In a move signaling strong forward momentum, Pharmicell Co., Ltd. (005690) has captured significant market attention with a major supply contract for electronic materials. This strategic partnership with DOOSAN ELECTRO MATERIALS (CHANGSHU) CO., LTD. not only bolsters its biochemical division but also provides a clearer lens through which to conduct a thorough Pharmicell stock analysis. This article will dissect the implications of this deal, explore the company’s robust growth drivers in mRNA and stem cell therapy, and evaluate its improving financial health to provide a comprehensive outlook for investors.

We will examine the core components of Pharmicell’s value proposition, from its stable Biochemicals business to the high-potential, long-term growth promised by its Biomedical division’s innovative pipelines. Understanding these dynamics is key to assessing the future Pharmicell growth trajectory.

The Strategic Doosan Electro Materials Contract

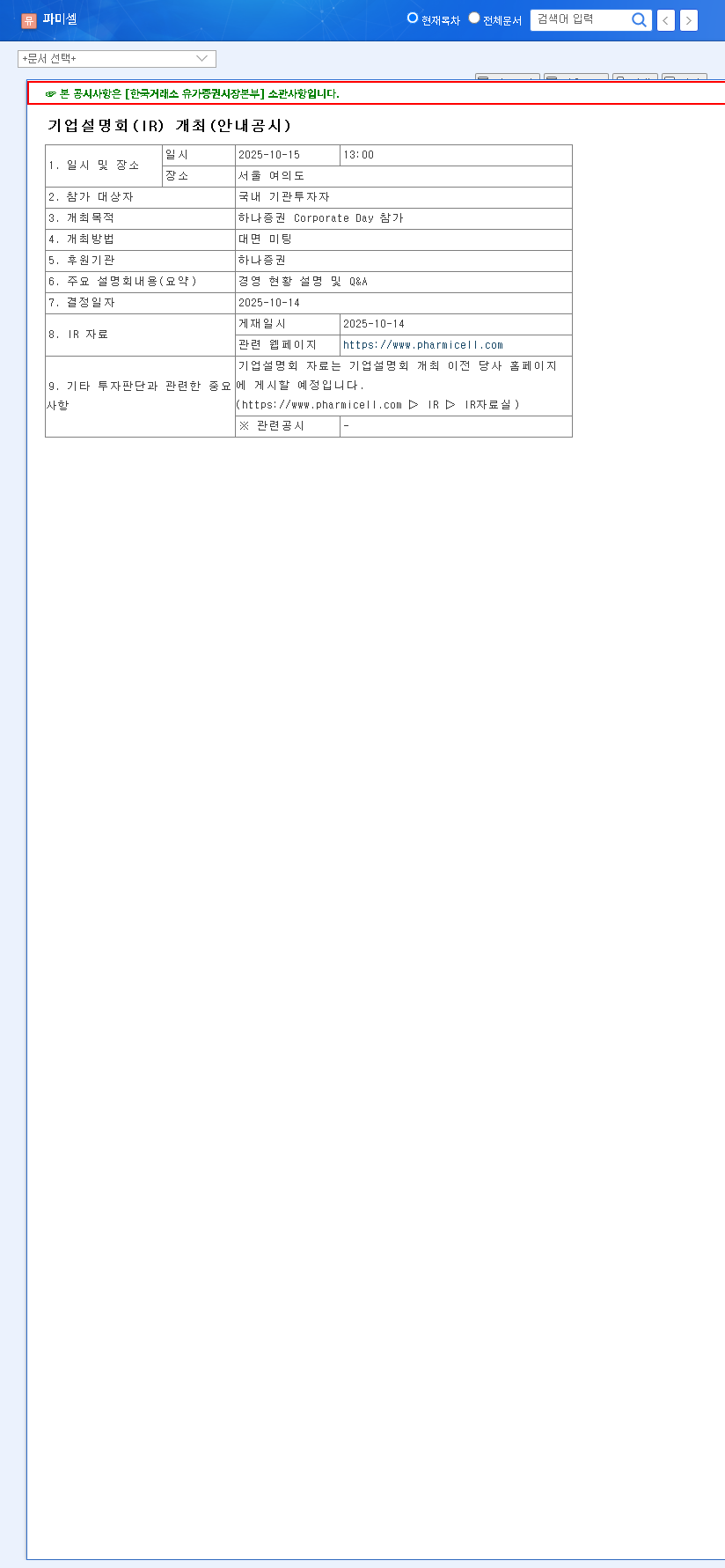

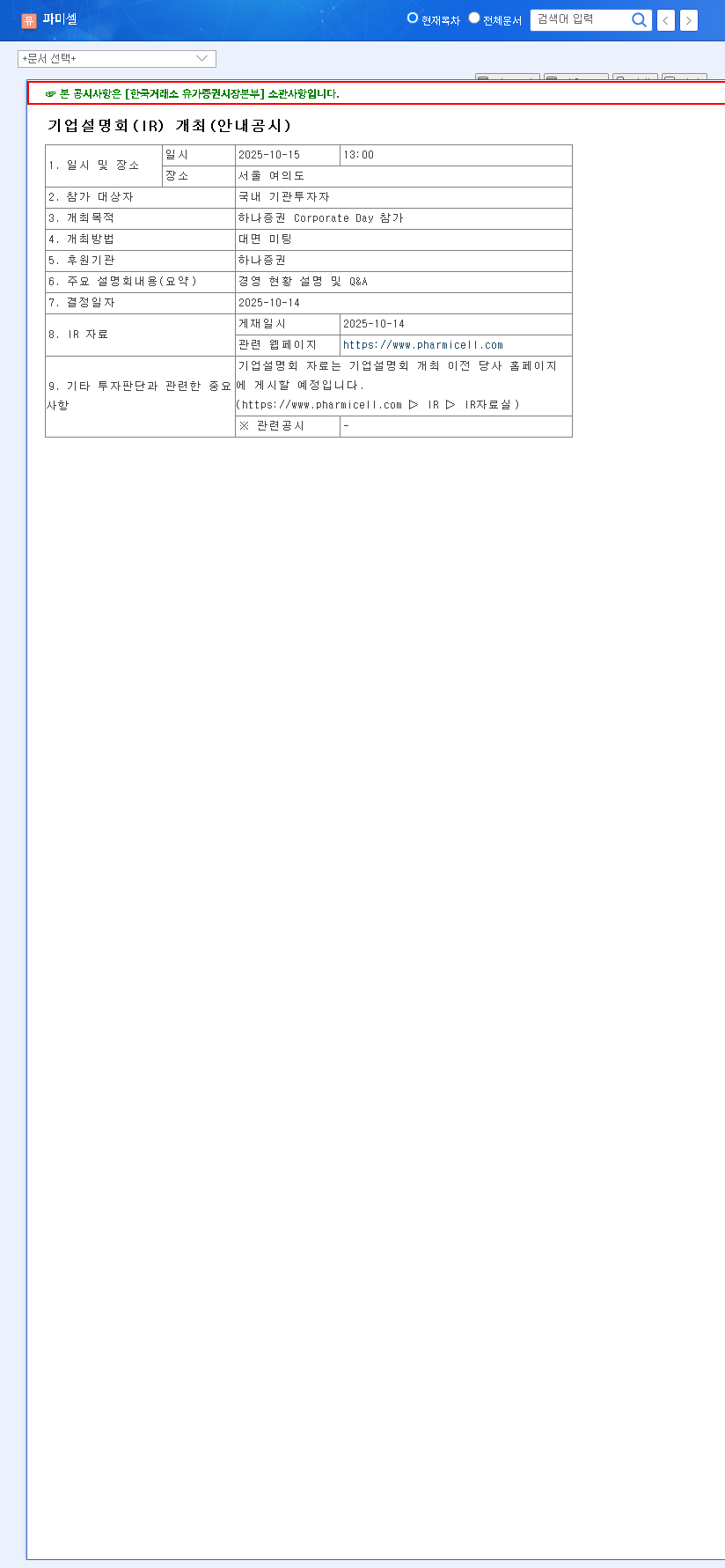

Pharmicell recently finalized a significant supply contract with Doosan Electro Materials, a deal valued at 6.3% of the company’s recent annual revenue. The agreement, set to run from late 2025 to early 2026, involves the supply of advanced electronic materials to Doosan’s operations in China. This move is expected to provide a direct and immediate boost to the revenue stream of Pharmicell’s Biochemicals business division, strengthening its market position and enhancing its portfolio. This information is based on the company’s latest official filing. (Source: Official Disclosure)

Analyzing Pharmicell’s Dual Growth Engines

Pharmicell’s business is strategically divided into two core segments, each with a distinct role in the company’s overall growth strategy: the stable, cash-flow-generating Biochemicals division and the high-potential Biomedical division focused on future innovations.

