Key considerations include the inherent risks and high failure rates of clinical trials, the extended timeline to market, and broader macroeconomic factors affecting the biotech industry.

In conclusion, the approval of the amended Phase 1 trial for HYUNDAI BIOSCIENCE CP-PCA07 is a tangible and encouraging step forward. Paired with a strengthened financial position and a growing pipeline, the company is building a compelling growth story. However, a prudent investment strategy requires continuous monitoring of clinical data and a clear-eyed view of the associated risks.