Biochemicals Division: Powering Modern Medicine and Technology

The Biochemicals division is the current cornerstone of Pharmicell’s financial performance. Its growth is propelled by powerful trends in global health and technology.

- •High-Demand mRNA Raw Materials: As a key supplier of nucleosides and PEG derivatives, Pharmicell is directly benefiting from the explosion in the mRNA vaccine and gene therapy markets. The demand for these essential mRNA raw materials is projected to grow steadily, a trend validated by a recent quality certification from European pharmaceutical giant UCB, which opens doors for expanded commercial sales.

- •Advanced Electronic Materials: The rise of 5G, AI, and high-performance computing has created soaring demand for specialized electronic components. Pharmicell’s low dielectric materials are critical for AI accelerators, positioning the company to capitalize on the tech industry’s relentless innovation. For more on this trend, see this report on the semiconductor market.

Biomedical Division: Pioneering Stem Cell Therapy

While the Biochemicals division provides stability, the Biomedical division represents Pharmicell’s long-term, transformative potential. The company’s heavy investment in R&D (11-15% of revenue) is fueling a promising pipeline of stem cell therapy candidates. Key projects like Cellgram-LC (for alcoholic liver cirrhosis), Cellgram-ED (for erectile dysfunction), and Cellgram-CKD (for chronic kidney disease) are progressing through clinical trials. Successful commercialization of any of these therapies could become a massive new growth engine, tapping into a global stem cell market growing at nearly 15% annually.

Pharmicell presents a compelling investment case built on a foundation of stable biochemical revenue and the explosive, long-term potential of its innovative stem cell therapy pipeline. The Doosan deal further de-risks the short-term outlook.

Financial Health: A Turnaround Story

A critical component of any Pharmicell stock analysis is its financial stability. The company has demonstrated a remarkable turnaround, with revenue increasing 15% year-on-year in 2024 to KRW 64.85 billion and, more importantly, a return to operating profitability with a surplus of KRW 4.65 billion. This financial strengthening is evident in key metrics: the debt ratio has fallen to a very healthy 14.84%, while the current ratio has surged to 628.24%, indicating excellent short-term liquidity. This improved financial footing provides a solid base for continued R&D investment and strategic growth initiatives. To learn more about financial metrics, you can read our guide to investing in biotech.

Investment Outlook: Balancing Positives and Risks

Key Strengths (Positive Factors)

- •Diversified Revenue: Stable, growing income from the Biochemicals division, enhanced by the new Doosan contract.

- •High-Growth Potential: The Biomedical division’s stem cell therapy pipeline offers significant long-term upside.

- •Solid Financials: A profitable status, low debt, and strong liquidity reduce investment risk.

Potential Risks to Consider

- •Clinical Trial Uncertainty: The success of stem cell therapies is not guaranteed, and clinical trial outcomes are a major binary risk.

- •Macroeconomic Headwinds: As an exporter, Pharmicell is exposed to currency fluctuations and changes in the global economic climate.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investment decisions should be made based on your own research and risk tolerance.